17 Categories

5 Videos

11 Videos

19 Videos

10 Videos

17 Videos

3 Videos

9 Videos

26 Videos

30 Videos

41 Videos

7 Videos

14 Videos

12 Videos

4 Videos

10 Playlists

0 Videos

187 Videos

20:24

10 Tips for Orthopedic Surgeons

9:48

10 Tips for Small Business Owners Profiting Over $1 Million

4:12

Maximizing Lifetime Gift Limits Before the 2026 Shift

5:30

Financial Independence and Legacy Planning Through Lifetime Gifting

5:51

Pros and Cons of Gifting Your Home While Living

Strategies for Safe Money All Stages of Life

11:24

Is a Roth Conversion Right For You?

4:53

Tips for Homebuying To Avoid Financial Stress

6:42

An Update to Our Direct Indexing Program

7:14

Superfunding Vs Annual Funding 529 Plans

5:36

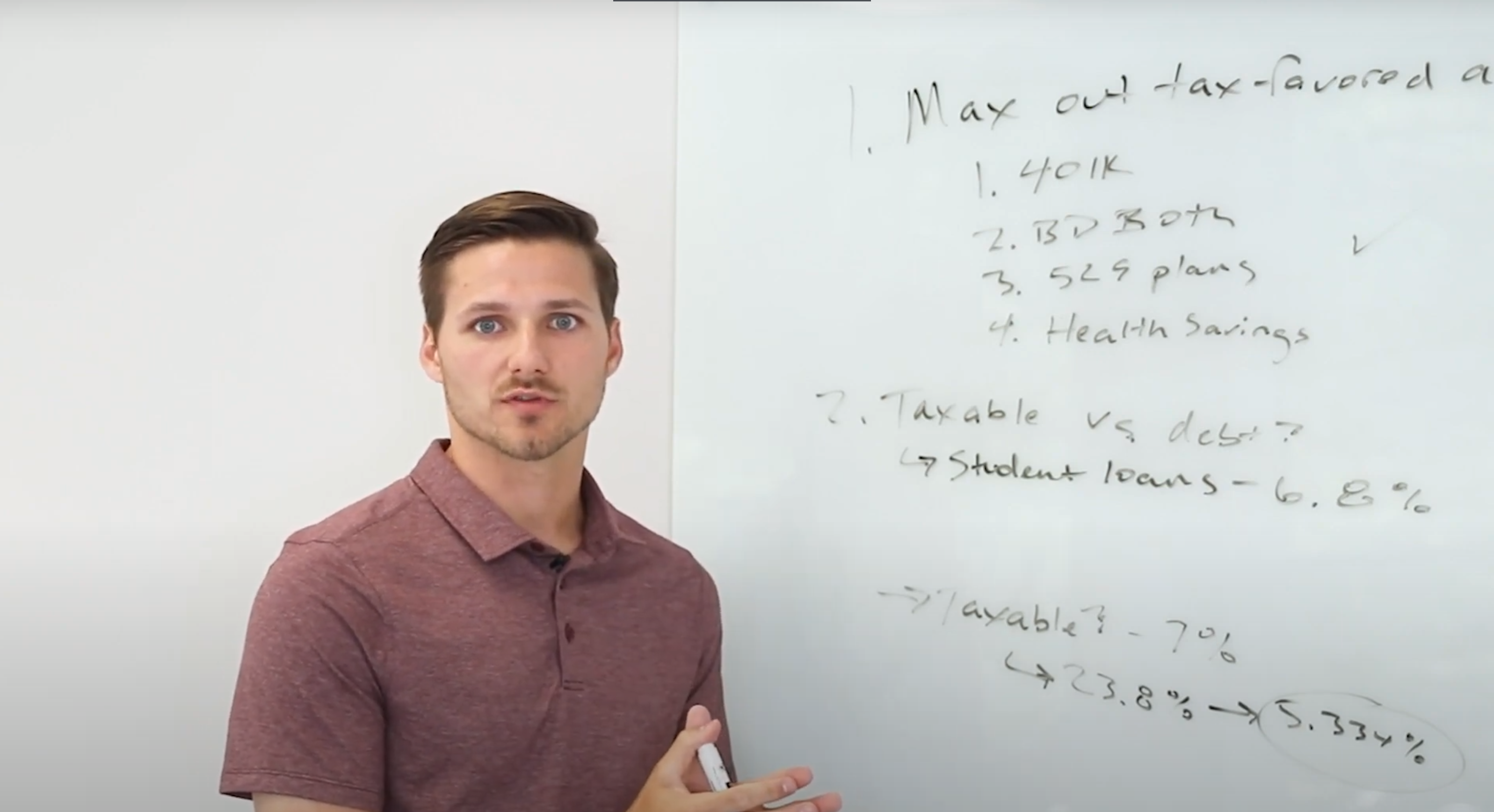

Strategies for Maximizing Your 401k in 2024

6:18

Buy or Lease: What is the Best Car Ownership Strategy for You?

6:32

Build Tax Free Wealth with Back Door Roth Strategy

5:20

The Best Credit Cards for Travel Rewards

3:53

The Power of Portfolio Diversification

5:56

A Deep Dive into Paychecks, Taxes and Savings for High Earners

8:08

Protecting Your Family With Estate Planning

8:36

Welcome to Equilibrium Wealth Advisors

6:19

Maximizing Investment Returns with Tax Loss Harvesting

6:00

Managing Bond Investments Amid Market Volatility and Rising Interest Rates

6:17

The Power of Diversified Asset Allocation vs. S&P 500 Investing

3:25

What is Quality Investing?

