In this episode of EWA’s FIN-LYT Podcast, Ben Ruttenberg, Tyler Houston, and Matt Blocki walk through 10 essential guardrails designed to protect your financial plan and help ensure your wealth lasts. They explain why wealth rarely fails due to poor returns, but instead from a lack of structure, discipline, and intentional decision making.

From defining what “enough” truly means to maintaining proper liquidity, the conversation highlights common risks high earners face, including concentration risk, tax inefficiencies, and emotional decision making during major life transitions. A strong net worth on paper does not always mean financial flexibility, and without guardrails, small missteps can create long term consequences.

The team also covers tax aware planning, maintaining tax free asset buckets, managing lifestyle creep, and creating clear rules for big money moments like business sales or inheritances. Simple frameworks, like pausing 48 hours before major financial decisions, can prevent irreversible mistakes.

A great financial plan is not about chasing extraordinary performance. It is about protecting what you have built, staying aligned with your values, and living your life by design. If you want to pressure test your plan and put real guardrails in place, this episode is a must listen.

Speaker 1 – 00:00

There’s studies that show if you create your wealth, statistically you’re very likely to keep it. If you suddenly inherit

the wealth or win it in a gambling, statistically, you’re going to lose it pretty quickly.

Speaker 2 – 00:11

Just because a stock has done well for you for a long period of time doesn’t mean it’s going to sustain your

retirement. And I think it’s important as advisors to assess guardrails for their financial planning and make sure

that it aligns with the goals that are most important to you.

Speaker 1 – 00:25

Most people, even in the high net worth space we stand with, they don’t have a money problem, they have a

decision risk making problem. If you’re going to grow your net worth, what’s the trade off? Everyone’s trading off

time versus money or money versus time.

Speaker 2 – 00:34

A net worth could look one thing on paper, but they may not have access to a large majority of what their actual

net worth is.

Speaker 1 – 00:40

Illiquidity can be disguised as sophistication. That’s why we recommend a minimum. You have a third of your

asset base available tax free.

Speaker 3 – 00:46

If you’re ready to make a decision, take 48 hours and make sure you still want to make that decision in 48 hours.

Speaker 1 – 00:51

Meeting Title: EP 02_ 10 Best Guardrails for

financial planning F…

Meeting created at: 19th Feb, 2026 – 3:31 PM

1 / 13

Making sure that the wealth stays is very hard to do.

Speaker 2 – 00:55

These guardrails are meant to protect your plan.

Speaker 1 – 00:57

It’s going to prevent irreversible mistakes. Make sure that you’re staying on the right track throughout.

