In this quarterly portfolio and market update, Matt Blocki reviews the adjustments made to the EWA portfolio in Q1 of 2025, including an increased equity overweight from 1% to 4% following the removal of election uncertainty. The update emphasizes a bullish outlook driven by strong GDP growth, moderating inflation, and robust consumer spending. Tactical adjustments include leaning into U.S. equities, adding exposure to the momentum factor, and introducing a small allocation to gold to diversify against geopolitical risks. Changes in fixed income involve trimming duration and increasing allocations to high-yield bonds and convertible bonds. The video concludes with a review of portfolio positioning, including a continued tilt toward growth stocks and an emphasis on flexibility to adapt to evolving economic conditions.

1. Introduction (0:04)

2. Portfolio Adjustments and Market Commentary (0:40)

3. Economic Outlook and Supporting Data (2:17)

4. Focus on Specific Asset Classes: Equities, Bonds, and Gold (6:54)

5. Closing Remarks and Strategy Summary (8:42)

Welcome everybody. This this quarter we are publishing our video a little bit earlier because some of the strategy we’re putting in place right now for your portfolio was impacted by the election and so trades have already been placed. This video is coming out before quarter end, but please still expect your quarterly performance report to show up in the first or second week of January. At that point we will send you a reminder and that will be automatically uploaded to your vault. So in the meantime, just wanted to give you the rationale and recap Back in September Our rebalance We highlighted a cautiously optimistic outlook for the year ahead, but a desire to temporarily de risk as we waited for election anxiety to pass. With this uncertainty now removed, we’re leaning back into equities, moving them from 1% previously overweight, back to 4%.

S

Speaker 1

00:52

If you remember six months ago were 4% overweight. Prior to the election went 1 and now we’re back up to 4. This supported by a variety of positive data releases on earnings in the economy since September. So strong real GDP growth and moderating inflation are teeing up stock with a solid economic outlook on a go forward basis. Inside of equities, we’re leaning into the US and adding to the momentum factor. These are both largely due to stronger earnings and relative to their peers where earnings surprises have been unusually strong for the momentum basket. Relative to other factors, our signals also suggest that the current regime of low volatility, continued economic strength points strongly to momentum relative to any other competing factor. As part of this trade, we are also adding gold to the portfolio.

S

Speaker 1

01:33

Since 2022, many countries have moved to diversify their central bank reserves by adding to gold stockpiles. Central bank demand and shifting geopolitics have been on our radar as catalysts for the recent upward moves. Because we see these drivers persisting in the near future, we are tactically adding a slight exposure to gold in fixed income. We’re also trimming duration and buying into bonds with more upside potential. We’re adding to our existing convertible bond position that has performed well and given us exposure to thriving debt issuers. We’re also rotating slight into high yield where despite tight spreads we see attractive source of carry with strong corporate fundamentals. Both of these moves are helping us lower our duration during a time where longer duration bonds aren’t being rewarded with enough term premium to justify the rate risk.

S

Speaker 1

02:17

We are bullish going into the end of the year as we await the unleashing of delayed demand of business activity. Businesses often change their behavior heading into an election and delay decision making until they have a clear picture of the economic and policy landscape they will be navigating on a go forward basis. This means money was sitting ready to move before November and we can now expect that to be deployed in a wave of renewed capex spending. KPMG’s 2024 US CEO Outlook Paul survey showed that 62% of CEOs were delayed were delaying investments until after the election was settled.

S

Speaker 1

02:47

This has been corroborated by data from the Beige Book or PMI Surveys Key Bank Small Business Flash pool as well as reports in Atlanta and Richmond Fed we read this potential influx of investment into the economy as a strong positive signal for future earnings. We’re coming off a lot of good economic data moderating inflation, persistent real gdp growth and 4% unemployment. Business activity heating up tells us that this is likely to continue and provides an excellent backdrop for redeploying risk across the portfolios. A resilient US Economy coupled with a growingly accommodative Fed has propelled US Stocks into a historic bull market throughout the year. We positioned ourselves in a generally risk stance on the back of a strong economic data, and we’re reasserting that posture with a conviction here.

S

Speaker 1

03:27

Something were keeping an eye on this summer was Although we had good data, it started to surprise to the downside, the economic surprise IND as seen on the left turn negative despite good macroeconomic numbers. Those numbers started to come up shy of economist estimates. We tolerate negative surprises when the data remains in decent shape. Overall, however, a continuation of that trend could start to be worrisome. Fortunately, that trend of negative surprises proved short lived and just flipped back to the positive, reaffirming our confidence in the underlying fundamentals and giving us a bullish economic signal. As seen on the right, a large contributing factor the positive macro story has been the strength of the US consumer. Real consumer spending grew at a rate of 3.7% in Q3, the strongest reading in 2024.