3:47

Why Index Investing Statistically Provides Better Returns Then Individual Stock Picking

3:10

Maximizing Long-Term Wealth: Compound Interest vs. Simple Interest

3:05

Maximizing Returns with an All-Weather Portfolio Strategy

8:31

A Promising Outlook for Investors in the Coming Years

7:25

Master the Art of Reverse Budgeting

6:50

Unlock 10 Key Stress Tests for Your Financial Plan

9:50

Surprising Lessons on Financial Returns, Risk, and Long-Term Planning

11:54

What You Need to Know About Spousal Lifetime Access Trusts (SLATs)

5:01

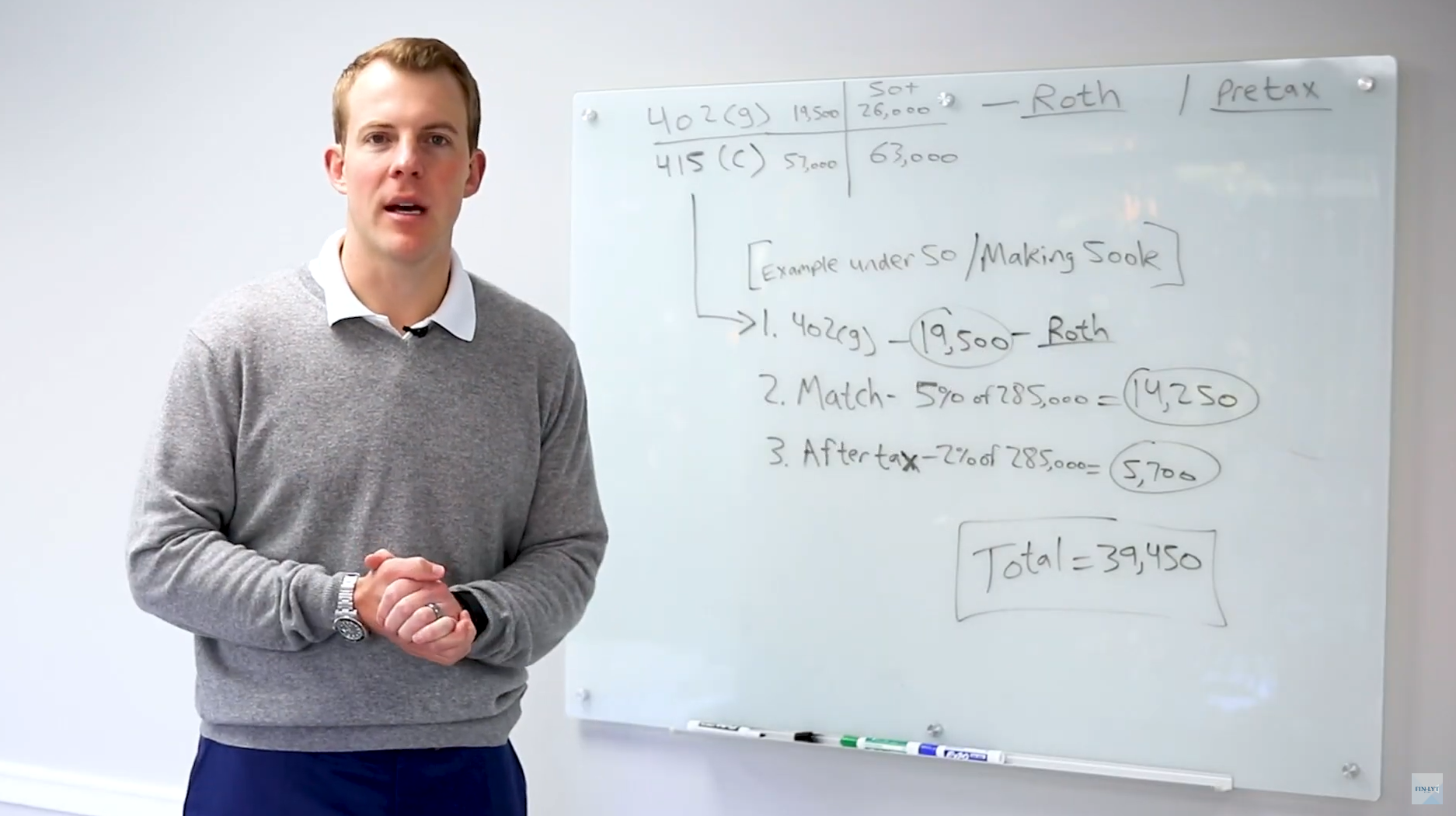

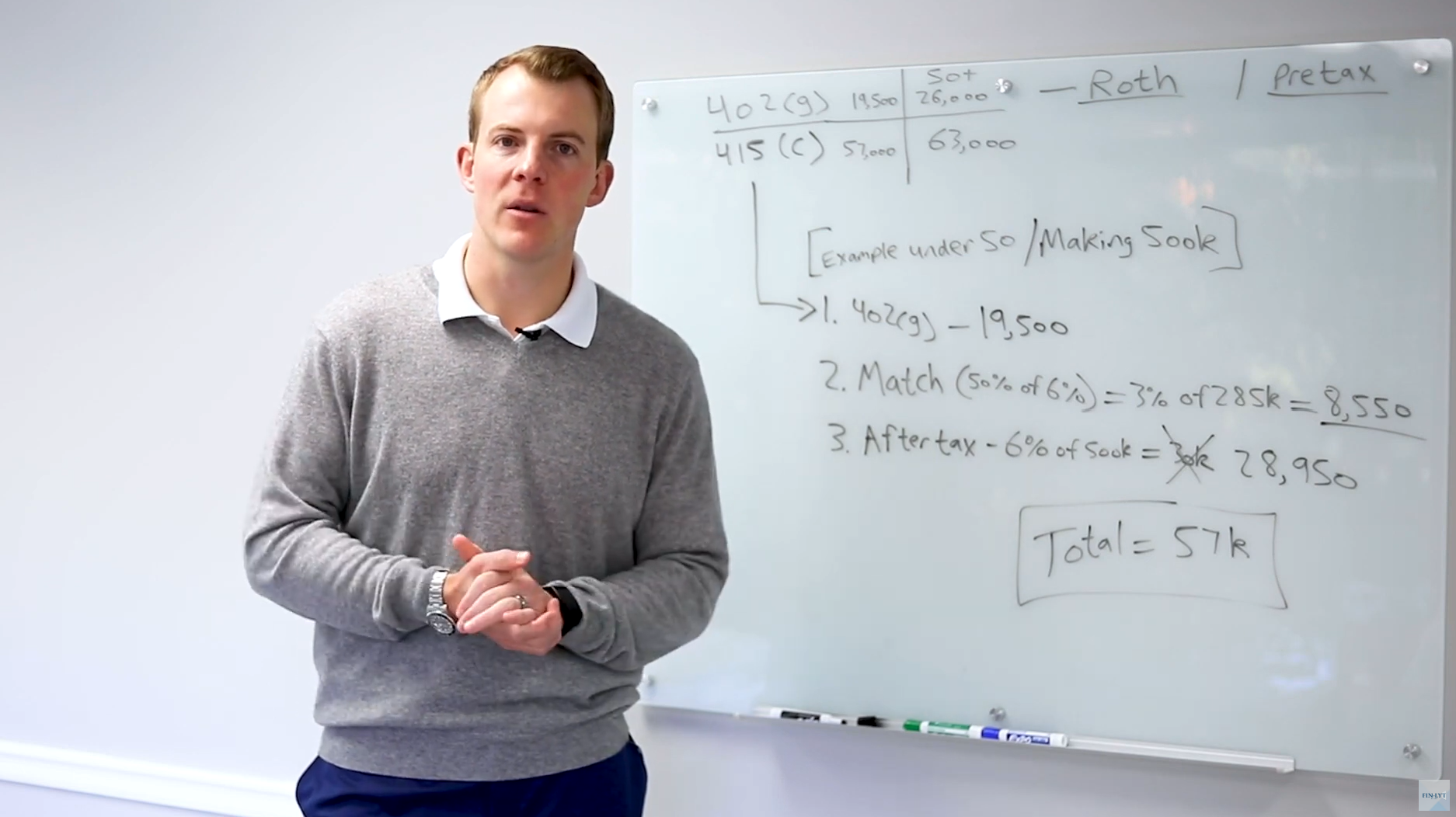

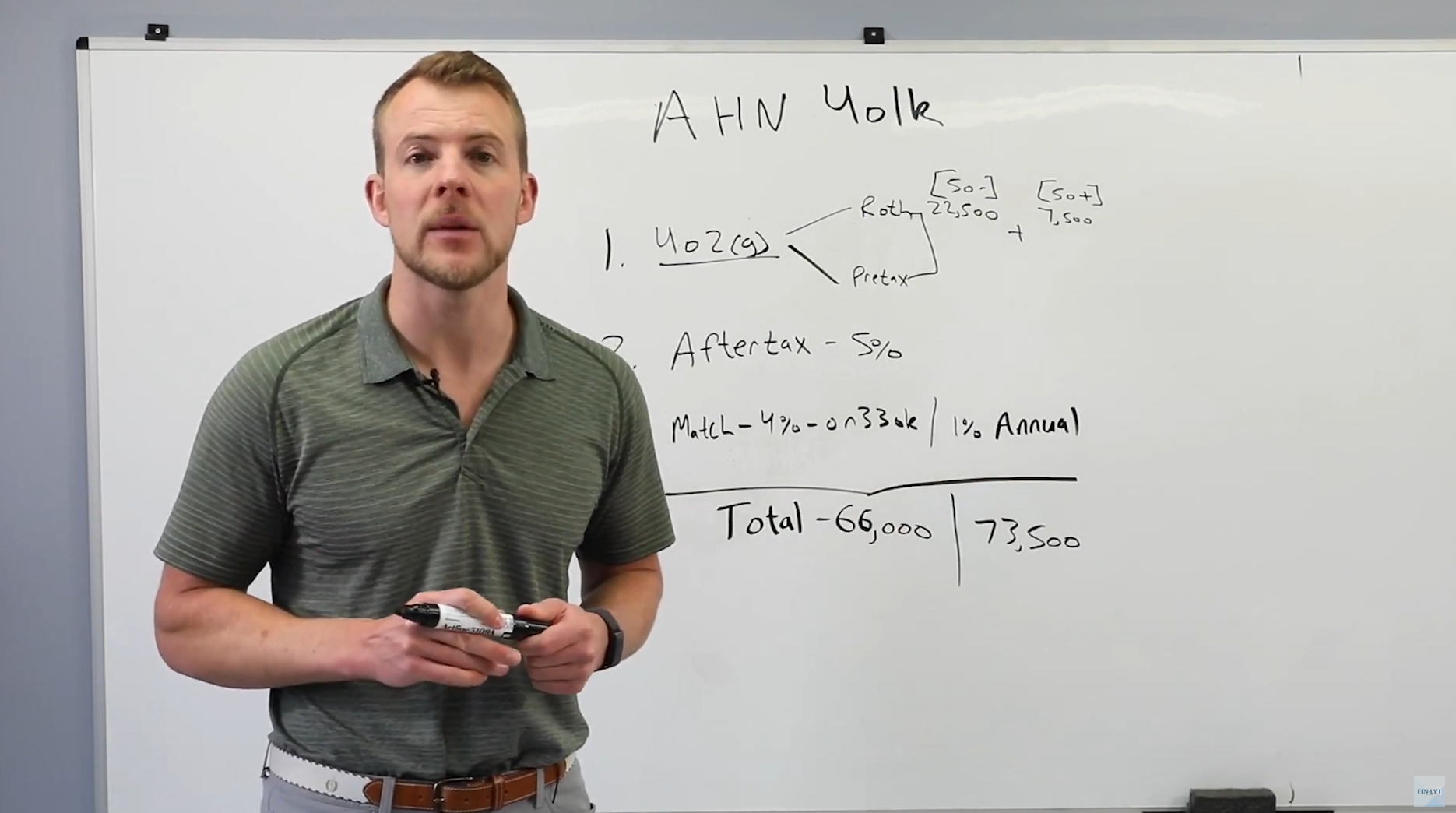

