Hi, I am Jamison Smith, a wealth advisor here at EWA. And this is a video that is part of our series, which is ten tips for anybody that’s in retirement or getting ready to enter retirement. So this tip is to make sure that you have seven years worth of spending in something that is a safe asset.

Reason being this will insulate you from any market downturn. So this is being filmed in November of 2022. There’s a massive correction in the equity markets. This year, it’s down over 20%. So really important that people that are in retirement now have this in place so they can avoid selling equities at a loss and jeopardizing the long term net worth of their portfolio.

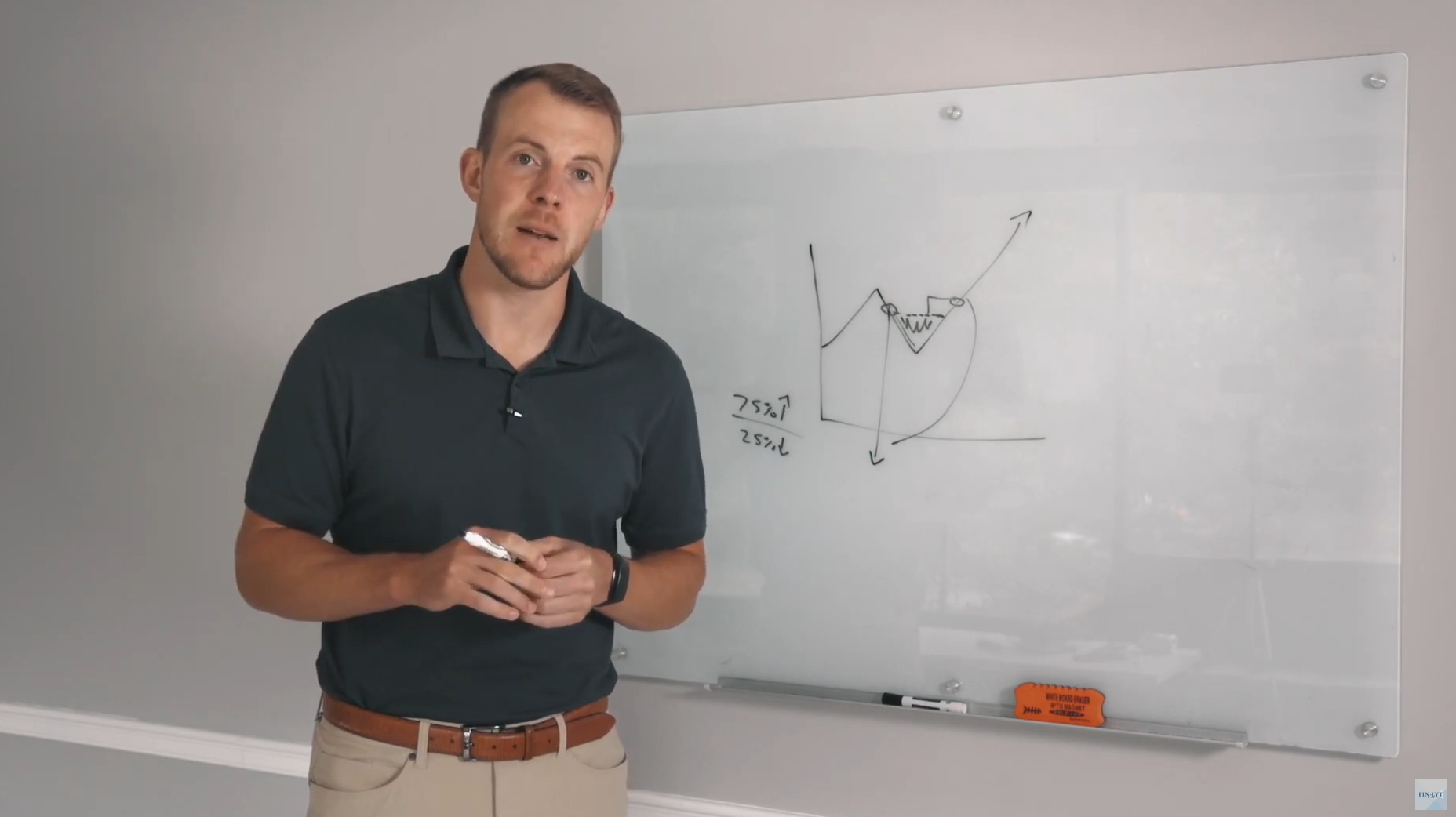

So what we mean by this is we want seven years of spending in something safe and that could be cash, something similar, fixed income bonds or cash value inside of a life insurance contract. Reason we pick seven years.

There’s no eight year period in the S and P 500 history where after seven years, the market is not higher than it was seven years ago. So if this would be extreme market downturn, but would get you through, you’d be able to weather any storm.

So an example would be if a client is spending 200,000 per year, once they’re retired, they may have 100,000 guaranteed from anything. Social Security, pension, maybe they’re working part time. This is guaranteed to come in no matter if the market’s up or down.

So we would now need to bridge this gap of 100,000, which is what they would be taking. Portfolio withdraws from your net worth is going to come into play with this a lot, but just generally speaking.

We would want this client to have 100,000, which is their annual spending times seven, which would be 700,000 in something safe again, bonds, cash value inside of a life insurance contract or cash. Something that not correlated to the equity markets that they can draw on and is liquid at any time, where they could avoid selling equities at a loss if are retired and they need income.

So having a seven year backup is one of the most important things in retirement. And this also gives a lot of clients peace of mind, knowing that no matter what the market’s doing, if it’s up or down, they’re still able to live their life by design rather than waiting to see what the market’s going to do.

If you have any questions about your situation, feel free to reach out.