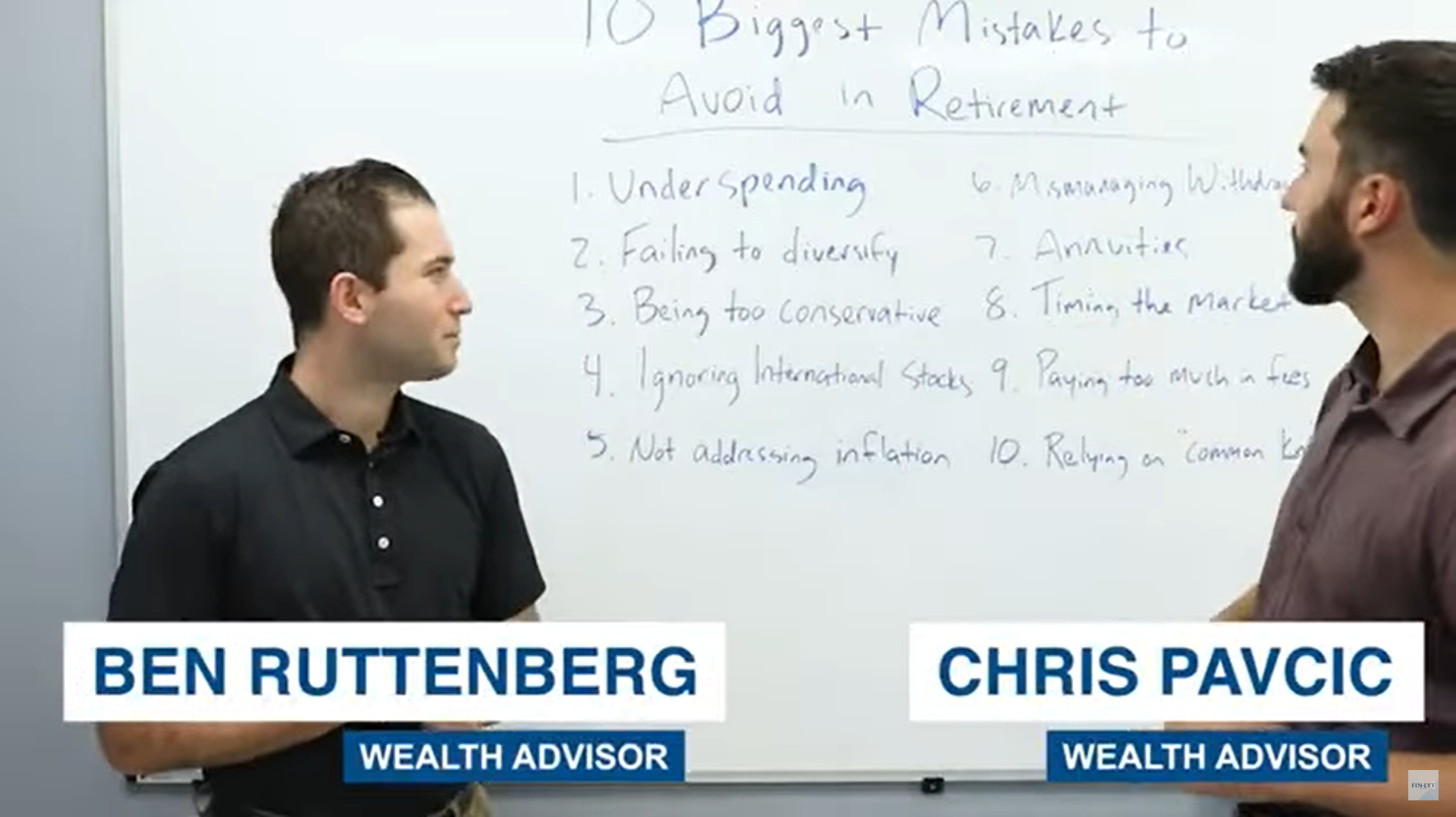

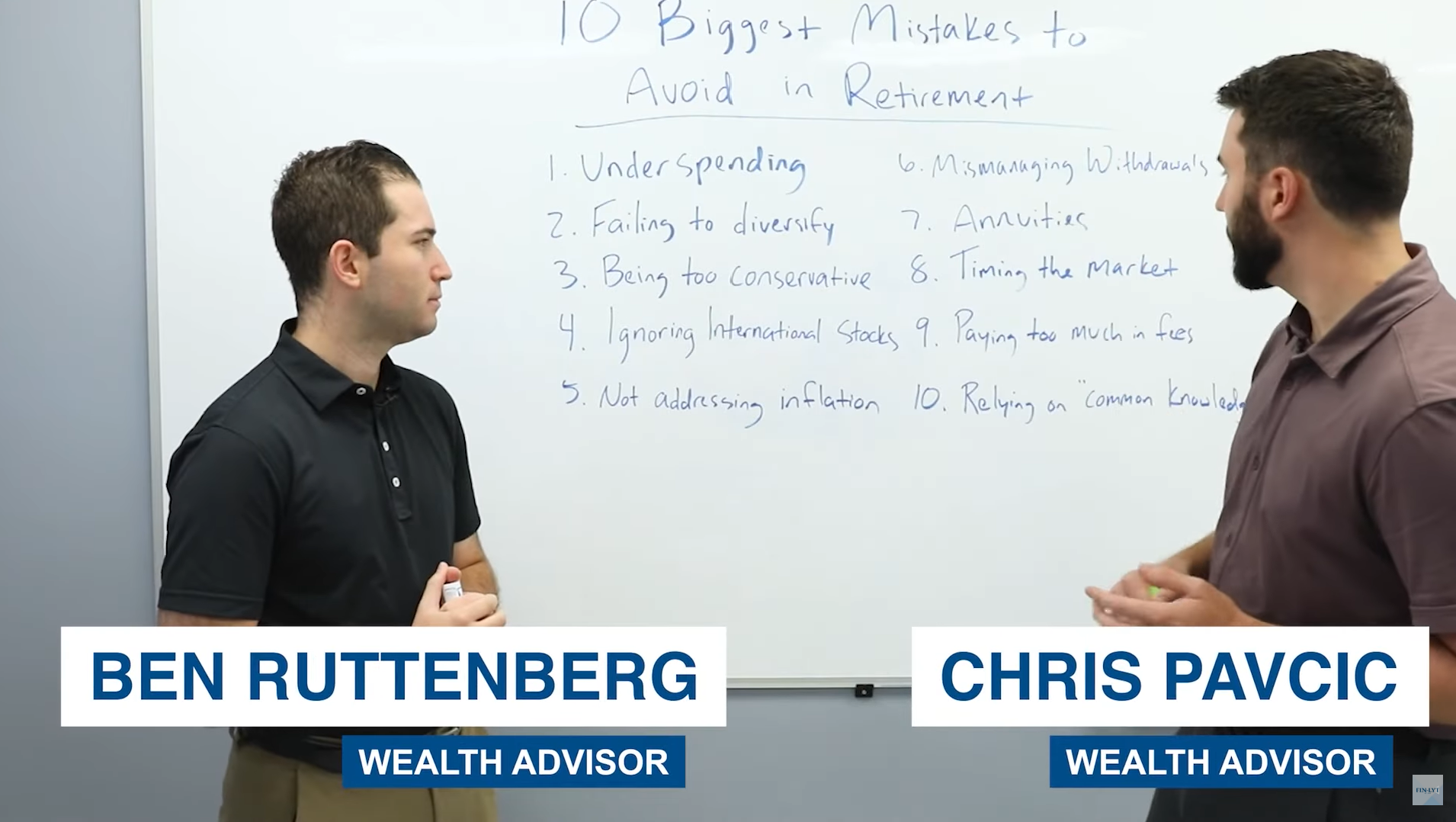

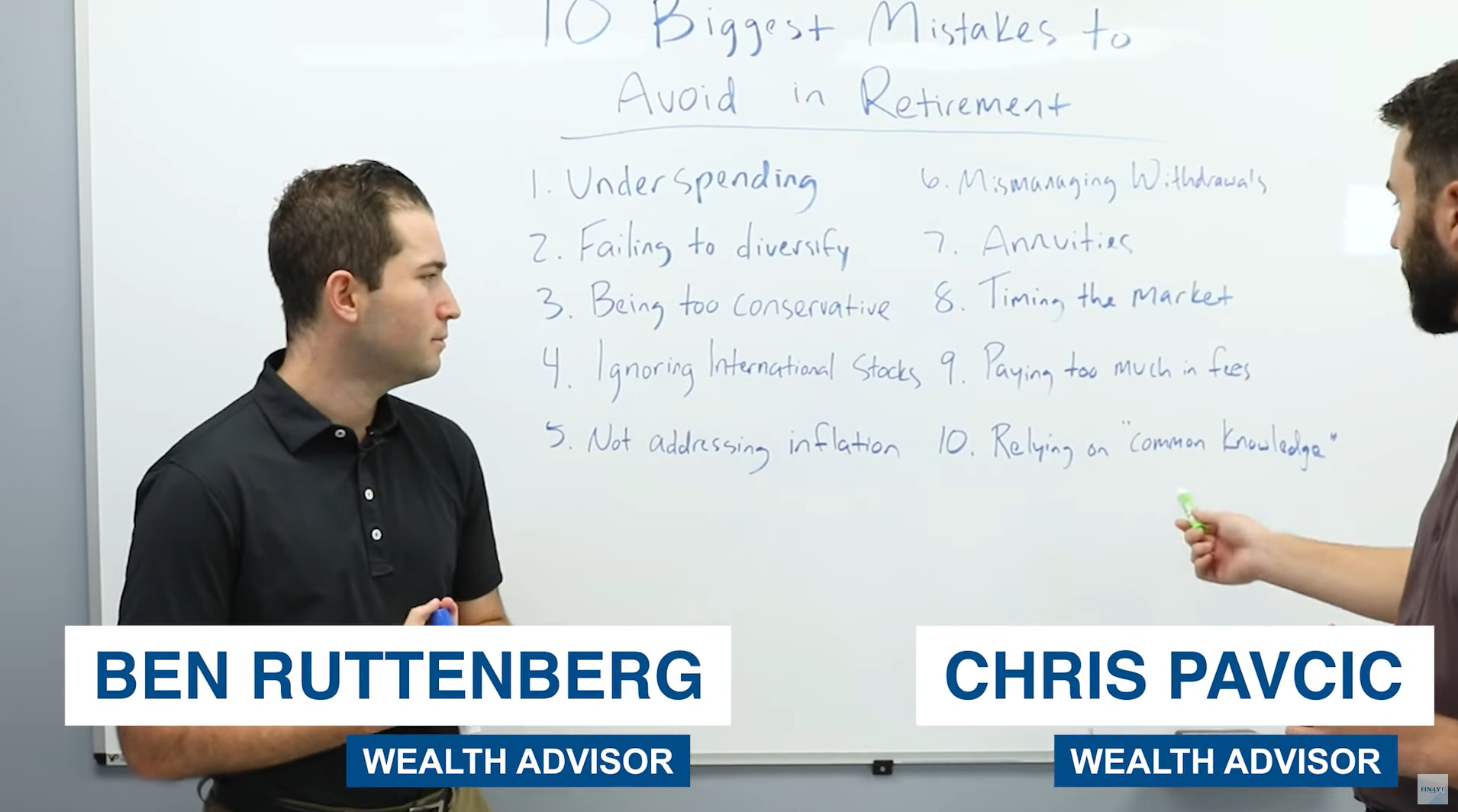

The 7th biggest mistake to avoid in retirement is annuities, but more specifically, owning an annuity for the wrong reason. There are many different types of annuities. There are fixed annuities, indexed annuities, variable annuities, and we have videos specifically breaking down each of these products specifically.

But to make a complicated subject as simple as possible, generally speaking, think of an annuity as the opposite of life insurance. So when you think of life insurance, you pay a little bit, you pay a little bit, you pay a little bit, and then you get a big check.

Annuity works the exact opposite way. You give the insurance company a big check, and then in return, you get a little bit, a little bit, a little bit back. That can be on a monthly basis, a semiannual basis, or an annual basis, depending on the terms of the contract.

So when we analyze annuities, there are typically a couple of issues that come up. First one being there’s a lack of liquidity in a lot of annuities. So there can be limited flexibility once you’re inside of an annuity contract.

And there can be very large surrender fees if you wanted to exit the contract early. The second issue being there are fees and expenses associated with annuities that typically cut into any sort of investment returns that make them not worthwhile products.

And then the third piece is that some annuities do not keep pace with inflation. So if you locked in a $1,000 a month payment from an annuity for a 20 year period, by the time those payments start, once inflation hits, if there’s not an inflation rider set on that annuity, that $1,000 a month payment is actually going to be worth $550 if we inflate at a 3% rate.

So we believe that owning an annuity should be done on a case by case basis only, after considering all of the factors that go into it.