Speaker 2 – 01:06

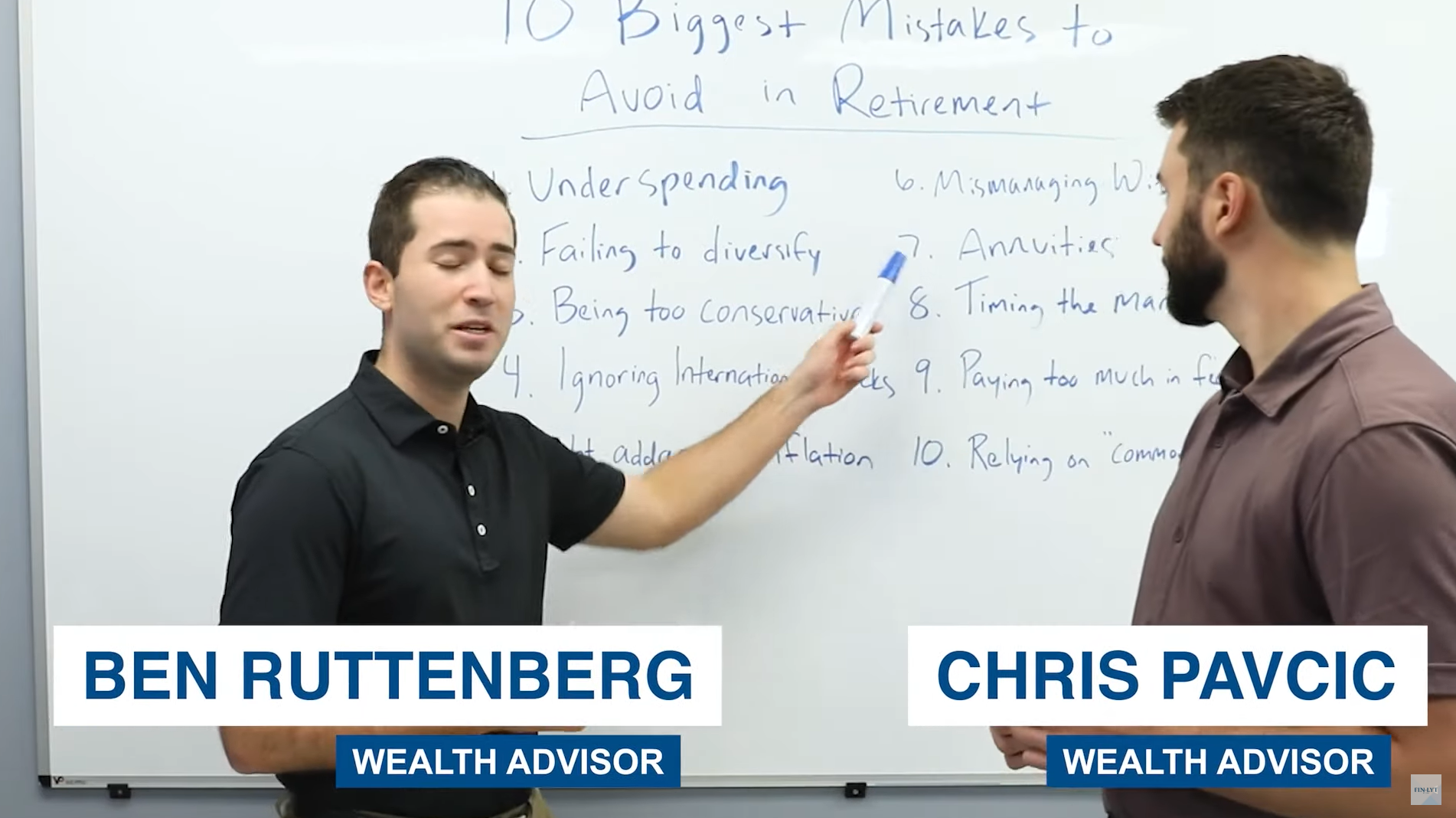

Wealth rarely fails due to a lack of returns. Oftentimes it fails due to a lack of guardrails. So today we’re going to

run through 10 guardrails to review in your financial plan to make sure that you’re living your life by design. So,

Matt, oftentimes we’re sitting down with a client. We have someone that has done a really good job saving

throughout their life, but it’s hard for them to turn on that switch and get to spending down what they’ve worked so

hard to earn once they’re in their financial independence years. And I think it’s important as advisors to assess

guardrails for their financial plan. Give them a sense of, hey, what does overspending look like for your situation?

What does underspending look like? And make sure that it aligns with the goals that are most important to you.

Speaker 1 – 01:47

Yeah, most people, you know, in the high net worth pace that we stand with, they don’t have a money problem, they

have a decision risk making problem. And so this one’s a big one because a lot of identity for high achievers and

high net worth are in seeing their asset grow. They’re probably tracking their net worth. They’re probably checking

their accounts, you know, multiple times a day. And so it’s almost like a competitive nature of like, what’s your net

worth, seeing it grow. So I think you know, guardrail number one is you have to have defined what is enough and

not saying you should stop growing your net worth once you have enough, but you have to have that philosophy

down of what’s enough. And then you have to have a financial plan that is dynamic, that goes along with that.

Right.

