Hi, Matt Blocki with EWA. Today we are talking about five tax tips if you’re a business owner. So as a business owner, I’m sure you’re aware you pay your fair share in taxes and as a business owner there are ways to be as tax efficient as possible.

So we’re going to be talking about some common tips and tactics and then also some things that you may have not heard about. The third tax tip is if you have a depending on the entity, if you have a sole proprietorship or a partnership or LLC, filing as an S corporation can be efficient as paying yourself a lower salary and a higher distribution would mean that you’re paying less in Social Security taxes, less in Medicare taxes and less in local taxes.

Specifically if you’re in a state that has local taxes, such as Pennsylvania, where we’re recording this video. So just as an example, if you’re a business owner in Pennsylvania making $100,000, that’s going to, as a sole proprietor versus an S corporation, a sole proprietor, everything flows through.

So you’re going to pay federal taxes on this and then let’s say the S corporation, you’re going to pay yourself a w two salary of 50 plus a dividend of 50 or distribution of 50. Federal taxes will be subject on both sides.

So we’re not saving in federal taxes. State taxes will flow through as well. So you’re going to be paying state taxes on the 100 here and the 100 here. Now, when it comes to Social Security tax, as a business owner, you pay the 6.2 on the employee side, the 6.2 on the employer side, a total of 12.4 here.

The Social Security tax does not hit the dividend side, but it does still hit the w two side. So the 12.4%. Is only effective on 50,000, but not effective on this 50,000. So right there, so 12.4% not having to pay down the $50,000 dividend, that’s a $6,200 savings.

Local tax, depending on where you live in Pittsburgh, could be anywhere between 1% to 3%. Again, the 1% will hit all 100,000 here, whereas the local tax, the 1% will not hit, it’ll hit the 50,000, it won’t hit the dividend.

There’s a $500 savings. And then the last thing is Medicare taxes, which again as a business owner, you would pay the 1.45 on the employee side, the 1.45 on the employer side, a total of 2.9%. That’s going to hit all 100,000.

Where the Medicare over here, the 2.9% is going to hit on the W two. You’re not going to pay that on the dividend. So that would be a 1450 tax savings. So all in all, a pretty significant tax savings.

Just as a quick recap. Federal taxes, there’s no difference. State taxes, there’s no difference. The difference here is the Social Security tax, the local tax and the Medicare tax hits everything. On the sole proprietor side, it only hits the W two.

On the S Corp. Side, the dividend, the distribution avoids those. It leads to an $8,150 tax savings just in this simple example. So the higher your salary is and then the lower you can make that salary in S Corp means the much bigger savings.

Keep in mind, Medicare is uncapped, local tax is uncapped, Social Security is capped. So there’s only going to be so much of a benefit on the Social Security side, which is the highest amount of taxes here.

Some downsides of the S Corporation. So this sounds like a no brainer, but some considerations are you do have to realize what is the audit risk of making your W Two salary lower? Obviously the IRS realizes people do this just for the sake of taxes.

They will look at your position. If you’re a physician at running a private practice and you’re a surgeon that would normally be making half a million dollars, they’re going to want to see your W Two industry standard.

So obviously you couldn’t pay yourself a $50,000 salary if you’re making $500,000. You could, but that leads to a high audit risk. And typically we recommend be above board and stay clear of any audit with the IRS.

