In video two, the discussion addresses credit score concerns when opening multiple credit cards. Caution is advised before big purchases, limiting new card openings to one or two within six months. Credit utilization is emphasized, suggesting lower utilization rates are better. Tracking is recommended using an Excel spreadsheet.

The conversation covers strategies for couples and using credit cards for planned expenses to earn bonuses. Annual fees are discussed, with benefits often outweighing costs. Closing fee-based cards after obtaining bonuses is recommended, except for those tied to loyalty programs.

Chase points’ flexibility for transfers is highlighted, and the importance of using earned points is stressed. The next video promises insights into a blueprint for lifelong free flights and hotels.

All right, video two. We’re going to talk specifically around concerns you may have before jumping right into the credit card game. So Stephanie yes. Biggest question I have is about credit score because I know when you open up any type of credit card, line of credit, mortgage, et cetera, usually see like a decline or you get hit a couple of points on your credit report.

So if I open ten or 20 cards, how does that impact my credit score? Is that a negative? Potentially? That was a great question. So this was my number one concern when I started doing this. And so just the first thing is I would ask a potential client or advisor is, why does your credit score matter?

And they’d say, well, I’m buying a house or I’m buying a car in six months. Just wait on this. I would recommend if you’re within three to six months, let’s say six months of a big purchase such as a car loan, a house, et cetera, then don’t be too aggressive.

One or two cars in the last six months isn’t going to hurt you, but 20 won’t hurt you. It’ll just raise questions. So secondly, for most people, if you’re in the house you’re going to be in, if you have cars you’re going to be in, your credit score is irrelevant because it’s just a bragging, right?