AHN Mega Backdoor Roth 2024 Updates

10:29

UPMC Mega Backdoor Roth 2024 Updates

5:35

Advice For Young, High-Income Earners

9:04

Estate Planning for Under $5M Net Worth

8:05

EWA’s Investment Philosophy

8:48

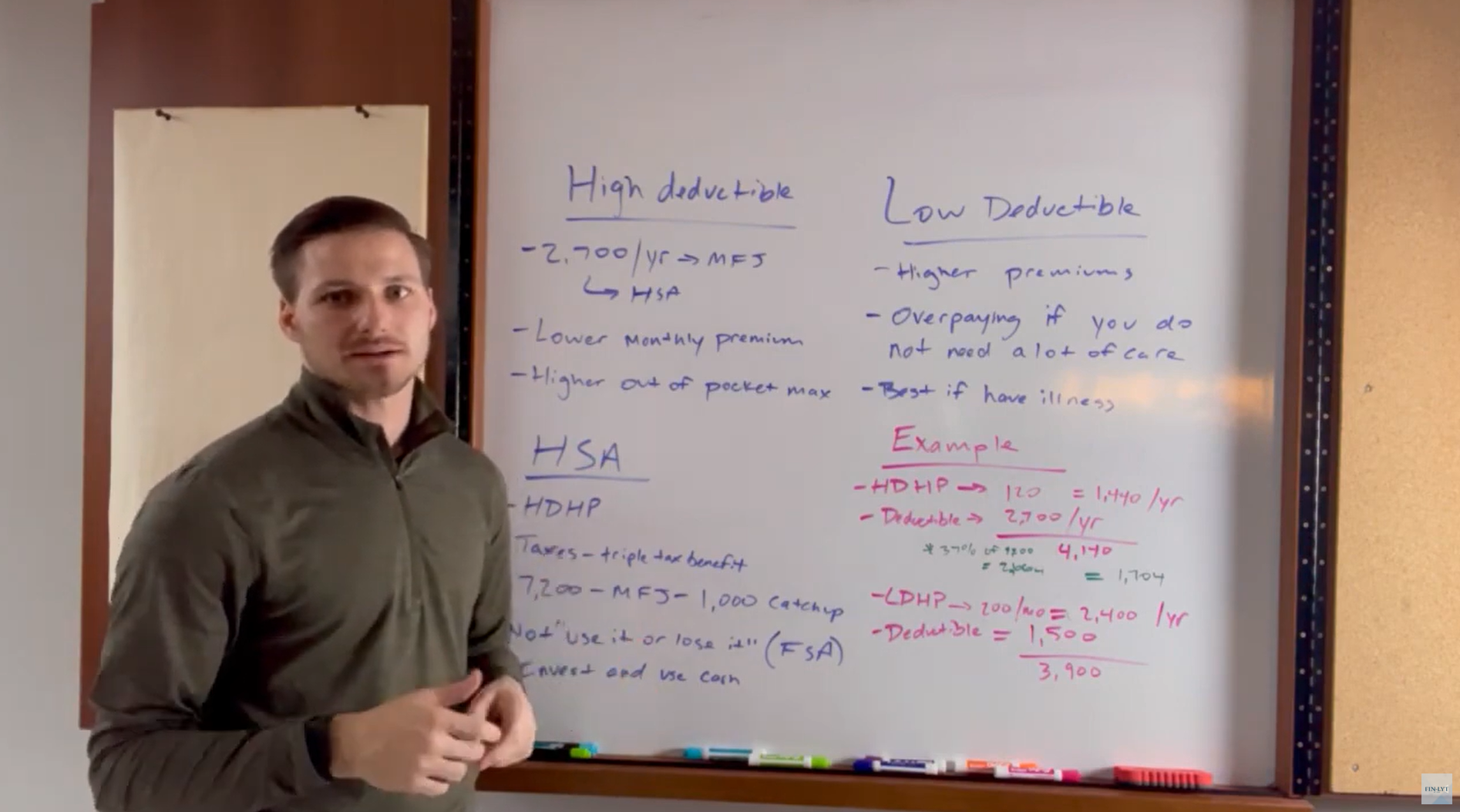

Why Would I Choose an HSA (Health Savings Account)?

