In this video, Matt from Wealth Advisor Training, along with Ben and Stephanie, discusses the art of traveling the world for free using credit card points. Matt shares his experience of saving over $40,000 annually with this method, highlighting its relevance for financial advisors who can leverage business expenses and taxes through credit cards and teach their clients to do the same.

The video explains how credit card companies generate profits by taking a percentage of every transaction while enticing users with rewards programs. Matt details how users can earn one-time bonuses ranging from 50,000 to 100,000 points by opening new cards and meeting minimum spending requirements within the first three months. He underscores the need for discipline and meticulous tracking.

Matt also explores how credit card companies profit from users who maintain balances and pay high interest rates, proposing a strategy of using significant purchases to secure sign-up bonuses and then closing the card before moving on to the next one. The video briefly touches on the psychological aspect of spending with credit cards versus cash or debit cards.

Additionally, the video acknowledges concerns about potential impacts on credit scores when opening multiple credit cards, promising to delve into a more detailed strategy in the subsequent video.

All right, today we are here, Matt, with Wealth Advisor Training, here with Ben and Stephanie. Today we’re talking about how to travel the world for free, utilizing credit card points, something I’ve been doing for over ten years, adding up all the savings of average $40,000 a year of actual dollars and saved versus what it would have cost to travel to these places.

So excited to bring this to Wealth Advisory Training, really for two reasons. One, financial advisors typically are 1099 and have the huge opportunity for business expenses and also the taxes that they can put on the credit cards and we can show how to really leverage that.

And then two, for financial advisors to use this information and also to teach their clients how to do it. Because we do this a lot with our clients with Roth conversions paying for taxes, and we’re asking about their goals and dreams, and typically the goals and dreams are around traveling the world.

So if we can help do that for free, it’s a win win for everybody. So twofold, we figured the best format to do this would actually be to show Stephanie and Ben the ropes for the current setup. We’re going to go through a couple of examples.

Stephanie is a K one, meaning she has to pay taxes out of her pocket, similar to 1099. And then Ben has W Two structure, which a lot of advisors and most like 99% of clients will have. Also want to show how this is completely possible with the W Two structure because I’ve been on that structure before and that’s been possible.

So we’re going to use two different examples as we go through this. So Ben, Stephanie, any questions before we get started? I’m going to give a quick intro into how this works, just in general. But before we go into the intro, any question just in general on the credit cards?

No questions for me. I just think this is a really important concept because I think everyone’s looking to. Figure out how to be more efficient with expenses that they know they’re going to be spending.

So I think the more information that people have about a subject like this is going to be very relevant. Yeah, I think there’s just no losing in this situation. I would say if you ask a blanket number of clients, like, what one of their big goals is during retirement, they say travel.

So I think this basically covers a couple of different topics that we come across often. Excited. Awesome. Okay, perfect. Well, so just a quick introduction to how this works. So in general, credit card companies take 2% of every transaction.

So just for example, if you’re a gas station, people are pumping gas and they’re using your credit card, they’re going to take 2% of every transaction. So this becomes the highest expense for a lot of business owners if their customers are using credit cards.

So the reason I give that background is most credit card companies are profitable for one of two reasons. One, they’re taking the two to 3%. And then two, the average American holds a credit card balance, and at that point, the interest rate could be between ten to 25%.

Typically what we see that becomes extremely lucrative. I mean, the balances, if it’s like 20 plus percent, it could be doubling every couple of years. And then the credit card companies obviously profit as well.

So this is not to scare you off. This is just the reason of why this we’ll call it the game actually exists. So that’s the first piece of information. The second piece of information is that every credit card wants your business because of those two facts.

So because of this, credit card companies want to lure you in so that. You’re using their card so they can two or 3%, you’re using their card so you get behind your balance and they can charge you astronomical fees and interest.

So how do they lure you in? Well, they better have the most awesome rewards program. A lot of credit cards will actually offer some very complicated rewards. Five X on groceries, ten X on travel, whatever.