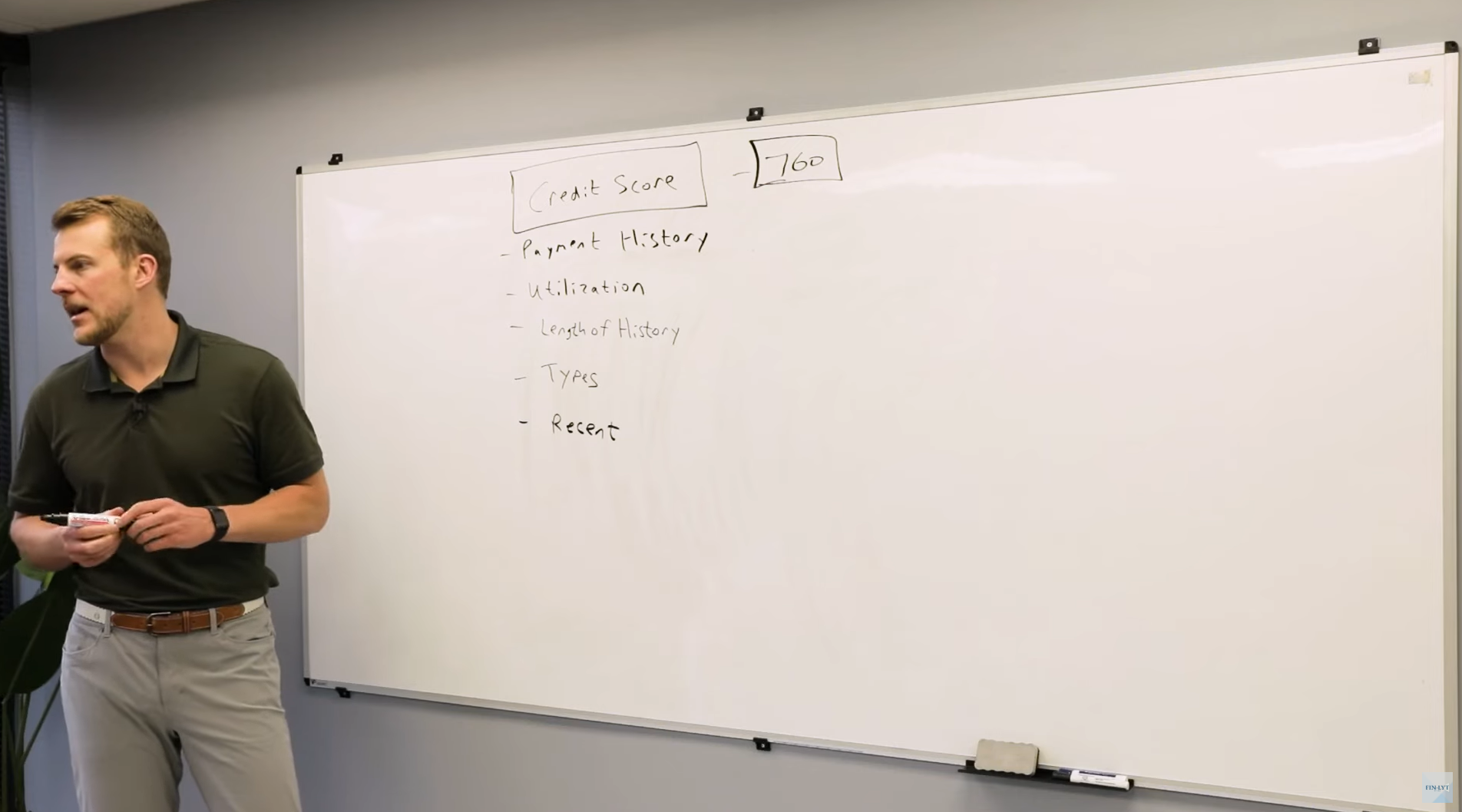

Unless you’re going to need to go borrow money. So might as well use this and save thousands and thousands of dollars. Long term credit score will go dramatically up. Because your credit score is based upon a couple of factors.

Utilization is one of the biggest ones. Utilization just means if you have one credit card that has a 5000 limit and you’re spending 4000 on that every month, your utilization is 80%. Credit card bureau gross are looking for utilization under 20%.

And so when I had 20 credit cards open at one point, I had $100,000, let’s say, of credit available. I was only spending a couple of $1,000. So my utilization was very low. So doing this actually really helps your utilization.

The type of accounts, amount of accounts, on time payments, that’s all going to positively factor into this. The one thing that hurts you is they do look at the average account duration. And so the more you have, the harder that’s going to hurt.

But I can tell you just personally, a credit score above 760 will get you the best deals on auto loans and mortgages. I’ve opened up so many, every credit card that’s been available in the marketplace and my credit score is above 800 and it has been consistently.

It may dip up and down a little bit when you start doing this, but long term this really helps. And I’m not just saying opening up because I open, I get the points, I use the points, I immediately close.

So we’re talking about two way transaction opening and closing. Literally zero concerns for your credit score. Long term, I would just advise someone if you have a big purchase for three to six months, limit yourself to one or two credit card opening or closings ahead of that purchase.

Is there any value in splitting that up? Like if you have a partner or spouse would be any value in having one partner, spouse do a few and then the other. No question. Yeah, this game applies if you are married, if you can, dating, whatever.

Traveling together. Traveling together. Every card is associated with one tax ID. And most good cards, you can only get a bonus either once in your lifetime or every two to five years. Okay, so you can actually open, close, open it again in five years and get the same bonus.

Got you. That makes sense. Any other follow up questions on credit score? None of my end. Okay, well, next question. Yeah, I would just say, is this cumbersome to track? So we’re opening a bunch of cards, using points and then closing them.

Is it different logins for different cards? Is it cumbersome and difficult to track? Where are all my points and how are they allocated? Yeah, it’s a great question. So. It’s not, it’s not as just simple as, like, expect to get millions of points.

And it’d be extremely easy, obviously, to do something as lucrative as this. It’s to take a little bit of work. So I have a friend who taught me, open up an Excel spreadsheet or a Google document, and you basically want to have the card type the day you open, give the details in there.

I need to spend 5000 in three months. I’ll put the deadline on that and then put that and we’ll put an Excel spreadsheet template in the video here. If you closed it when you closed it, because then you’ll know if there’s a bonus available.

And then just do that on a year by year basis so you can track which card you or your partner had on a year by year basis and you know when to recycle through. So it’s just a matter of an Excel spreadsheet.

What I did is I dedicated 1 hour per week at the same time every single week to this. And so I would go in, I’d check the balances, pay them off, anything credit card or travel related, I did within that hour.

I did not allow myself to go out of that hour with anything. Makes sense. So if you want to be as aggressive as me, I found 1 hour per week will accomplish to me was worth saving $40,000 per year on purchases that I was already doing, but also saved me tons of travel.

Makes sense. So the Excel tracker kept you in line. Excel tracker. And then you were right about every chase. American Express, capital One, Discover. You know, I did have multiple logins, so I had those in an app that I paid for, I still have on my phone.

So the bottom line is the biggest mistake I hear is people say, oh, want to do everything through United? If you want to be an effective credit card gamer, you can’t be loyal to everyone. You’re going to need a loyalty code to every hotel brand and every airline code, because when you open these cards, you’re going to attach that to the credit card.

So it’s a little bit of work in the first year because you’re going to establish a preferred customer number, a rapid reward number with Southwest, United, American, British Airways, all these different airlines, but you’re going to then use that for the rest of your life.

And as you earn points and they transfer, it becomes easier. So the year one is front loaded. Year 1 may be 2 hours per week, but then after that, now I spend 15 minutes week. Makes sense. Okay. All right, next question.

