Hi everybody. Matt here with Jameson and Ben from EWA. Really excited to have this course live on credit cards and how to maximize the points and how to travel the world for free. And we love helping you get your vacations for free.

So one of the most common things that we do for our clients is Roth conversions. And so those Roth conversions studies have shown the taxes that are owed on the Roth conversions, if you’re able to pay those from cash, it’s much better to have as much money growing inside the Roth post conversion as possible.

If you’re over 59 and a half, you could technically have the tax withheld out of the IRA, but it’s much more beneficial if you’re able to have the cash set aside to pay the tax liability. So we just wanted to now that we’ve watched the course, really just go through step by step mechanically on how to do this.

So Jamo said, Give us an example. You just recommend a Roth conversion? Yeah. So if a client does $100,000 Roth conversion, if they’re in the 24% marginal tax bracket, they would owe $24,000 on getting that money into the Roth IRA.

In return, never pay taxes again. Once inside the Roth IRA, this 24,000 in taxes has to be paid in that tax year. So they can go online, go on the IRS website and volunteer to go online, go on the IRS website and pay that tax either well, generally from cash, or you can use a credit card, for example.

So you can go enter your credit card info, pay the $24,000, ideally spread out over a couple of cards to hit these bonuses, and then get all the credit card points. What happens if you don’t? So the client can either pay the $24,000 let’s say it’s quarter one of 2023, and there’s a 24,000 you did $100,000 Roth conversion.

There’s a $24,000. Tax liability out there federally, the client technically could wait till April 15 of 2024 and put that on the tax return. What’s the downside of that? Yeah, there is a percentage penalty for each quarter you do not pay the tax up until that date.

Typically, it’s 1%. So we want to make sure that if we are paying the tax, we’re doing so in a timely manner. Yeah. So just option A, if you’re doing a Roth conversion, $100,000 conversion 24% tax bracket 24,000.

Option A is you could wait till April 15 of 2024 for the taxes due for your 2023 tax year, but 1% per quarter would be $240 penalty for quarter 1234. So that’s a $960 penalty. So you’d pay close to $25,000 in tax instead of $24,000.

