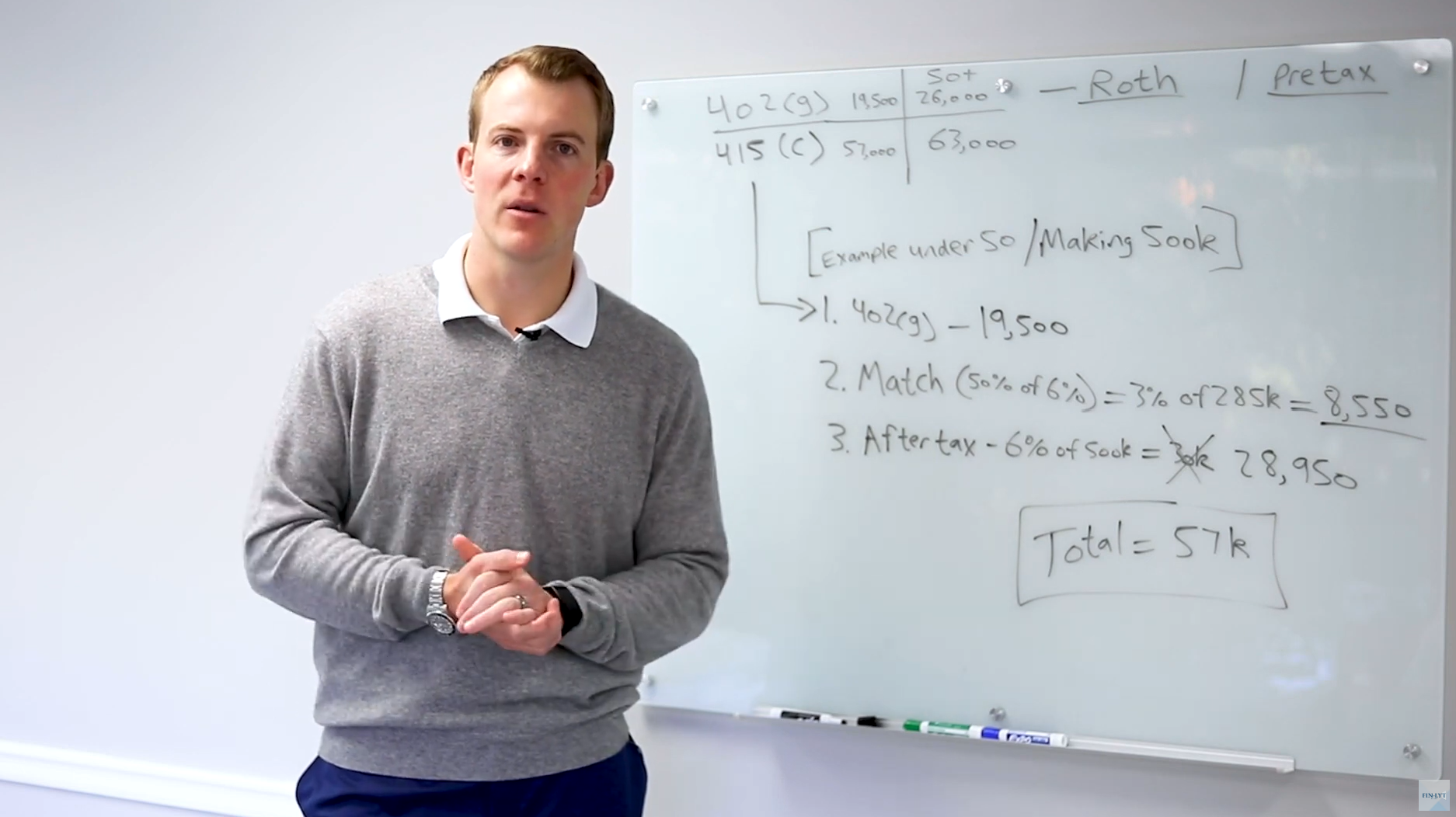

Matt stresses the importance of a robust investment philosophy amid market trends and decision fatigue. At EWA, four principles guide their approach: asset allocation, diversification, a long-term time horizon, and strategic asset location. Matt explains how these principles, like building a diversified football team, aim to achieve optimal returns with minimized risk. The emphasis is on maintaining a long-term perspective, discouraging market timing, and strategically placing assets in tax-efficient accounts for maximum benefit. The overall goal is to ensure that investments align with individual goals and lifestyles while optimizing tax efficiency.

Investment philosophy, this is more important than ever today, with decision fatigue and a new fad, it seems like coming out every week. Whether that’s a new coin, whether that’s a private investment, etc. We found is true. Wealth is built with sound principles, discipline principles, and really being patient over time. So here are four principles that we use at AWA to ensure that your money is working for you and your life by design, versus you having to change your life based upon what your money does or doesn’t do. The first principle is what we refer to asset allocation. So if I were to refer asset allocation as having one definition, it would be the marriage between trying to get the highest returns possible, but also with the lowest amount of risk possible. So think about a football team.