Actually, I think, Ben, you brought this up, which is know people if they are not seeing their checking account balance go down or do they have the temptation to overspend or overextend and then subsequently get themselves in a pickle with their finances as a result of having a lot of credit line available.

Right, right, yeah. What is the psychology question? Spending on a credit card versus spending in cash or in a debit card, is there any differences there? Yes, I recommend so personally, I do not put every dollar towards the goal of this is put every dollar you can in trying to pursue a new bonus.

I do not do that anymore because that point it gets too cumbersome to track and then the psychology can take over. So I do have a reverse budget. So we’ll put a link to that in this where you have a fixed amount that you’re covering all your bills and you have a variable amount for all your fixed stuff.

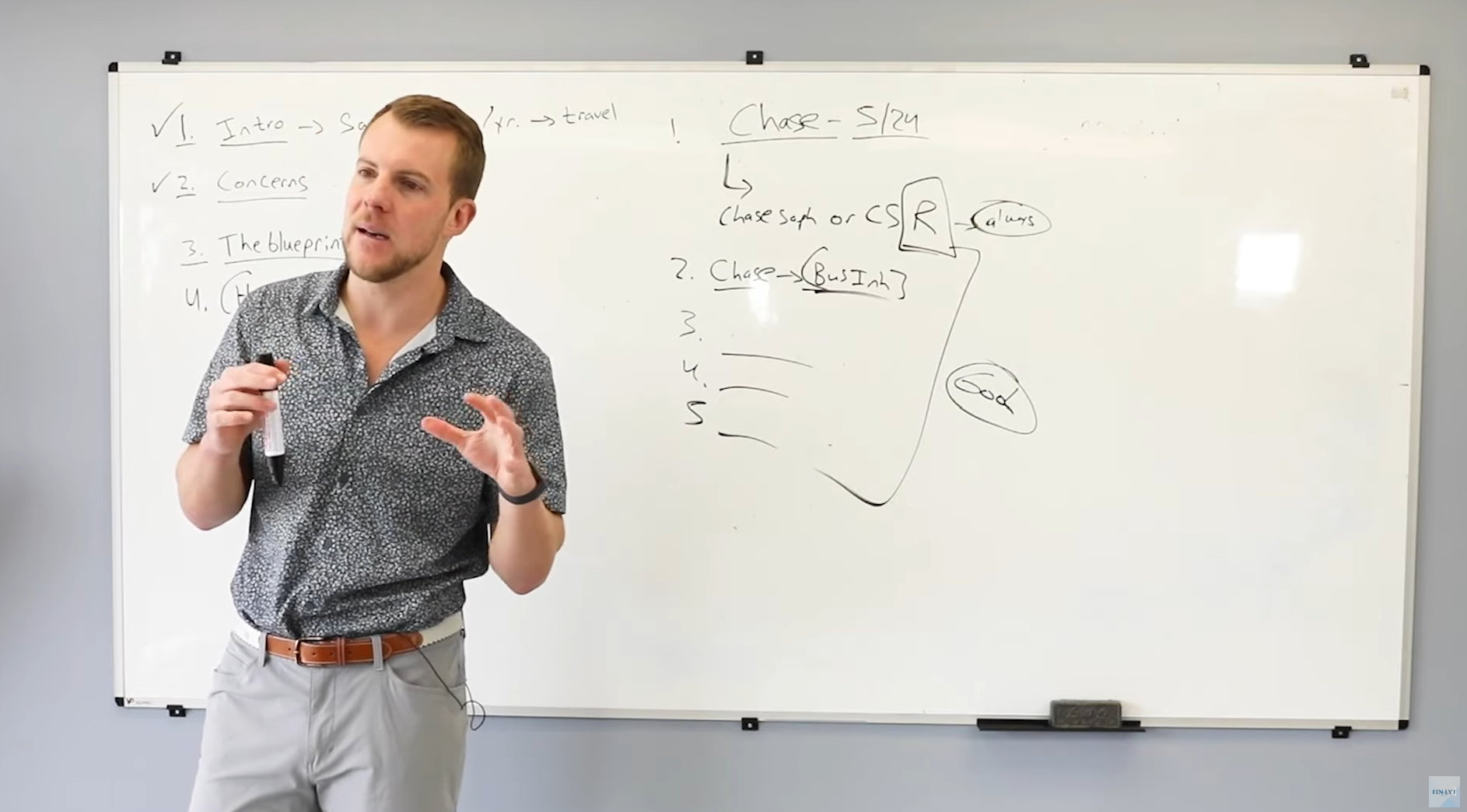

I would recommend that the bonuses that you earn should be only using expenses you’re already going to pay. So for an example, for a K one or a 1099, if you’re going to owe $40,000 of taxes throughout the year, that $40,000 for a 2% fee, which would be $800 can be run through.