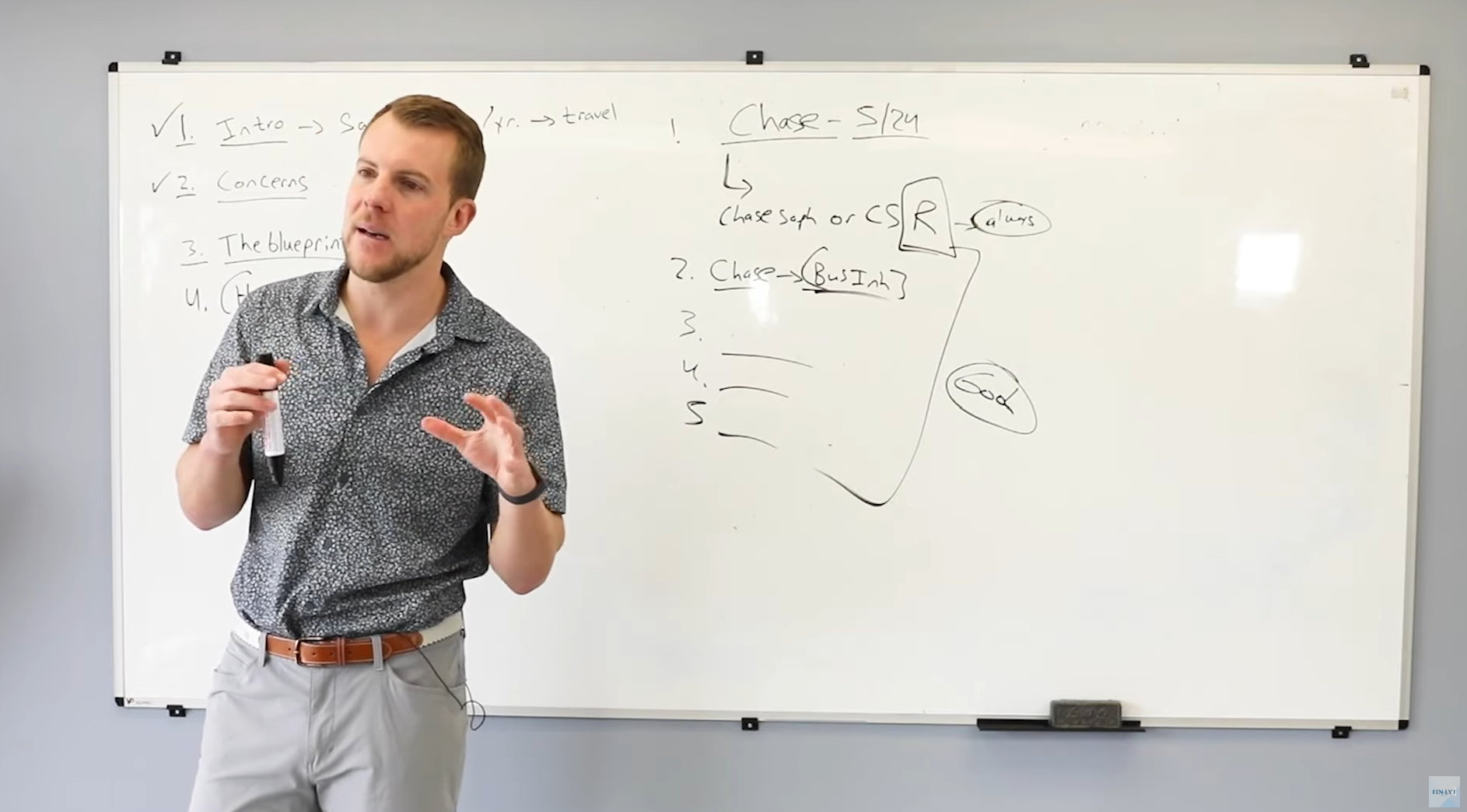

So option B would be immediately. We could spread that $24,000 tax liability on several credit cards. So you’re actually able, if you’re married filing jointly, you’re able to do two payments per spouse.

So let’s say Mr. And Mrs. Smith had done the Roth conversion. Well, the tax liability for Mr. And Mrs. Smith is all going to be on the same tax return. So you can do two payments under Mr. Smith’s name and two payments under Mrs.

Smith’s name. So technically, we could divide this by four and put $6,000 on four different credit cards. And if those are four new credit cards, we can do with the payments on one of these websites, pay 1040, Dot or Payusatax.com.

And just as a hypothetical, if you put $6,000 on a Chase Sapphire reserve card immediately, if you spend 4000 in the first three months, you get a 60,000 point bonus. We do 6000 on the Chase Sapphire Reserve for Mr. or for Mrs. smith.

That’s another 60,000. And then you could also do 6006 thousand. Like a Chase business card get 90,000 90,000. So in essence, you just got 300,000 points. And in exchange these in general, it’s a 2% charge.

So 2% of 24, that’s a $480 charge that you’re going to pay because you used a credit card. But in exchange, you’re getting 300,000 points and those points can be transferred one to one. United Airlines is a perfect example from Chase and 300,000 points would get you a first class round trip flight to Europe and back, which the cash price of that would be $20 to $40,000 versus paying $480 plus some annual fees.

So let’s say all in $1,000 to save minimum of $20,000 obviously would be well worth it when planning your vacations. So guys, anything to add to that? Any other thoughts? No. I think the big thing for me is understanding that if you are going to be spending this trying to do it as efficiently as possible I think we’ve talked about it in the previous course, but credit cards in general, it’s all relative to make sure that it’s spending that you’re planning on doing and it’s not in excess of what you’re planning on doing.

Absolutely. So, pre planned expenditures, you already plan on spending the money. We don’t want to go spend money on credit cards just for the sake of getting points. Redirect money that you already were going to spend.