S

Speaker 1

04:07

This tells us that despite widely publicized concerns about stretched consumer balance sheets, consumers are generally healthy and have actually been exhibiting positive momentum. We’ve also seen consumer sentiment rising again recently after moving down a bit during the summer, with consumer spending accounting for 70% of domestic economic activity. This upward trend is a great sign for economic activity and the markets overall. The elephant in the room for the economy has obviously been inflation. The Fed started an easing cycle in September that should be accommodated for growth and earnings that could change in the event they observe inflation’s core drivers start to stick or even reverse back upward. We’ve kept our eye on labor market tightness as an indicator of potential inflation. After the pandemic, demand for labor outpaced supply. The inflationary effects of this were resultant from employers bidding up wages to secure workers.

S

Speaker 1

04:54

In this chart you can see that quit rates increases when employees have more to gain from leaving. So we monitor quits as a predictor of whether or not employers are bidding up wages. Softening up the labor market such as slow tick up in employment or smaller payroll gains demonstrates that we’ve left the period of tight labor markets. Continuous upward pressure on wages would have been likely prevented inflation from moderating as much as it has this year. Looking at the bigger picture, a course of inflation drivers has significantly moderated goods. Inflation has not been a concern for a while. Shelter is continuing its long trot down and a slower wage growth is peeling back services inflation. Job moderation also gives the Fed more reason to cut despite focusing on prices for the last few years.

S

Speaker 1

05:33

The dual mandate of managing both unemployment and inflation is now top of mind for Fed officials. The numbers we’re seeing give the Fed a clear path to continue with stimulative cuts in order to lend some support in the labor market and hold unemployment near target. When we pull back and look at the full macro picture, we see an environment that is supportive of US equities and risk assets built on top of economic and corporate earnings growth following inflation and a Fed that is on a path to policy normalization. Looking at the charts on the left hand side we see real GDP which is growing at 2.8% as of Q3 and the chart on the right we show that Fed’s preferred metric of inflation core PCE, which is running below 2.5% year over year and 2.2% on a quarter over quarter basis.

S

Speaker 1

06:15

With inflation numbers running at 2 and real growth running closer to 3, this is a very positive backdrop for risk assets. That also rhymes with what we’re getting from the earnings data. Moderating inflation and economic growth have delivered a good year for corporate earnings. Inflation is no longer posting a significant threat to corporate cost while GDP is emboldening earnings growth. The main concern when the Fed started tightening was whether or not we would see a soft landing. Inflation figures have now moderated, many in arm’s reach of the Fed’s 2% target and real GDP growth doesn’t appear to have been sacrificed in the process. This is outcome that few investors anticipate and certainly one of the best case scenarios for U.S. Stocks. Conditions in the United States give us reason to be overweight in the region.

S

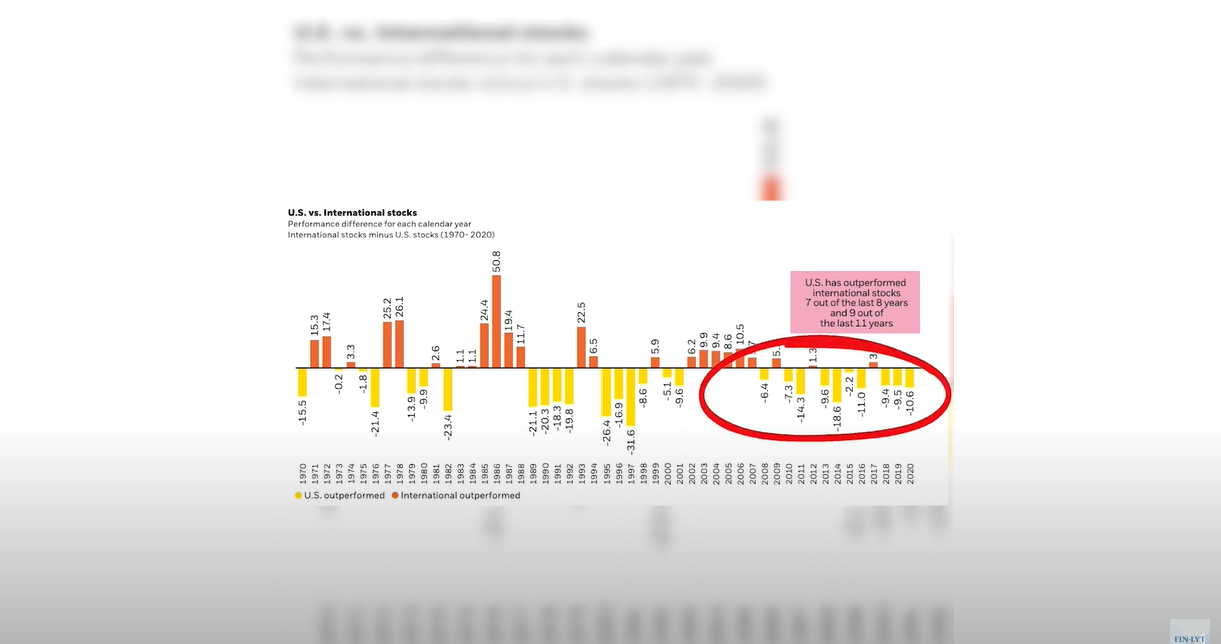

Speaker 1

06:53

U S stocks have broad outperformance over emerging markets and developed markets in recent years. With a better business environment forward earnings picture, we expect this trend to continue. One notable addition is the slight position of gold. So this rebalances a small allocation which were funding from the fixed income sleeve. As we see over variety of reasons to hold in the near future, A substantial trend in the international market since 2022 has been central banks looking to diversify their reserves and substantially increasing their purchases. In just the past three years, central banks have purchased more than 28 tons, an 85% increase from the three years prior. We are seeing this broadly across international central banks, perhaps in preparation for a world of slightly more unorthodox trade and to make their reserves more diversified.