That’s $10,000 per quarter. That can be split on three different credit cards each quarter. So that’s twelve credit cards we can get and. Each one of those will have a sign on bonus. We’ll say between 50 to 100,000 points, and we’ll just say 75 to keep these numbers simple.

So that’s 900,000 points. So hypothetically, if someone owed $40,000 in taxes and they decided, okay, I’m going to pay this taxes whether I like it or not, opening up three credit cards in quarter one, paying the tax on their credit card than paying cash to pay off their credit card, doing that in quarter two, quarter three, quarter four.

And if you’re married, the same tax return, same tax IDs flow through. So you can use your husband or wife or partner’s tax ID to go through. If you’re married to go through and hit your tax liability in that example, we can guarantee 900,000 points.

And if you just look at a conversion calculator right away, that’s worth $9,000. So you just paid $800 in fees. Each one of these is going to have an annual fee, let’s say of $100. So you paid $800 in IRS fees because they don’t want to be charged the credit card processing, so they’re charging that back.

And the credit cards are paying you $100 annual fees on average times twelve, so that’s $1,200. So the total this is costing you is 2000. If you just cash these points in, you’re getting $9,000 back.

So right off the bat, you just made seven grand tax free. So hopefully I don’t jinx this, but right now, points don’t get taxed. They’re not income. So that 7000 is really net of taxes, 10,000, that 900,000 points.

I can show you how to make that worth 50 to 100 in free travel cost if you convert them the right way. So that’s what you would do. So I would say from a psychology standpoint, let’s pick on Stephanie.

There’s no worries, Stephanie. Whatever your budget is, whatever your systems are, don’t change a thing. These credit cards you’re going to get, you’re going to pay your taxes on them. You’re not going to put.

Single purchase on them other than your taxes that will make it much clearer to track and it will not disrupt the systems you already have. Right. Any questions on that? No. That makes sense. So this is personally exactly what I do, and I keep my credit card from my personal that’s attached to my variable account, which keeps me in line.

I have the same card, and I have a credit card that we run through business here, and it’s the same card. We don’t get distracted by trying to get a new card and put new expenses and attach recurring bills.

That’s just a waste of time. This is not a waste of time because it’s just, boom, one transaction, open, earn points, close it. If I started putting personal expenses, it would be so disruptive my day, and it would take hours upon hours upon hours to do so.

That’s for a K one or w two? But Ben, does that address your concern around the reverse budgeting psychology aspect of getting sure. I think as long as it’s for a dedicated purpose, like you said, and it’s part of a system that’s being tracked, then the psychology of it is in line.

I think what you just said is so important. If there’s no system in place or expenses are getting mumbled together and overlapped, that’s where you could run into issues. But I agree with you 100%. Awesome.