Speaker 1 – 02:28

Because like the lot of business owners that we’ve started working with, I was actually sitting down with a friend

yesterday for lunch. And I remember like 15 years ago, we’re sitting at Panera Bread and you know, he had like one

kid and he was making 80 grand a year. We had done this financial plan where he was like, he’s going to retire off

of 4,000amonth and fund 25% of college. He was planning on having three kids. Now fast forward, he’s well into

Meeting Title: EP 02_ 10 Best Guardrails for

financial planning F…

Meeting created at: 19th Feb, 2026 – 3:31 PM

2 / 13

seven figures of income. You know, the money temperature is like minimum 30,000amonth. And he wants to fully

fund like undergrad and post grad. And he has four kids now. And so the enough for him is definitely the goalpost

move from like just the 4,000amonth for inflation.

Speaker 1 – 03:06

I think he needed like two to two and a half million bucks to retire and now he needs like 10 to 15 million to retire.

So moving the goalpost I don’t think is a problem. But having defining enough, like if you’re going to grow your net

worth, what’s the trade off? Everyone’s trading off time versus money or money versus time. So what being

intentional about that trade off and making sure you’re not working to work, you’re not growing your money just for

the sake of growing money. It’s very intentional and it’s your money is there to support your life by design. And

you’re not going to have any regret with, you know, spending too little time with kids. I would say the opposite is

like too much time with kids.

Speaker 1 – 03:40

Because if you’re never working, like, what kind of example are you setting up for them when they graduate, Right?

So it’s this artwork that you have to hit, but you have to have defined. I mean, this one literally is the guardrail of

what is enough. And then calibrating that as you money temperature grows. Because if we had stuck with his

original financial plan and never adjusted it, he Would be five years of retirement plan for. So that’s obviously gone

up as he’s, as his income gone up. So yeah, that’s the first guard rule. What’s guardrail number two?

Speaker 2 – 04:05

Yeah, guardrail number two is just having enough liquidity. So oftentimes we’ll have clients that have a net worth

on paper. But a lot of it’s maybe tied up in a retirement plan that maybe they can’t touch until they’re old or they

have you know, money in a pre tax account that they’re subject to ordinary income tax when they take money out

or capital gains tax if it’s an investment account. So just making sure that you have enough money to support your

short term goals over the next 12 to 36 months proper liquidity.

Speaker 2 – 04:32

So whether that’s in money market, whether you have cash value inside of life insurance, whether you just have

money in your bank account, under your mattress, whatever it is, making sure that you have those tiers of liquidity

so that you’re able to not only withstand if there is a market drop over the next few years, but making sure that you

don’t have to sell anything at a loss if you’re anticipating a big purchase or if you have a goal plan that you’re, that

you want to fund soon. So that’s why that you know, sometimes you’ll see in this high net worth space. Oftentimes

people’s net worth is tied up in real estate, private investments, concentrated stock or you know, interest in their

business. Exactly.

Speaker 2 – 05:10

Meeting Title: EP 02_ 10 Best Guardrails for

financial planning F…

Meeting created at: 19th Feb, 2026 – 3:31 PM

3 / 13

So you know, a net worth could look one thing on paper but they may not have access to you know, a large majority

of what their actual net worth is.

Speaker 1 – 05:18

Yeah, listen, no judgment like at all. I mean we’ve, I have a client making $2 million a year that you know, needed to

call their, this isn’t a joke like their parents for you know, 15 grand because you know things were just, they had

done so many private investments, had a big house, they had. And so you know we see that, we see the business

owner’s business is worth $20 million that can’t make a tax payment because you know the like ebbs and flows of

cash in the business inventory, lines of credit, we’ve seen it all. So like illiquidity is not, it can be disguised as

sophistication. Look at all my cool investments and my private stuff. Liquidity is so important if you’re high income

earner. If you’re high. We’re not saying like keep everything in Cash.

Speaker 1 – 05:54

We’re just saying like if your general thumbs like you have to have six months of expense, you’re like why? It’s like

up my income. So life always surprises. You’re always gonna need more cash than.

Speaker 2 – 06:02

You think you are.

Speaker 1 – 06:03

So six months. And if you’re a business owner, I mean it depends on what kind of business you’re in. But I mean if

you’re, you should probably have like 5% of your net worth in something that it can’t go backwards and safe. So if

you’re not worth 10 million bucks, you should have at least half a million dollars. It’s depending on the business.