7:08

Plan for Your Child with Special Needs with a Trust

7:16

Long Term Care Planning

2:06

Backdoor and Mega Backdoor ROTHs

1:55

Should You Invest in Non-US Stocks?

1:15

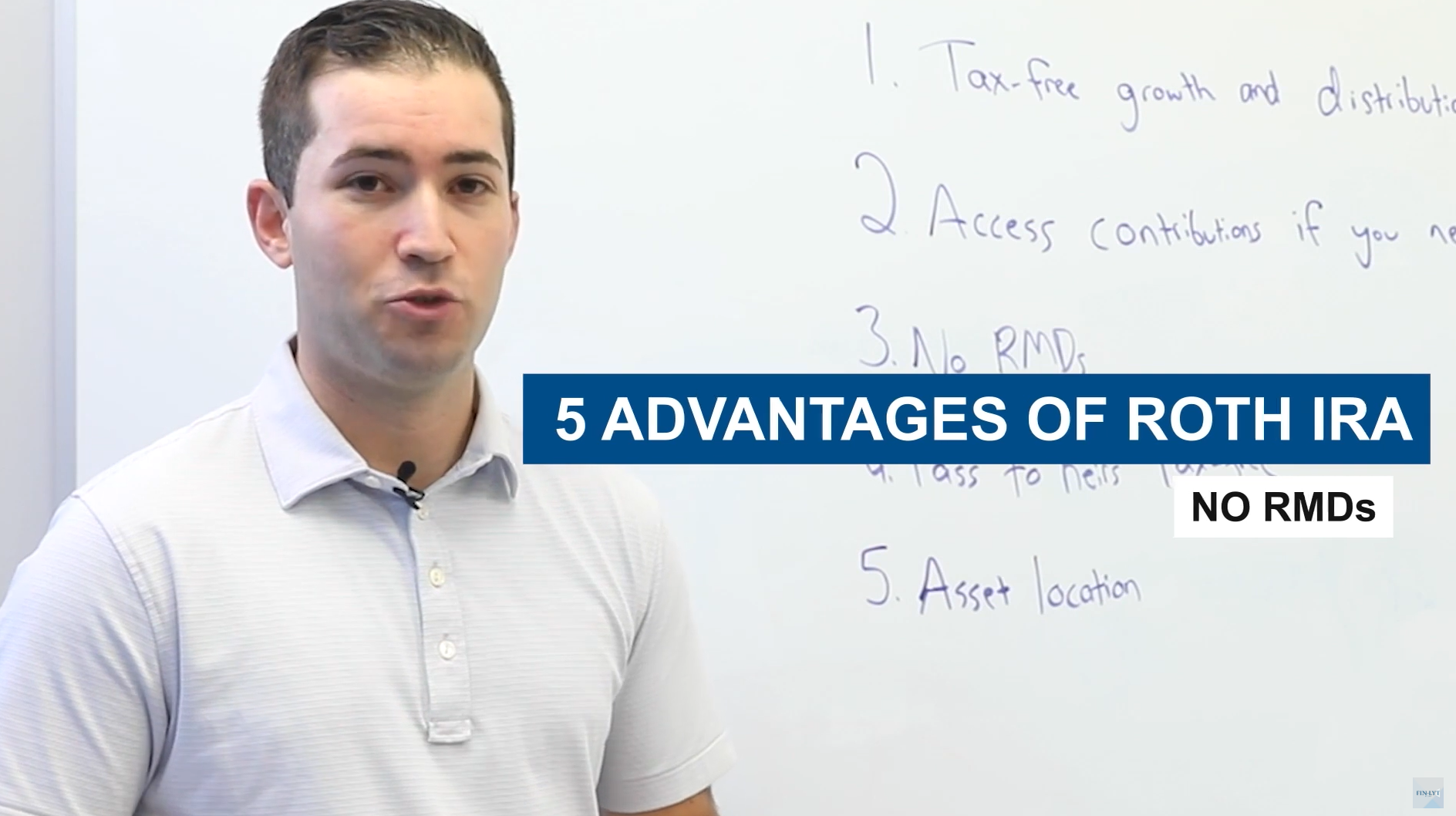

5 Advantages of Roth IRAs- #5-Asset Location

1:09