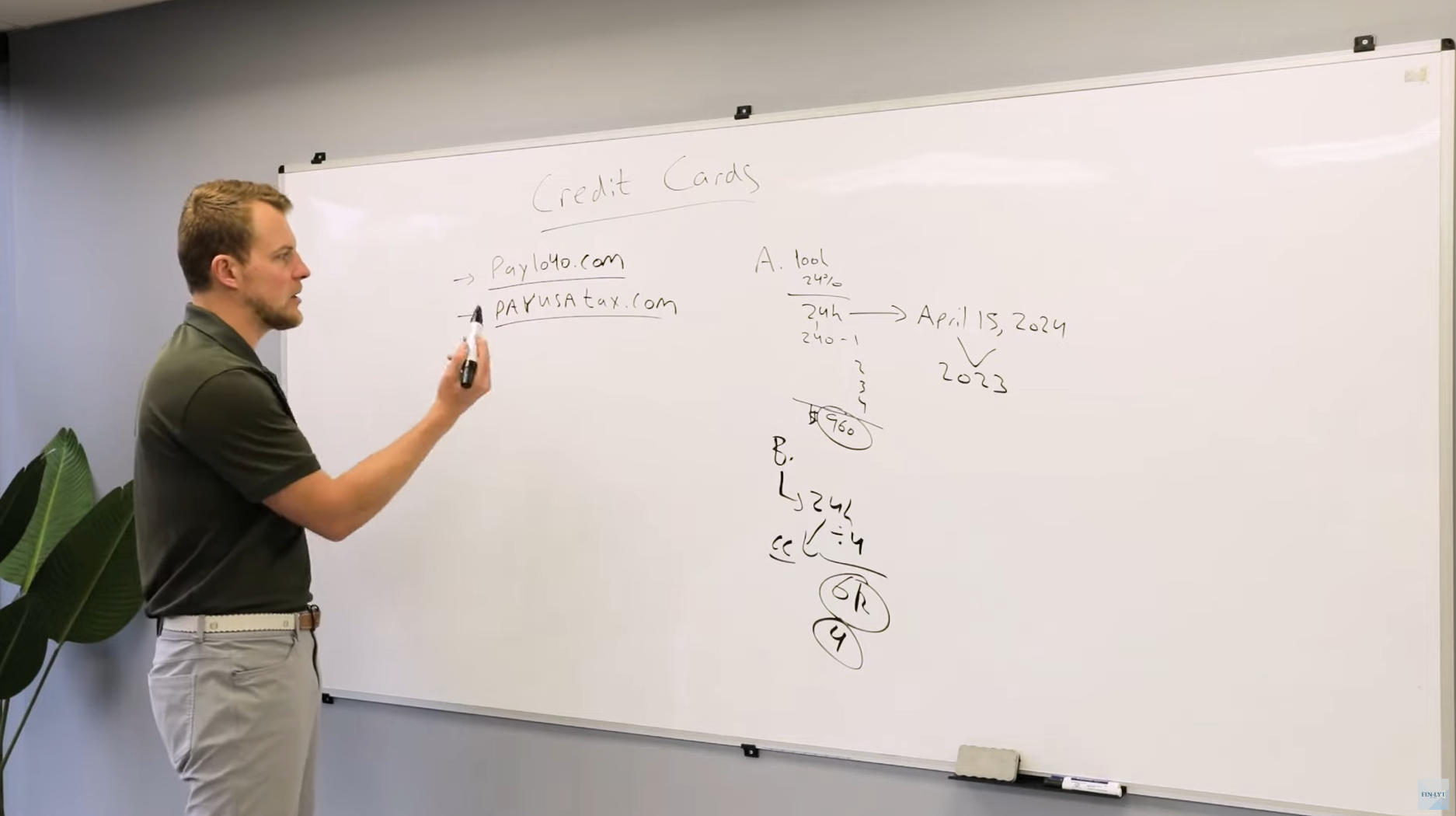

So let’s run through a W Two example because it’s a little bit different. So obviously your taxes are being withheld out of your paycheck. So one thing you could do as a W Two is you could just under withhold your taxes on your paycheck and then pay the taxes quarterly out of the extra money that went in your actual bank account.

So you can do this the taxing as a W Two employee, massively under withhold work with an advisor like Ben. Figure out the calculation. So if you owe 10,000 a quarter and you withhold five, that leaves you five that you can throw on the credit cards.

Same amount of money is going to the IRS regardless, but you’re just earning the points, right? Right. The other way a W two employee could earn is if you have a fixed budget and then a variable budget.

And so the variable budget we recommend maybe it’s 2000 a month and that’s going on a credit card anyways. I wouldn’t mess with any subscription fees. Like if you have like a Netflix or YouTube TV or whatever, just keep that on the same credit card.

But if you’re on average spending 2000 a month with doing traveling and dining out, there’s no work for you to swipe a different card out of your wallet when you’re out. So you can naturally I wouldn’t mess with the subscriptions, but my guess is at this spending level, you can hit six new bonuses throughout the year just with money you’re already spending.

Does that make sense? Yeah. The psychology is fixed because you’re limiting yourself. The credit card balances can only be attached to your variable checking account and then your fixed checking account, which covers your fixed costs, like your mortgage, your car payment, student loans.

These can actually get paid through a company called Plastic with a Q again 2% processing fee. But that allows these will not accept credit card payments for a reason. Because they don’t want to pay the fee, the credit card fee.

But Plastic will do that for you with a small fee, they charge it’s like ten or 20 basis points, whatever it is. They’ll charge you the 2% to then pay the money. You pay the credit card to Plastic, they pay the mortgage, the student loans, the car payments, et cetera.

So w two for could easily earn another six new bonuses. So in the example where I said Stephanie could get twelve ben, you could get twelve as well, just with your normal expenses. More tracking. But the goal here is to not disrupt what money you’re already spending.

It’s just to take the money you’re spending and you put it towards. Credit card bonus, and everyone knows what their time and how much they want to travel. I would do this to the extent where it’s actually worth the tracking and the time versus the free travel you’re going to obtain from it.

Sure. Any questions on that? No, that makes sense. Okay. All right, so next question. Yeah, and there’s something that I was thinking about as you were running through this, but how long does it take to fill out these applications for these cards?