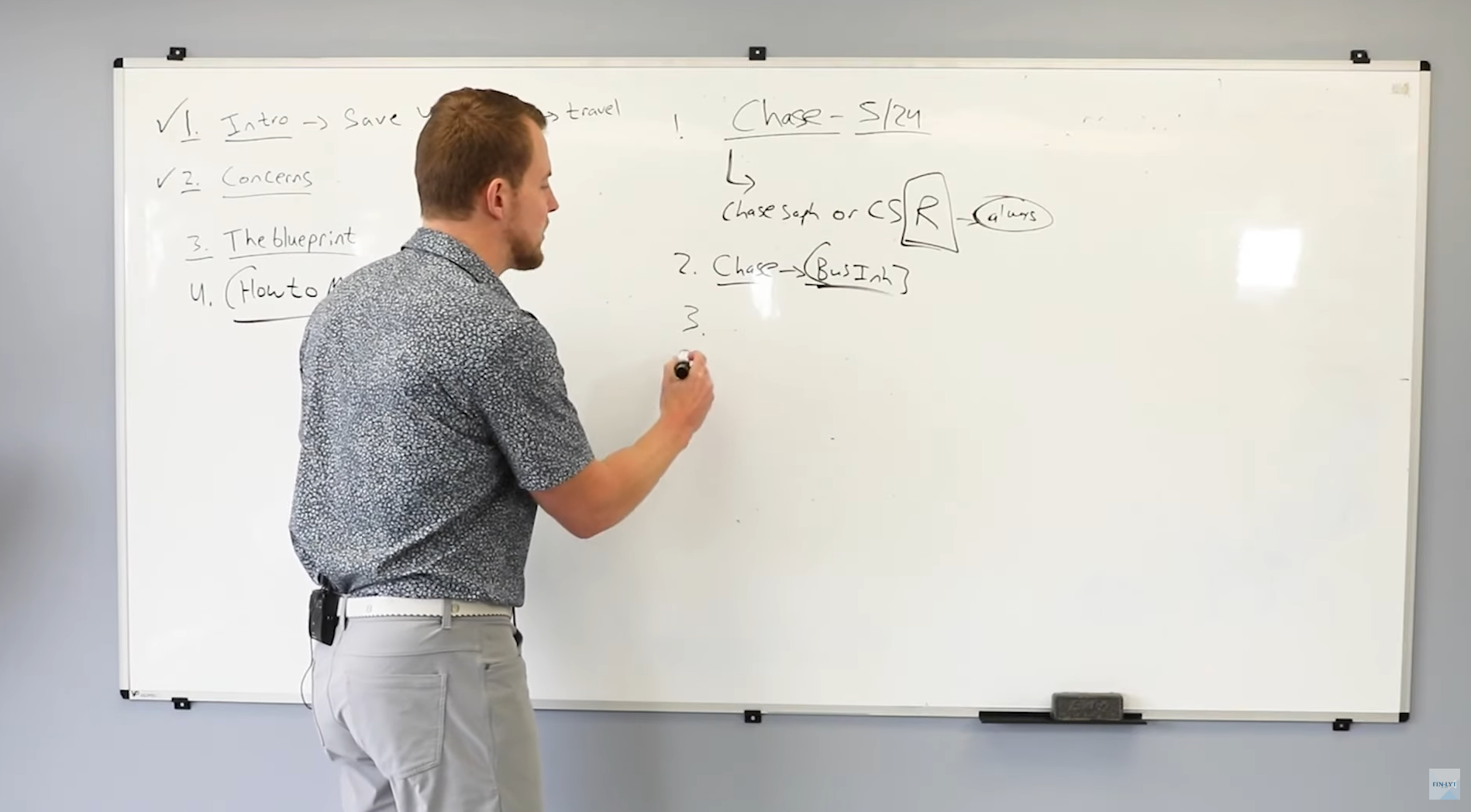

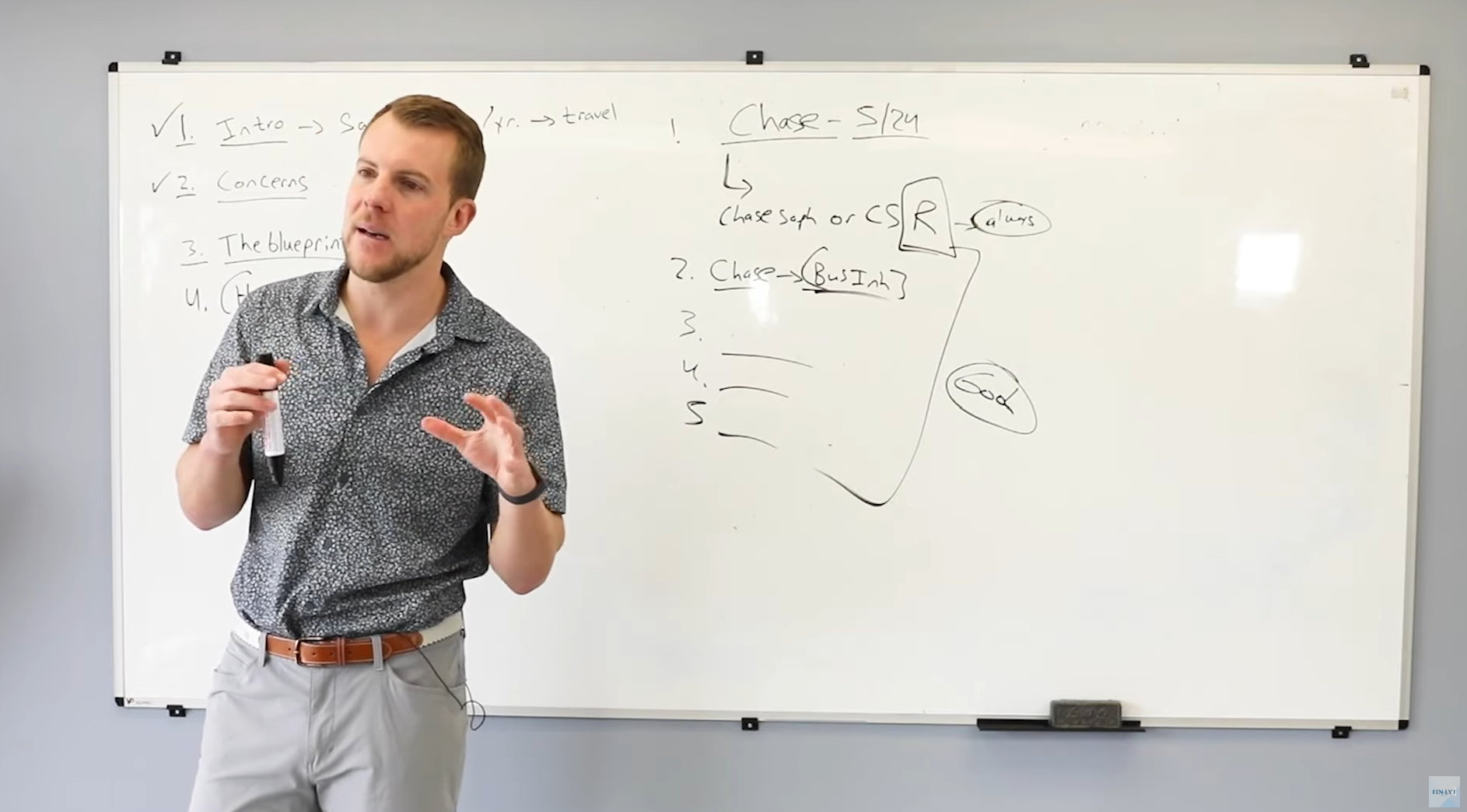

The point of what we’re talking about has nothing to do with that. This is much more simple. What credit cards will do is they’ll offer you one time bonuses and the one time bonus is anywhere typically between 50 to 100,000 points.