S

Speaker 1

07:36

This is a trend we believe unlikely to slow and provides a nice tailwind for further price appreciation in the near term. A tactical allocation of gold offers portfolios diversification benefits with notable upside as well as opportunity to trim duration by funding this specifically from the fixed income holdings. In addition to what we’re seeing with central bank purchases, there’s also evidence that Fed rate cutting cycles have been supportive for gold. In this chart we look at the data going back to 1990 and we can see that on average gold experiences more than a 14% gain in the 12 months following the first cut. Fed cuts lower interest rates make non yielding assets relatively more attractive. This tends to increase demand for the metal and it’s complementary to the recent central bank and geopolitical forces moving gold higher.

S

Speaker 1

08:17

The bond market trying to anticipate the Fed path has always made gold attractive on a relative basis. Generally, the market grants a term premium, a reward for risk taking by lending long term instead of short term. And today the curve remains quite flat and there is a very little term premium available in the longer term fixed income. So this also creates a good entry point for us to fund this exposure again from fixed income. To put a really quick summary on the changes, with the US Presidential election now decided, market participants and economic actors can move forward with renewed clarity. The coiled spring of pent up business activities from previously postponed capital allocation decisions will now likely begin to release, providing a potential tailwind for risk assets as we enter the historically favorable November December seasonal period.

S

Speaker 1

08:59

Rather than attempting to thread the needle with bets tied to specific electoral outcomes, we’re positioned for a broader relief rally that we believe will transcend partisan results. So again, to Summarize, were 4% overweight previously in 2024. Prior to the election, were 1% overweight in equities and now we’re back up to 4% overweight in equities as a result. The second change on a high level basis is the introduction to gold. So the yellow metals impressive performance this year is especially noteworthy when you consider the strength of traditional economic drivers, notably interest rates and the dollar that usually act as headwinds. Historically, we have observed higher real rates and a stronger dollar putting downward pressure on gold prices.

S

Speaker 1

09:37

Our expectation of sustained central bank buying amid an increasingly complex geopolitical landscape reinforces gold’s role as a potentially attractive diversifier to our current stock bond positioning. Again, although a small position, this has been introduced and now implemented in your portfolio. Last but not least is our bond allocation shift. So our bullish positioning and further supported by an economy that continues to demonstrate impressive resilience, illustrated by a recent turnaround trend of positive economic surprises, robust consumer spending data. Yet we also see signs of sufficient economic moderation in areas like job openings, quit rates, wage growth. This all gives us confidence that inflation pressure has remained contained. This strong but not overheating backdrop should embolden the Federal Reserve to proceed with rate cuts.

S

Speaker 1

10:24

As you can see here, the risk gauge meter, you know, we’re kind of neutral prior to these moves and now we are leaning into risk, given all the things that we described in this video. And now that we’re past the election. The second thing is just the stock to bond ratio. So if you’re, you know, hypothetically an 8020 investor, you’re really going to be 84% equity, 16% bond. So we have the ability to go up 5 or down 5, depending on what macroeconomic and asset allocation views that we’re looking at the time. Then were looking at the duration, were a little bit heavier with interest rates have gone up, we wanted to lock in those high rates. And now the interest rates, there’s an expectation of some cuts.

S

Speaker 1

11:05

We’re going shorter term duration, so we have that flexibility now below that, as you can see, the credit, which would be a little bit of a higher risk in the bond market, we’re leaning more into risk to get higher returns to offset the lower duration that we’re incorporating in the portfolio. And then last but not least is the value versus growth. Traditionally, if we just look at the last 100 years, if you look at a value stock versus a growth stock, and just to repeat, a growth stock would be something like Apple, Google, Tech space right now. And a value stock would be like a utility company that’s paying a dividend for the last couple of decades. More mature companies these two types of investments have performed very similar, assuming the reinvestment of dividends on the value side over the last hundred years.

S

Speaker 1

11:51

But during certain decades and periods of business cycles, growth can sometimes outperform value can sometimes outperform growth, and there’s a risk appetite. Sometimes growth can be less risky than value, and vice versa. Based upon those factors, we have both in the portfolio, but we have them separated out. That gives us the ability to tilt towards one that we think is in favor and tilt out of one that’s out of favor. We’ve always been overweight for growth, which has really helped the portfolio with outperformance over the index the last couple years. But you can see we’re leaning even more into a tilt towards growth in the upcoming as a lot of these tech companies have continued to outperform. You know, their estimates from an earnings per share perspective on a quarterly basis. That wraps up this quarter’s video.

S

Speaker 1

12:38

Please reach out if you have any questions, and we’re excited to discuss this with you during our next review meeting.

Sync with audio