What kind of questions am I going to be asked? What’s the process and timeline for applying for a card and then actually getting a card to spend so fast? But there’s just a lot of steps, hence the Excel spreadsheet is so key.

For example, you get the new bonus offer, your card gets recommended. We’re actually going to have a list of credit cards with the bonuses that you should get. That’s how we’re doing this course for free is actually we get affiliate commissions if you use the links that we have, win win, because they’ll provide the highest bonuses on the marketplace.

And then we’re able to continue to produce content like this for free. So two minutes to fill out the credit card. They’re going to ask for you, your social, your date of birth, your address, your rent payment, your income.

That’s it. You get approved on the spot, or they tell you you’re going to have a decision in ten to 14 days. Usually the card just gets approved and gets mailed to you unless you’ve opened up too many cards.

Unless I get declined. I know I’m not being aggressive enough. I just keep applying until someone declines me. But you know me. I’m very aggressive, growth minded. That doesn’t sound right. That’s how you use my credit card points, is aggressive.

So with that being said, it’s two minutes. But then once you get it approved, you need to activate it. That’s two minutes. Once you get it activated, then you need to hit the bonus. So if you’re using it to pay taxes, that’s probably five minutes to fill in all your tax information, and then.

You know, download the receipt, put it in. I have a dropbox what I put all my tax payments into, so I keep track of those in Excel spreadsheet as well. The actual time per card is probably two minutes here, two minutes here, five minutes here, another five minutes to get the loyalty program established.

But then the big thing is, though, this is exhausting. It’s not exhausting. Have the Excel spreadsheet with the fact pattern and the steps listed out? No, it’s all being tracked there. Trust the process.

You’re only looking at this once a week. It’s very little time. The steps will probably scare most people away. And why credit cards still allow these huge bonuses is not a lot of people are doing this.

But if you again, hard decisions, easy life, easy decisions. Hard life, easy decision is this is too complicated. Well, then you’re going to pay for travel or not travel. Hard decision is stick to the process.

Make your life really easy because you’ll travel the world for free. Makes sense. Okay, next question. Yeah, I think you already touched on this a little bit, but just how do you actually utilize these cards?

Like, and you said that you can pay taxes on them, big expenses. I’d never heard of plastic before, so that’s pretty neat. I think mortgages are probably most people’s hugest expense of the month, so that’s a neat thing to explore.

But any other tips on how you get up to those initial purchase requirements? Yeah, the golden age has passed. So there used to be if you really do some dig due diligence on this, you could basically just spend money in a circular pattern.

So me and my buddy would go to taught me how to do this, but we’d go to CVS and we’d buy the maximum amount of gift cards, cash gift cards, credit cards. There’s no fee to load them at the time. So we’d buy 30 grand of gift cards, and then we’d go on a website and we’d take the gift cards and unload the gift cards to pay back the credit card.

So it was just basically money that we didn’t spend. It went here and then it went right back. No money out of our pockets. Ever left in our bank account and we hit all the bonuses essentially for free.

They caught on that the golden age has now passed us. Got you. Now there are ways I’m not going to get into that. You could still purchase money and just have an exchange like that. It gets very complicated now and there is risk to that.

If that got shut down, we would be stuck with $30,000 credit card balance and a $30,000 gift card that we have to figure out how to use. So it is higher risk. So what I would recommend to do is just, again, utilize money that you know you’re going to spend.

So the two things would be taxes for everybody because everyone can adjust their withholdings and make those quarterly payments. You can make two quarterly payments per tax ID per quarter. So for you, Stephanie, that means you could make two per quarter or eight for the year.

You can also do that for your spouse. And if you’re married filing jointly again, everything is flowing through the same tax return. So you can get 16 credit cards opened, earned the bonus, flowing through on your tax return, just using taxes, the mortgage, everything else can go through a company.

There’s several websites that do this, but plastic with a Q is obviously one that you can earn it as well. Where I steer clear of is saying, oh, magically, I want to have that new toy that costs $20,000 and I can earn this.

Free travel. Don’t do that. If it wasn’t something you were going to do anyways, don’t do it for the sake of earning points. Can you pay state taxes or local tax that way? Or is it just Fed? Just federal.

And I wouldn’t mess with state or local any ways because the amounts are small, it’s not worth the time. So I just do federal. You only do federal with the credit card. Right. Cool. That’s helpful. Okay, next question.

Yeah, I know we talked about this a little bit when we broke down K One versus W two. Prepaying taxes on credit cards. And we talked about how some cards can have annual fees. Is there an annual fee that would be considered too high for this exercise?

Or should we only be looking at cards with no fees or very little fees annually when you open them? Just walk us through what we should be looking for in terms of annual fees with these cards that we’re opening.