If you do two things, you open the card and you spend a minimum spend in the first three months. So, hypothetically, Chase is some of my favorite cards. If you open up a Chase Sapphire reserve card right now, you spend 4000 the first three months.

You get 75,000 points in the first three months. So that is how it exists. That is why credit cards, how they make their money is very clear. And I would argue credit cards don’t make really much money for me, even though they’re taking 2% because I leverage the points to a very dramatic level.

They’re still making money though. And so this game will always be available for those that are disciplined and take a little bit of extra time to figure it out. So any questions so far on any of that?

No? That makes sense as to why they would offer that to you if they’re capitalizing in two different ways. Okay, cool. So what I’m about to tell you next is may sound too good to be true, but that background is helpful.

So, um, there’s two ways to do this. So, ideally, you know, 1000 points typically will equal, so 100,000 points will equal. $1,000 if you don’t know what you’re doing. But just in general, if you have an existing credit card, it would take $100,000 of spending to get 100,000 points, just dollar for dollar on the existing card if you’re not tracking what you’re purchasing.

So the credit card just profited 2% at minimum, probably 3% 2000, $3,000, and they’re giving you $1,000 back. So that’s just simply how this works. So the hard way to do this is you just put all your spend on a credit card.

The easy way to do this is when you have big purchases, you always use those purchases to get the sign on bonuses. Then you shut that card off, take the points run, you move on to the next card. So some people may stop here.

When I say I opened up 20 cards a year for the first couple of years of doing this. That is an under exaggeration. I did. But in the first year of doing this, I earned 2 million points, which ended up being worth an astronomical amount of money because we’re going to talk about how you can stretch your points very good on international travel and some hotel brands specifically.

Any questions on that so far? I feel like you’ll probably get to it, but the first thing I think of is if you are going to open 20 to 30 cards, how does that impact your credit negatively? Possibly. So we’re actually getting right into step number two, which video number two, which will be your concern?

So that’s the most important question. But any other thoughts or questions on just the introduction here of what the game entails? Yeah, I would just say a conversation that I’ve had with clients and other advisors just about credit cards in general is and I’m not saying I agree or disagree with this, but.

Psychologically, does it hurt more when you spend cash? When you spend a debit card and you see your balances go down, is it easier to spend money with a credit card than it would be paying out of cash?

Psychologically, would you spend less if you didn’t have credit cards? It’s an interesting conversation. It’s something that I think about personally, too. When I pay out of cash or when I use a debit card and I see the balance go down or I physically watch the cash leave, that could psychologically be like, oh, I’m spending a lot, whereas if I swipe a credit card, maybe you don’t realize actually how much you’re spending.

Do you find any truth to that from just a general credit card? And I don’t want to get too off track, but I think it’s relevant for a conversation of just credit cards and spending as a whole. No, absolutely.

So it’s much easier to spend money when you have a credit card versus if it’s cash or if it’s a debit card where you’re tracking the balance and the balance actually matters because your transaction get declined, where in a credit card it won’t unless you hit your credit card limit.

So this is going to go right into the concerns as well, but I’m going to address that exact thing because you can get yourself in trouble in pursuing points. My recommendation is pursue points with what you know you’re already going to do, but don’t spend just for the pursuit of points.

So it’s a big difference. I’m going to talk about some barriers, some lessons learned along the way, but we’ll definitely get into that in a second. All right, that’s it for the intro. Look forward to addressing concerns, and then we’ll go through the blueprint as the third step.

Awesome. Thank you.

Playlist

In 15 minutes we can get to know you – your situation, goals and needs – then connect you with an advisor committed to helping you pursue true wealth.

EWA, LLC dba Equilibrium Wealth Advisors, is an SEC-registered investment advisory firm providing investment advisory and financial planning services to clients.

Investments in securities and insurance products are not insured by any state or federal agency.

To view EWA’s public disclosure, registration, Form ADV and Part 2B’s, click here.

To view EWA’s Client Relationship Summary (CRS), click here.