On a football team, we don’t want just quarterbacks. We want to have a quarterback, a wide receiver, a running back. We want to have every position to formulate this team. An investment portfolio is no different. Some of the categories we include would be large, mid, small, cap. Those would be all of our us based investments. Generally, this is going to be the majority of the portfolio. Usually for most, over 70% of the portfolio will be us based. Then the other 30% would potentially be international developed, and then emerging markets, which would be international, that are not as developed, such as european countries. Why this is important. As you can see on the screen here, this data shows from 2006 through 2020 on the top, real estate in 2006 was the best commodities. In 2006 were the worst of 2%.

But if you look at the rhyme and the reason between 2006 and 2020 over this 15 year, these fluctuations are very random and the averages are shown on the right. So the highest return from 2006 to 2020 was large cap stocks, which returned 9.88%. Let’s look at the risk of investing in a large cap. The next column was 15.12%. If we look at real estate investment trusts, for example, the returns over the 15 years were 5.78. The returns, or the risk, was the highest of 23.8%. That means you’re getting four times the amount of risk per unit of return. Asset allocation would be mixing all of these positions onto one team approach, which would be the gray, what’s referred to as the diversified portfolio. The average return over 15 years was 7% and the risk was 9.78%, measured in standard deviation.

Not the highest return, not the lowest risk, but the most efficient relationship between return and risk. And doing it this way is also an all weather portfolio. There’s a podcast we did specifically on developing an investment portfolio and being able to stay in regardless of what type of economy we’re in and get consistent, good compounded returns is what asset allocation is built to do. There’s no timing, there’s no worry. Once you’re in, you stay in. You stay disciplined with rebalancing and continuing to dollar cost average in as you go. If you’re retired, same thing, dollar cost averaging. The whole purpose of having these different categories is we have to pick and choose and never send your money back at a loss. You always have a gain available to you if you asset allocate properly. The second principle that we live by is called diversification.

Now, this is a build on of asset allocation. So diversification just means that every category we’ll pick on large caps. For example, we could invest in one company per category and technically still check the box of asset allocation. This could be home Depot, for example, or Apple stock could be our large cap. However, to properly diversify, I would describe that as think about a pencil. One pencil, you could snap in half. Now, if we diversify, we would want 100 large cap companies, 100 mid cap companies, 100 small cap companies. So think about having 100 companies at a minimum wrapped around 100 pencils wrapped together, almost impossible to break. 25 companies per position would lead to 80% reduction in risk. When we talk about diversification, if you go to 100 companies, it’s 90%. We can take 90% of the risk of the table.

Anything above 100 companies really doesn’t do us any good. So when you’re investing in a mutual fund that totes, we’re going to outperform the market. The more stocks they have, actually, the less chance they’ll have of outperforming the market. So the trick is getting diversification down, but also having the correct number of companies. And we prefer to not try to beat the market. We try to ride with the market through low cost index investing, or direct indexing that is also designed to mirror the indexes as tax efficiently as possible. But regardless of how that’s accomplished, asset allocation is key. Number one, diversification is key. Number two, key number three is a long term time horizon. So if you think about a casino, if you own the casino and you’re the house, you’re always going to win in the stock market, 75% of the time.

Looking at the s and P 500, dating back to the Great Depression till now, the returns compounded have been over 9% in the s and P 575% of the time, the market’s up, 25% of the market’s down. If you try to get in the timing game. You got to time it right twice and that’s nearly impossible to do and no one is able to do that consistently. So when you invest, we recommend the long term time horizon. Anything you put in the market has to have a goal attached to seven years or greater. So obviously, if it’s college planning for a kid, if it’s a retirement plan, the nice thing about financial independence or retirement planning is even if you’re retiring in under seven years, you still are going to have that money invested for life.

So we recommend always have a long term time horizon for equity investing of seven years or greater. Once it’s in, don’t worry about timing. It’s long term, it’s lifetime money, but always have a safe backup plan as well, not tied to the portfolio. So when equities are going down, you can protect the portfolio and let the recovery occur, but not question your lifestyle decisions and continue to live your life by design, even during those down markets. The fourth key to having an investment philosophy is what’s called asset location. So asset location just speaks to where we place our assets. And very simply, going back to the football analogy, if we have a quarterback and we decide to place him on the defensive line, he’s probably not going to perform well for us. A quarterback is meant to be a quarterback.

So in the world of investing, you have to look at this from a tax perspective. If you have a bond, corporate bond, that’s paying interest, and we put that in a brokerage account, you’re going to pay interest on that every year. If we put that same bond in a IRA, it’s tax deferred, you’re not going to pay interest. Same thing with a Roth IRA. Essentially, a Roth IRA is where we want to have all of our aggressive growth. We don’t care whether it’s dividends or just appreciation. All of the appreciation is there is going to be tax free, a 401K, if we do hold fixed income that’s pre taxed, that’s where we’d want it. And then in a brokerage account is where we would want growth stocks.

Because then you get the growth tax free and you only pay capital gain taxes when you sell out of the position. If you have direct index and you have tax loss harvesting, that can offset some of the capital gains owed on the growth in the end. So overall, we want to have a portfolio that has asset allocation diversification, a long term time horizon, but we want to view every account you have. If you have a Roth, a pretax, a brokerage account. All of those we want to view as one team, one household, and position the right asset allocation strategy into each one to maximize your tax efficiency, which can be, if you’re a high net worth investor, millions of dollars of difference over your lifetime.