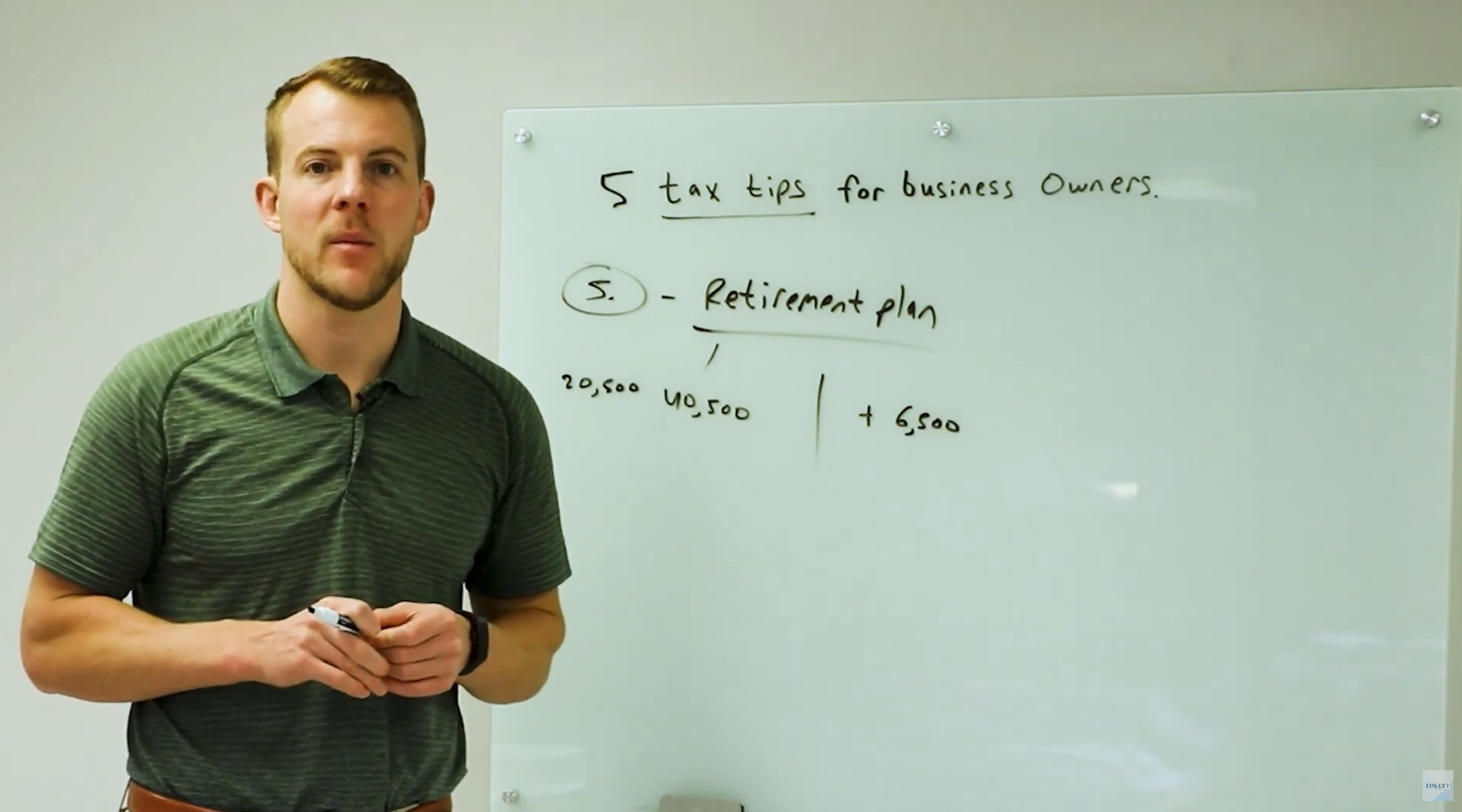

But if you’re in a position where it’s normal for the salary in your field to be 50,000s, corporation can make a lot of sense, but audit risk needs to be taken into consideration. The second thing is one of our next tax tips is going to be a cash balance plan.