That’s a great question. So that’s actually the most important. It’s like a veteran question, right? So what what I see a lot of people. So any good credit card is going to have a fee at least of $100 per year.

Don’t let that scare you because if you’re getting that for one year and you’re getting 100,000 or 50,000 points, we can show you how to make those points magical. Some credit cards, premium credit cards offer 550 per year.

So an example of this would be the premium credit cards like Chase, Sapphire Reserve, American Express, Platinum, are those worth it to get 100,000 points? When you say 100,000 points are only worth $1,000?

Yes, but you have to be a student of the game and know how to make those 100,000 points worth $6,000 in travel expenses. But you have to be okay paying the 2% to get the money plus the annual fee. Again, I probably pay a couple of thousand in credit card fees to the tax side of it and then probably a couple of thousand in credit card actual annual fees again.

So let’s say it’s 5000 all in and we’re saving 40,000. And I was going to travel anyways. It’s a no brainer, but those things do scare enough people away. Again, that’s why this still exists. So with that being said, my opinion is any annual fee is worth it in the year you’re earning a bonus because the bonus will always be worth much more than the fee.

Then the question is, is it worth keeping the card around? And the one card I have personally, I literally have one personal card open right now. That Chase Sapphire Reserve. It’s a $550 per year fee.

Is that worth it? Well, that Chase Sapphire Reserve. I get $300 back if I book travel on it. And obviously, I’m booking travel all the time. I get unlimited DoorDash delivery. Well, if you know me, I DoorDash probably five times a week.

That’s $50 a week. Times 50 weeks, that’s $2,500 I’m saving. So right off the bat, free, TSA free. It’s a platinum card for a reason. So if you’re utilizing it, I would pay $2,000 a year to keep my Chase Sapphire Reserve open.

No brainer. So obviously $550. What I wouldn’t do is open up ten cards that have $550 fees, get the bonuses, use the bonuses, and keep them all open. No, the nine out of ten are getting canceled right away after the first year, and you got to pay that first year no matter what.

Sure. Okay. Great question, though. Okay, any other questions? I think the only thing that I wondered is if I accrue all these points. I mean, if we’re paying taxes quarterly, I’m obviously paying them in the fall.

Do they expire in the calendar year? Is there a certain time frame in which I’m able to use them? Can you combine them, too? I mean, that’s really good question. Phenomenal question. So, absolutely, they can be combined.

In general, if you open a card, earn the points, and close the card, and it’s not tied to a specific airline or a specific hotel, you’re going to lose the points. That’s a rookie mistake, closing the card before you use the points.

However, if you open up a Chase card, that’s a Southwest card. Specifically, those points are now housed at Southwest. So I can open up a Chase card with Southwest Airlines, get the points, close the card, I keep the points.

Okay, so that’s again, repeat that. If it’s a general card, which are the best flexible at Chase points, you’re going to lose the points as soon as you close it, so do not close it. Or transfer them to a hotel or airline and then close it, then you won’t.

If a credit card associated with an airline or a loyalty program specifically doesn’t matter, you’ll keep the points no matter what, you’ll close it. In general, points can expire. I’ve never had them expire because as long as you show some activity on a yearly basis.

So, for example, if I have 100,000 points of American Express, I earn one point that year. I don’t lose anything. And usually they expire every couple of years. But don’t be a points hoarder. I earn them and use them right away because points, they’re tax free.

The whole purpose is to go out and travel, and it keeps me accountable to actually plan trips and to book them. Good balance they show chase are the best. Basically, it’s unlimited. I’m constantly opening up Chase cards, which we’ll get into Roles and the Blueprint in a second.