Maybe you need two or three million dollars, you know, because your divs inflow. So it’s really specific to the type

of line of work that you’re in, the type of business that you’re in and the current balance sheet that you have. But

liquidity is extremely important and it does look different from everyone.

Speaker 1 – 06:32

This isn’t just like a financial planning like cfp, you need three to six months bogus like you could need five years if

you’re a business owner of a hundred million dollar valuation and one day of the, of certain swings and certain

prices can affect that. So okay, so guard rule number three. You know risk defined by outcomes, not volatility. So

you know you have to have sequence of return risk address. It’s the biggest risk that exists for you know, someone

in distribution planning or running a business is you know the risk of the stock market is over history. It’s basically

over. You know, if you look at 20 year periods again based upon history, there is no risk.

Meeting Title: EP 02_ 10 Best Guardrails for

financial planning F…

Meeting created at: 19th Feb, 2026 – 3:31 PM

4 / 13

Speaker 1 – 07:10

There’s never a time period where if you’re invested in like large cap stocks over 20 year time periods in like one

year time periods, over a third of like a third of the time you’re going to depending on if you have cash versus the

cash doesn’t out perform the stocks depending on when you put it in. But over a long enough period of time, you

know, the risk gets basically eroded and then safer stuff in your mind over long periods of time becomes very risky

because like bonds have very big standard deviations of interest rate risk and inflation can erode your principal and

power. So you need to have your money really defined by what your goals are and what the outcomes that you’re

looking for are.

Speaker 1 – 07:46

And so you know, being risked to having a risk of selling good stuff at a bad time. It’s crucial to have a financial

plan to make sure that you know that doesn’t happen. Okay, number four is all around taxes. Tyler, let’s pass the

ball to you. Tell us about the fourth guardrail we have in place.

Speaker 3 – 08:01

Yeah, I think the biggest guardrail in my opinion, or one of the biggest, is actually tax planning as a core strategy. I

think a lot of clients, business owners, individuals think of tax planning as kind of like a different bucket. Where in

our opinion tax planning should be, you know, all encompassing. You should be thinking out from a tax standpoint

across every bucket, whether it’s estate, business, individual education, planning. You know, I think a lot of

mistakes or problems in a financial plan arise from not taking a tax conscious approach across the entire financial

plan.

Speaker 1 – 08:36

No question. And there’s so much leakage that can. I was just sitting down with a business owner client and so

he’d been audited, so he’s a little bit more conservative on the tax strategy. When you think about as a business

owner trying to save money, you know, if you’re 100, owner of a, of a small business, any profit essentially is going

to go to your tax return. And the ebbs and flows throughout the year can be really scary. So you can have all these

tax surprises. If you don’t have your books up to date, it’s really hard to save.

Speaker 1 – 09:02

You know, you’re maxed out your 401ks, maybe you have a pension plan, you have all these deductible stuff and

then let’s say you have a million or 2 million in profit and it’s, and your business demands, you know, growth and

capital and so taking money out, it’s basically like 44 cents immediately goes to taxes. It’s really hard to take chips

off the table when you’re in the high of a tax bracket and you have the businesses dependent on you and you’re

basically the bank of the business. Having tax planning and being able to make your plan efficient later, but also

super tax efficient now and just saving the time and stress so you can make the best business decisions by having

everything up to date and coordinated in one place is absolutely crucial.

Meeting Title: EP 02_ 10 Best Guardrails for

financial planning F…

Meeting created at: 19th Feb, 2026 – 3:31 PM

5 / 13

Speaker 2 – 09:39

And even just in the distribution phase, we’ll sit down with clients that have this. Oh yeah, we, you know, we have 3

million in an IRA. Well, it’s all, you know, is the 3 million in a traditional IRA that you haven’t paid any tax on yet or is

the 3 million in a Roth IRA that’s coming to you completely tax free? It makes a huge difference in terms of back to

guardrails like how much can you safely pull out? How much can you safely spend and maintain your goals,

sustain your lifestyle? Whether that’s spending and enjoying your financial independence, whether that’s leaving an

inheritance to your children or some charities, like, it makes a huge difference, the tax treatment of those

accounts.