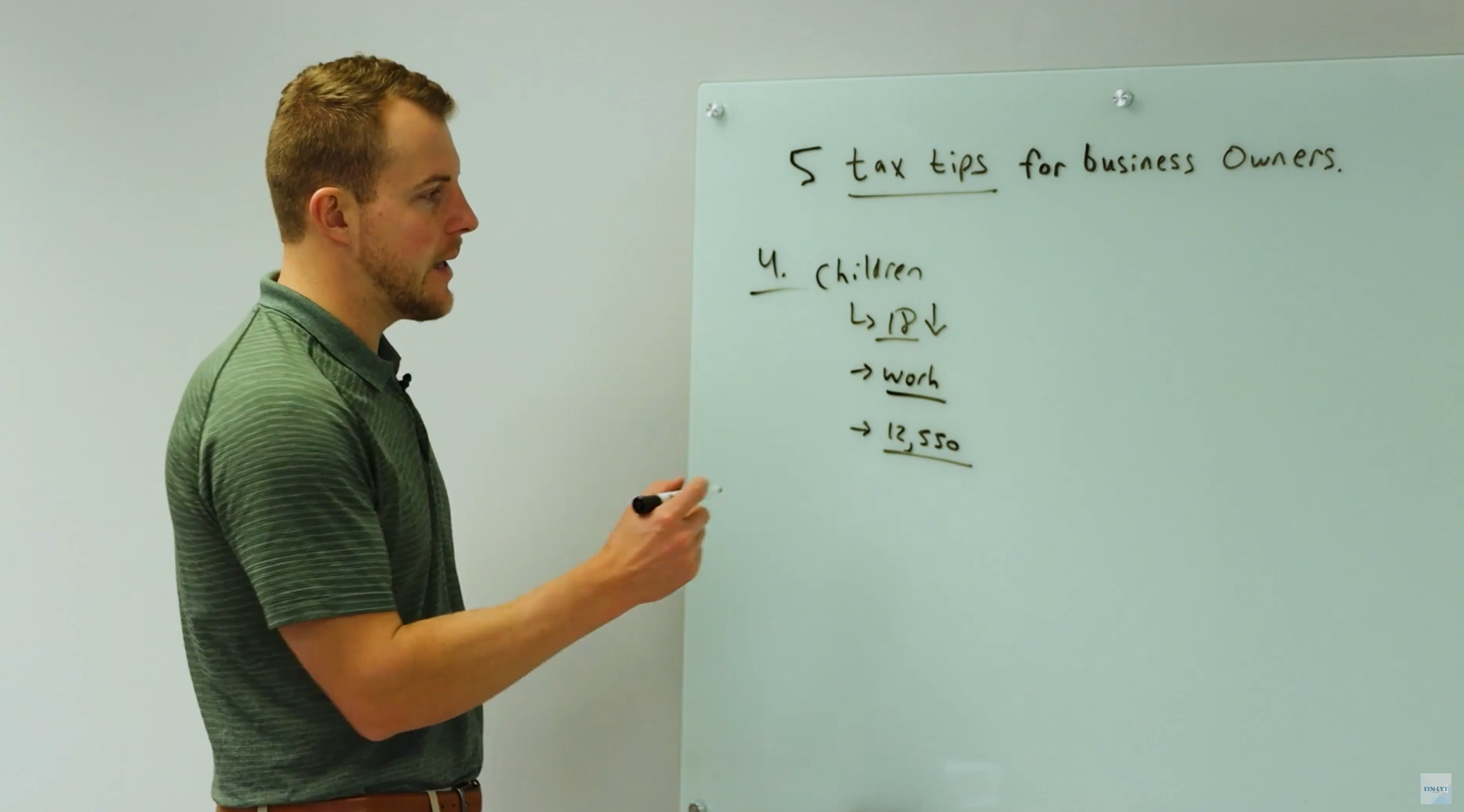

These calculations as a sole proprietorship are based upon your full income. If you’re doing an S Corporation, the W Two is what gets factored in to the retirement contributions. So the lower your salary is, that’s going to really limit your ability to put the maximum deferrals into the cash balance plan.

So it’s kind of a catch 22 because there’s a lot of tax savings here with the lower salary that may be offsetting the taxes you saved anyways. So that has to be very closely analyzed is what’s the net effect of, okay, I can do retirement plan, but now that I can do a lower retirement plan, am I offsetting what I otherwise would have saved if I kept things more simple?

Then the third thing is increased CPA fees. Obviously need to consult with your CPA who does your taxes. Does this make sense? But the increased CPA fees with the S Corp. They have to run payroll for you.

They have to file certain things with the IRS and typically the fees, if your normal tax return costs $500 to $1,000, this is probably going to be. About $2000 to $5,000 if you’re doing an S corporation.

So that obviously eats into the tax savings as well. Again, something we have to individualize for you. What are the savings? What are the pros and cons to this? But this is a potential avenue where you can save a significant amount in taxes.

These are our five tips for tax planning. Please reach out if you have any questions.