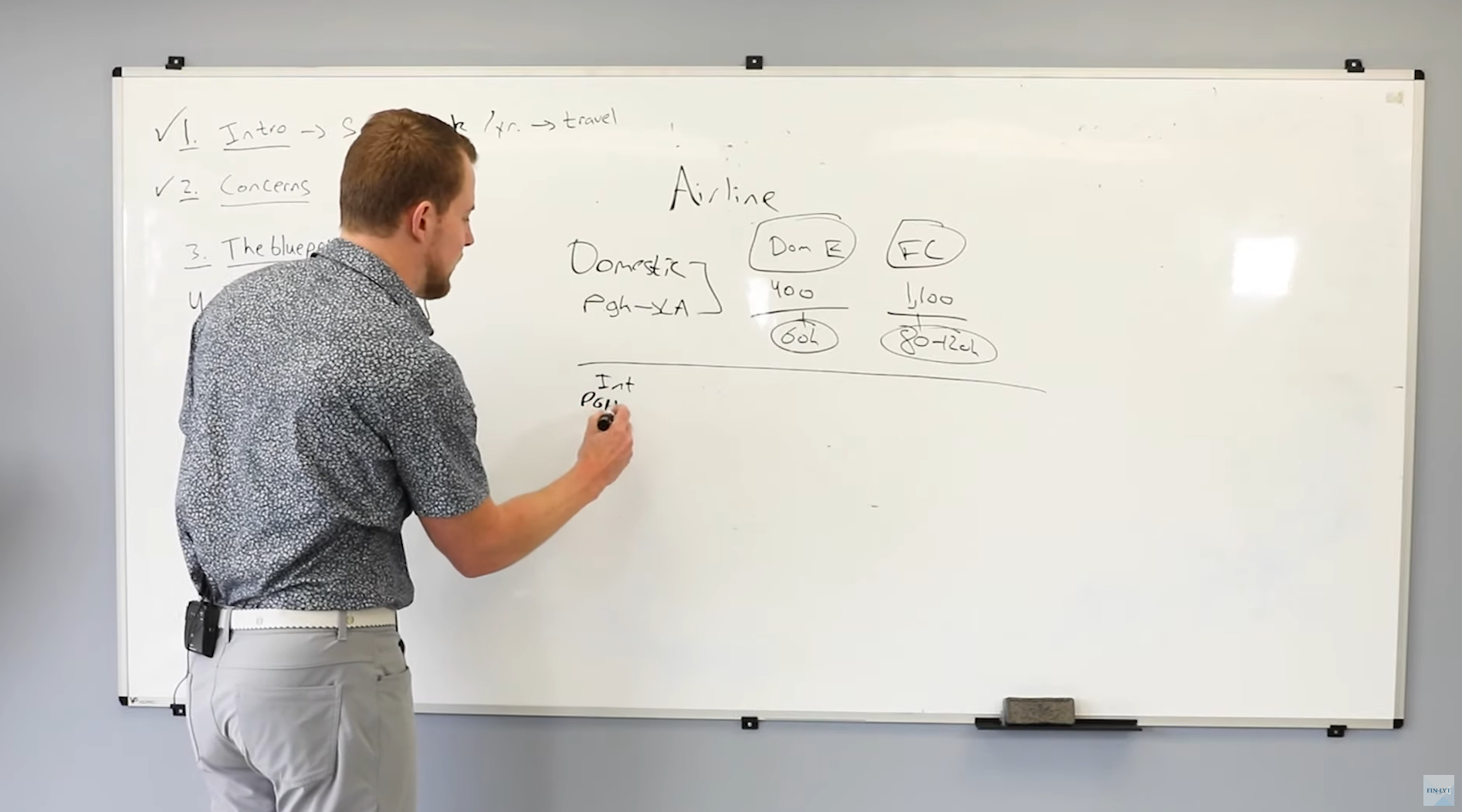

But Chase will transfer one for one to United, one to One to Southwest, one to One to Hyatt, one to one to Marriott. So it’s really flexible. If I want a hotel and I’m like I like the Hyatt. For example, I was in New York City, my girlfriend, a couple of weeks ago, we were looking at obviously we’re not going to pay for hotel.

The flight we already got for free there on Delta because it’s only direct from Pittsburgh, using points. And then we’re like, which hotel should we stay at? Should we pay cash? Should we not looking at the Park Hyatt One, $800 a night.

I was like, well, let me check the points. 20,000 points a night. I have a couple of hundred thousand Chase points. So we book it for three nights, 60,000 points. That would have cost almost $6,000. Totally free.

So obviously, deals like that where you can just know how this works. I didn’t have those Hyatt points. I just immediately transferred them that day and then booked it. It was like a two second process.

It was pretty powerful and cool what you can do. Same thing for the Bahamas. SLS has a hyatt. It’s all attached, 25,000 points a night. Usually it’s 1000 per night. 25,000 per night. We got three nights, 75,000 points again, all free.

So pretty powerful how far the points can go, if you know what you’re doing. Any other questions? Concerns? No, not on my end. All right, well, next video, we’re going to go through the exact blueprint how to get Stephanie and Ben to never pay for a flight or hotel ever again for the rest of their life.

Playlist

In 15 minutes we can get to know you – your situation, goals and needs – then connect you with an advisor committed to helping you pursue true wealth.

EWA, LLC dba Equilibrium Wealth Advisors, is an SEC-registered investment advisory firm providing investment advisory and financial planning services to clients.

Investments in securities and insurance products are not insured by any state or federal agency.

To view EWA’s public disclosure, registration, Form ADV and Part 2B’s, click here.

To view EWA’s Client Relationship Summary (CRS), click here.

COPYRIGHT 2024 EWA, LLC. ALL RIGHTS RESERVED