5 Advantages of Roth IRAs- #4-Pass to Heirs Tax-free

1:20

5 Advantages of Roth IRAs- #3-No RMDs

0:52

5 Advantages of Roth IRAs- #2-Access Contributions If You Need To

0:50

5 Advantages of Roth IRAs- #1-Tax-Free Growth and Distribution

2:39

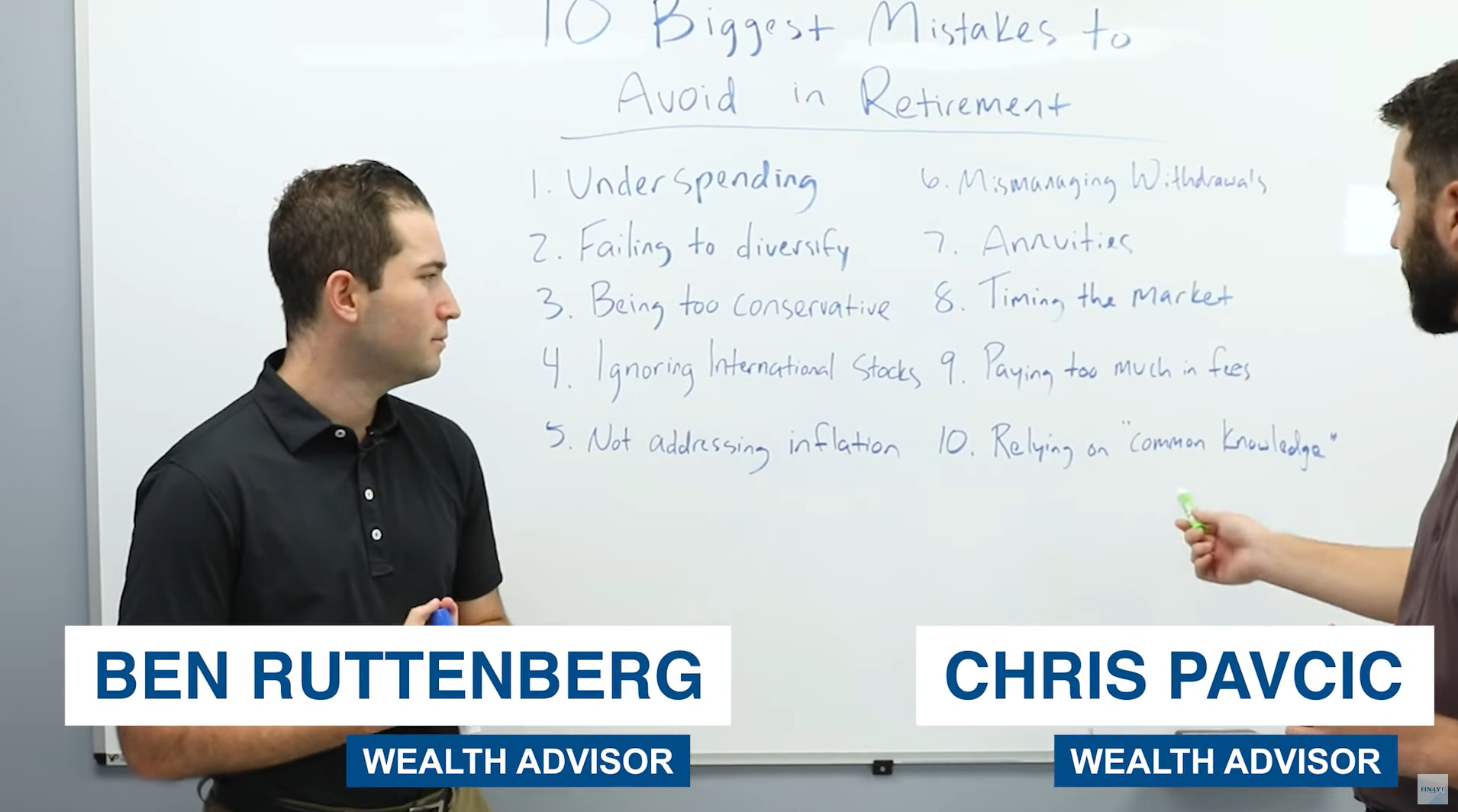