Speaker 2 – 10:12

And so making sure that you’re doing a lot of that planning 10, 20 years down the road before you get to that point

where you’re financially independent is extremely important, because once you get to that point, it’s hard to wake

up in retirement, say, okay, now it’s time to.

Speaker 1 – 10:26

To do tax.

Speaker 2 – 10:27

To do tax planning like it has to be done.

Speaker 1 – 10:28

And Ben, that’s a good point. That’s why we recommend a minimum. You have a third of your asset base available

tax free. So that could be, you know, if you’re retiring with 6 million bucks, 2 million of that we want available tax

free. So that could be basis in a brokerage account, that could be, you know, cash value and a life insurance.

Hopefully that’s mostly in a Roth ira. But having that really allows you to navigate the sequence of return risk that

we talked about before and navigate, you know, filling money up at low tax brackets and taking money out and

avoiding high tax brackets.

Speaker 1 – 10:55

And so the decisions you make if you’re young for the next 20, 30, 40 years is gonna be crucial to make sure you’re

Meeting Title: EP 02_ 10 Best Guardrails for

financial planning F…

Meeting created at: 19th Feb, 2026 – 3:31 PM

6 / 13

in that minimally acceptable balance sheet tax situation where you at least have a third of your assets available tax

free at a moment’s notice. So, okay, well, that brings us to Guardro number five. So then concentration risk. Talk

about this. We see this all the time.

Speaker 2 – 11:14

Yeah, this is huge. And concentration risk, meaning too much of your net worth is tied up in one asset, whether

that’s, you know, your equity in your business, whether that’s a stock that you’ve held for a long time, whether that’s

in real estate, whatever. It is generally a good rule of thumb that we analyze for clients is trying to keep your, you

know, one position of your net worth less than 10% of your total net worth. So we don’t want one position to be

more than that. This can be difficult, particularly for a lot of executives that we work with that have a lot of stock

options and maybe equity in a company, you know, 25, 30, 40% of their net worth is tied up in this position. And it

can be really difficult to unwind that for a lot of reasons.

Speaker 2 – 11:57

There’s tax implications, there’s, hey, what are, you know, does this look bad if I start Taking chips off the table.

Obviously, you work at this company, you believe in the work you’re doing, so you want to have as much exposure

in it as possible. But at the same time, if things go south or things take a turn down, we don’t want your entire

financial plan to go down with it. So it’s a huge balancing act, making sure that you’re not overly concentrated in

one position. And that’s more so on the equity side. If you’re talking to a business owner or thing like that. But if

you’re just a investor, just because a stock has done well for you for a long period of time doesn’t mean it’s going to

sustain your retirement.

Speaker 2 – 12:34

So I think there’s a, you know, you don’t want to get emotionally attached to a company or a stock or a position.

Just because it’s gotten you to a certain point doesn’t mean it’s going to sustain your retirement. So it’s really

important to not let past results dictate future decisions. Try to remove your emotions as much as possible. As, as

difficult as it may be,

Speaker 1 – 12:54

A lot of times it’s not intentional. It just happens over time when stock performs very good. And you talked about

the loyalty factor, the political factors of the executive with the stock. And sometimes they are required to hold, you

know, 1x their comp in stock and it, again, it’s going to look bad and they’re looking for, you know, getting to the C

suite or it’s like, why can’t they feel like they can’t sell it? But this company is already paying your paycheck. You

know, it’s already so much tied into that we’ve seen honestly, like reverse. We want to see no more than 10% in a

concentrated asset. Whether that’s a stock, whether that’s hard to do if you’re a business owner, obviously, you

know, but most of the time we see if someone has a concentration. Prof. Is opposite.