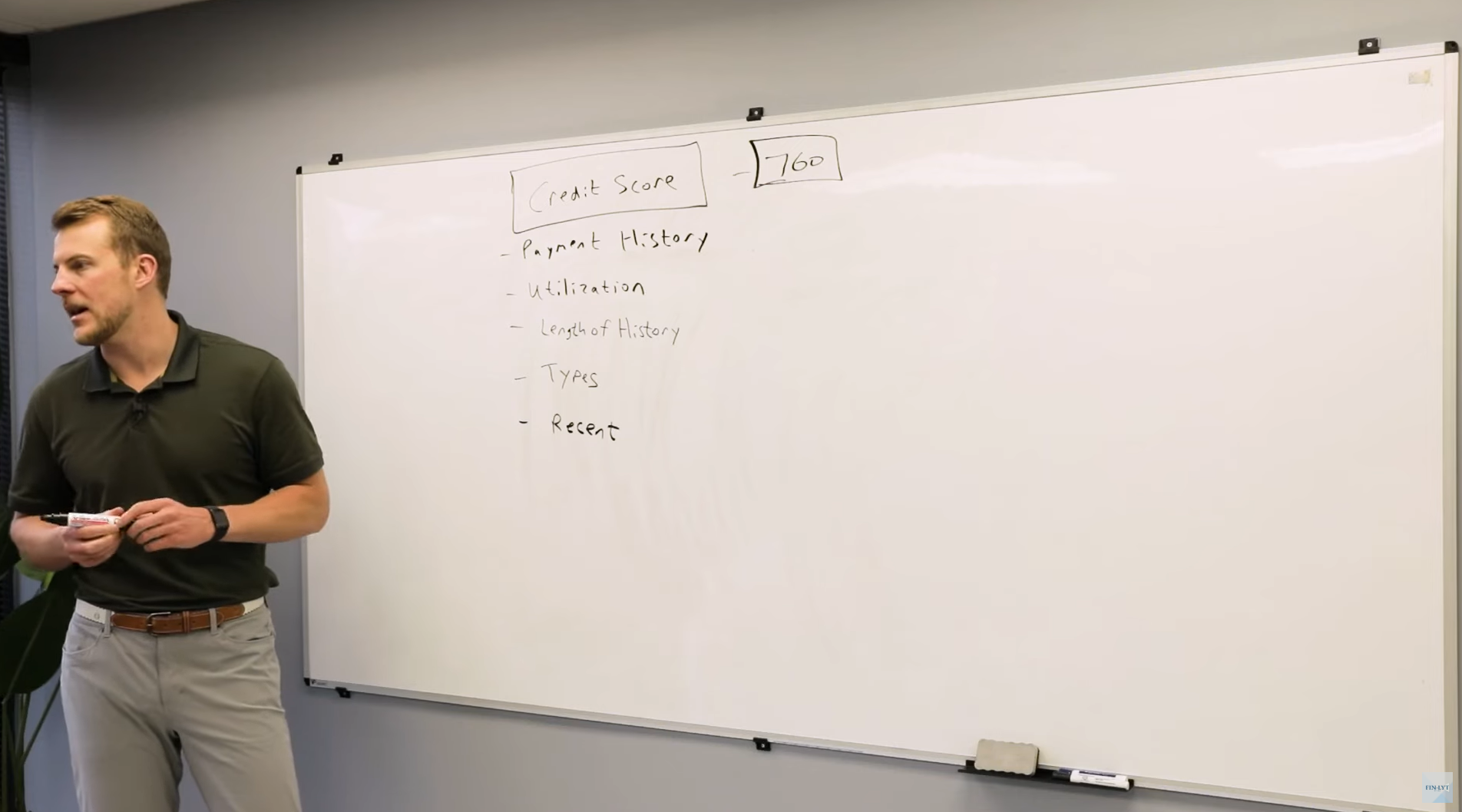

It’s a great point. Okay, perfect. Well, last video we’re going to be talking about credit score, which was one of the concerns that we talked about in the Intro video, but something we want to deep dive in to close out close.