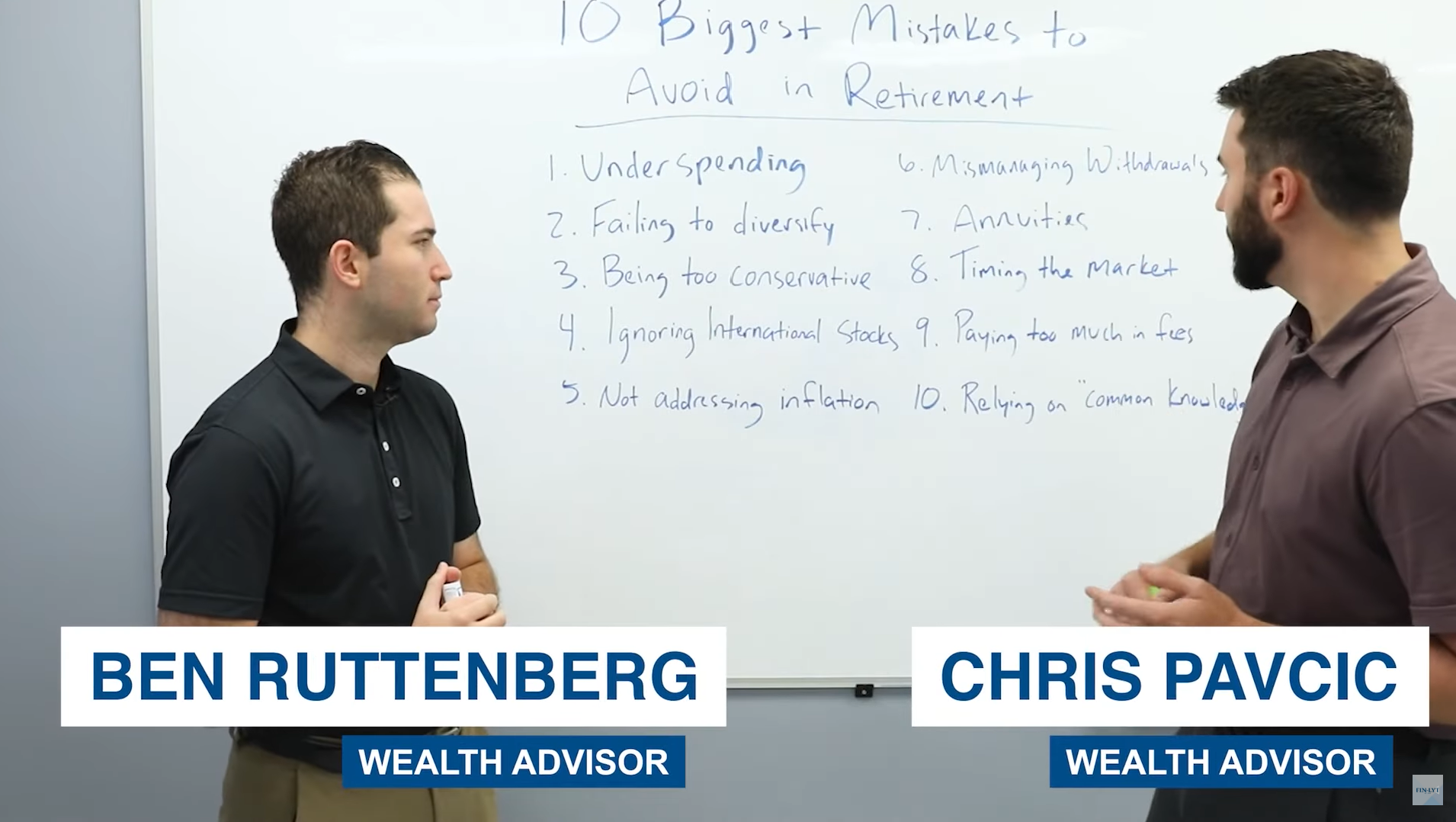

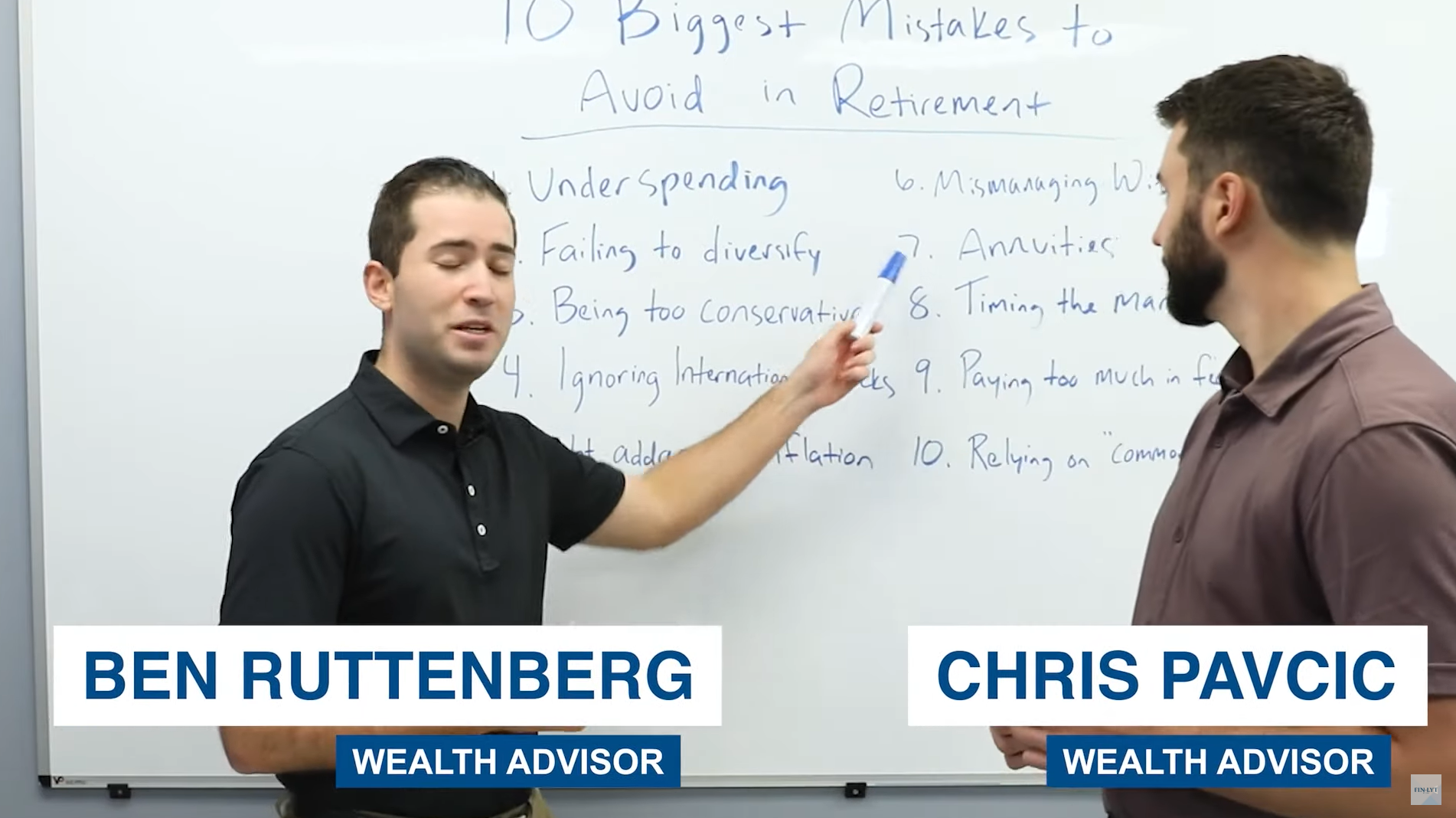

10 Mistakes That Retirees Make and How to Avoid Them: Tip 10 – Relying on “Common Knowledge”

10 Mistakes That Retirees Make and How to Avoid Them: Tip 9- Paying Too Much in Fees

2:43