Meeting Title: EP 02_ 10 Best Guardrails for

financial planning F…

Meeting created at: 19th Feb, 2026 – 3:31 PM

7 / 13

Speaker 1 – 13:29

They have 90% of their net worth in one thing, especially business owners. Sometimes we see it in a stock and it

should be, you want it reversed, you know, 90% diversified, 10%. But concentration is what get most people rich.

Diversification is how you stay rich, you know, essentially so. Well, let’s go to guardrail number six. So, Tyler, this is

all about spending guardrails. So talk to us about not budgeting. You know, rich people don’t really budget. Right.

How do, how do we navigate this?

Speaker 3 – 13:52

Right.

Speaker 2 – 13:53

No.

Speaker 3 – 13:53

Yeah, the Six guard is definitely in our opinion like spending and lifestyle discipline. So, you know, I think it gets to a

point where some clients like you might have 10, 50, 100, $200 million and the risk does like it’s really hard to

spend all of that money, right? Like you’re probably not going to spend all $200 million. But I think what is

important is I’m setting up some sort of, whether it’s a budget or a plan where I have a plan in place that if the

market drops 20%, I’m not stressed out, right. I want to have a plan in place where like there’s a safe bucket of

assets where I can access if the market’s down so I don’t have to take from depreciated assets during a time of

market volatility.

Speaker 1 – 14:30

The other thing I’m going to add to that, Tyler, is that I think you need to have the ability to say no. Because when

you’re talking about high net worth people, they’re getting pitched ideas all the time and a lot of times it’s friends

and family and so having. We don’t recommend a budget. I think that some high leverage tools you can do is doing

a past year and year, past year and review from a financial perspective. It’s like put all of your, get all your bank

statements, all your credit cards, see what did you spend? Does my fan financial plan address the spending? Am I

happy? Am I stressed about how much I spent? Don’t beat yourself up. You can’t get that money back. Do that.

Passing your review just to kind of get that new temperature gauge that you’re in.

Speaker 1 – 15:05

Meeting Title: EP 02_ 10 Best Guardrails for

financial planning F…

Meeting created at: 19th Feb, 2026 – 3:31 PM

8 / 13

Is, is my life require 20amonth? Is it 50amonth? Is it 100amonth? Are we going to have regret if we don’t spend?

Are we going to over accumulate if we have this and get that philosophy in place? But more importantly is set the

minimally acceptable savings goals to make sure that you’re on track for, you know, maximizing life today, but

financial security in the future for a defined time frame. I think even more important that the greatest risk to, you

know, spending guardrails is not that you don’t have enough money now that you don’t spend enough money is like

chaos that can occur if you just say yes too much.

Speaker 1 – 15:36

So you need to have a decision framework of how to say no and how to make sure you actually your balance sheet

works for you and you’re not working for your balance sheet where you have, you know, 10 different people all the

time giving you updates on these investments that are probably not going to hit, but they are going to continue to

ask you for money because their company isn’t doing well. And they’re like, well, if we just get this money, then we

can get to the finish line. Okay, so that brings us to guardrail number seven. Then this is around estate planning.

Speaker 2 – 16:00

Yeah.

Speaker 1 – 16:00

Walk through the importance of this.

Speaker 2 – 16:02

Yeah, estate planning. It’s making sure that all of your documents are aligned with your goals. This goes back to

just making sure that your goals are communicated. I mean, that is probably the biggest thing for people in the

high net worth space that are thinking about guardrails for their financial plan. It’s making sure that their wills,

powers of attorneys are up to date. Making sure, if there’s any trust planning, that all of the provisions are what you

want them to be. Making sure that assets are flowing to where you want them to flow in the most tax efficient and

the safest manner. Making sure all your beneficiaries are correct, your assets are titled properly if you are subject

to potential estate tax.

Speaker 2 – 16:38

Making sure that you’re doing the right type of trust planning to get some money out of your estate, if it makes

sense, but also making sure that you’re not, you’re still maintaining some flexibility and making sure you’re still

Meeting Title: EP 02_ 10 Best Guardrails for

financial planning F…

Meeting created at: 19th Feb, 2026 – 3:31 PM

9 / 13

maintaining some control of those assets. There, there’s certain trusts that allow you to do that. So that’s, you

know, I think the, the biggest thing with that is just communicating your goals. And that can be, that could be the

hardest part is trying to make sure that you’re balancing, enjoying your lifestyle today, making sure you have

enough money to sustain your financial independence. Do the things you want to do that you’ve worked so hard to

enjoy the time in your financial independence, making sure that your kids are taken care of, making sure that if you

have any charitable obligations, those are taken care of.

Speaker 2 – 17:19

So just weighing all that, balancing all that and making sure your estate documents reflect that.

Speaker 1 – 17:23

All right, let’s go to number eight. So, decision making rules for big money moments. So wealth is at most risk

during transitions. We’re talking liquidity and events, we’re talking inheritance, we’re talking career changes,

business sales. Yeah. So what are some of the guardrails we need in place for, you know, big decision making, big

liquidity events, et cetera. What do you guys think?

Speaker 3 – 17:41

Yeah, I think number one is, I don’t want to call it a rubric, but do we have an actual guideline in place where it’s like,

okay, If I want to invest a million dollars into this company, stock fund, whatever it might be, what does that look

like from, you know, what are the certain topics that, or pain points that have to, you know, maybe it has to meet a

certain threshold before I’m interested or feel comfortable making that investment.

Speaker 2 – 18:03

Yeah.

Speaker 1 – 18:03

And I think if, depending on the emotional aspects behind, you know, selling your business, if it’s a death in the

family and inheritance, it’s, I think it’s really important not to make any immediate drastic decisions is have a

cooling off period for, you know, three to six months. If you sold your business and you’ve this influx of cash, don’t

make any major purchases for the first three to six months because that’s going to really set the tone for the rest

of your life. It’s going to affect your money temperature for the rest of your life. And you know, we’ve done a whole

podcast on dopamine and how it affects finances. Once you set a baseline, it’s really, you need a new baseline to

feel that same effect. And, and that’s why people feel really good about a new car.

Meeting Title: EP 02_ 10 Best Guardrails for

financial planning F…

Meeting created at: 19th Feb, 2026 – 3:31 PM

10 / 13

Speaker 1 – 18:41

And then a week later it’s like the feeling’s already on. Right. So having coaching and having a philosophy and like

you said, a, a guideline decision process on how you make decisions over X amount similar as a business owner, a

gaff that remove bottlenecks and like any decision under a thousand dollars team members can just make without

your involvement on your own personal financial plan, there should be some card rail with it. If you make a

purchase above X or make a decision above X, here’s the process behind which we’re going to approach this.

Speaker 3 – 19:09

Yeah, I just want to, I think like for a lot of things like even if you’re buying car, like it’s like an age old tale, it’s like

just sleep on it, right? Like just sleep on that decision. Like if you’re ready to make a decision, take 48 hours and

make sure you still want to make that decision in 48 hours.

Speaker 1 – 19:22

So Ben, number nine is around gifting philanthropy.

Speaker 2 – 19:24

Yeah, we’ve done a few podcasts on this but this is a good guardrail just to making sure that you’re, you know,

giving within your means but at the same time balancing out, you know, your spending versus giving. So I would

say biggest things here would be, you know, things that we’ve seen done right is giving to the next generation while

you’re living so that your kids Grandkids can see the value of hard work. And you know, you can almost teach the

next generation the values that helped you accumulate your wealth. And also you can see your next generation use

the gift and help better themselves financially.

Speaker 2 – 19:59

So whether it’s gifting to children to help fund their Roth IRAs, fund grandkids 529 education plans, you know,

giving cash flow to allow your kids help max out their 401ks, you know, teaching them that financial responsibility

is extremely important. On the flip side of that, if you just don’t do any of that gifting, you die and you leave them

with a big pile of money, you know, are they going to be able to inherit that responsibly? Do they understand the

work and the value that it took to that, that you gained from that wealth? So we like that gifting while they’re living

so that you can see that money in action and actually teach them some of the values. And then on the philanthropy

side of things, intentional giving versus reactive giving is extremely important.

Meeting Title: EP 02_ 10 Best Guardrails for

financial planning F…

Meeting created at: 19th Feb, 2026 – 3:31 PM

11 / 13

Speaker 2 – 20:42

So just if you are going to be giving, make sure you are doing it in the most tax sensitive manner, you’re doing it in

the most appropriate manner. This is where something like a donor advised fund could make a lot of sense.

Especially if you’ve held stock for a really long time. This is a good way to get money into a donor advised fund.

Get an income tax deduction the year you make the contribution and then avoid the capital gains tax if you had just

sold the proceeds and donated the cash proceeds to charity. So again, we’ve gone in depth as to how those work

specifically. But this is just a really good guardrail to manage your philanthropy versus your giving.

Speaker 1 – 21:15

And I would say one high level guardrail is making sure that you’re the giving is the is leading the way. Like we see

a lot of like high net worth people get pitched with these different charitable ideas and they’re like we should do

this because it’s all these tax savings. Well, if it’s a tax savings, you even know what the charity is, probably not a

good idea. But don’t make sure you’re giving for the sake of giving. And then once you figure that philosophy out,

let’s do it the most tax efficient way because sometimes you can save 90 cents on the dollar. Like you said,

appreciate stock and get the tax write off 30% of AGI, no brainer through a DAF.

Speaker 1 – 21:44

But some of the times the fancier, more complex strategies you can accomplish being anonymous, saving the

maximum taxes through some, you know pretty basic strategies such as the donor advice fund. They’re not basic,

but they’re basic for us. But like some of the more complex stuff, you know, really think hard between is this what’s

the main goal here of the main goal is the charity and you know, teaching your children that can be accomplished

pretty simply and very tax efficiently. Last but not least is around ongoing oversight and accountability. So you

know, the idea of governance, this becomes very important the higher net worth you become because usually you

know, the higher net worth is driven by a family or an individual.

Speaker 1 – 22:24

And then once kids and other people get involved, there’s studies that show if you create your wealth statistically

you’re very likely to keep it. If you suddenly inherit the wealth or like win it in a gambling statistically you’re going to

lose it pretty quickly. So when we talk about high net worth and governments, the wealth is going to get spread,

you know, potentially between family members and new family members. And so making sure that the wealth

stays is very hard to do. But having the right governance and accountability and oversight is extremely important

to that.

Speaker 1 – 22:55

And so why we try to bring in, you know, family members and have these meetings to have a family constitution of,

you know, what’s our philosophy with how we treat money, how we give, how we save, how we, you know, what are

the card rails that you want to make sure and the values that you say are most important because that’s more

important than the money. And we’ll guarantee, I guarantee, ensure that the statistically the money is going to stay

there as long as possible versus it getting squandered or potentially you know, ruining some kids motivation. So I

think a real good way to put it is a good financial plan is not going to get the some crazy performance that can’t be

Meeting Title: EP 02_ 10 Best Guardrails for

financial planning F…

Meeting created at: 19th Feb, 2026 – 3:31 PM

12 / 13

repeated every year. It’s going to prevent irreversible mistakes and make sure that you’re staying on the right track

throughout.

Speaker 1 – 23:37

So any other closing thoughts?

Speaker 3 – 23:39

Tyler?

Speaker 2 – 23:39

Ben, these guardrails are meant to protect your plan as you stated earlier. So it’s making sure that everything that

you’ve said and you’ve stated from your goals are in line and are on track. So this is what like a team can do for you

is almost hold you accountable to the things that you’ve said were most important. So from a guardrail standpoint,

if you’ve said that, you know, enjoying your financial independence and spending what you’ve earned is a 10 out of

10 most important. And you’re not doing that. It’s up to. It’s up to your team to challenge you on that. And that’s.

That’s that constant oversight and constant accountability, making sure you have that partner so that you are living

the life that. That you designed. No doubt.

Speaker 1 – 24:17

No doubt. Well, thanks for joining us, everybody. I look forward to catching you next week.