10 Mistakes That Retirees Make and How to Avoid Them: Tip 8- Timing the Market

2:01

10 Mistakes That Retirees Make and How to Avoid Them: Tip 7- Annuities

2:12

10 Mistakes That Retirees Make and How to Avoid Them: Tip 6- Mismanaging Withdrawals

1:30

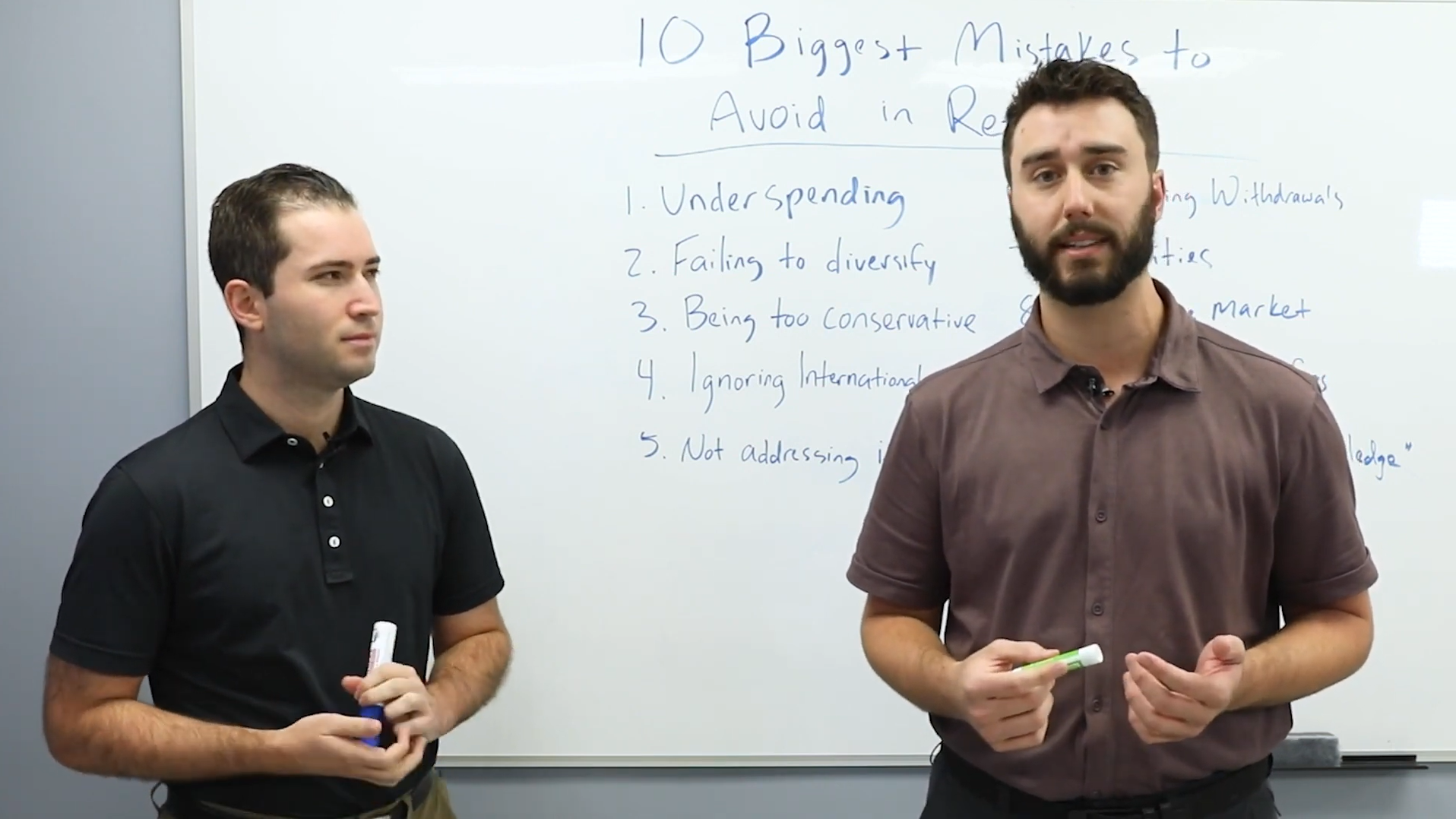

10 Mistakes That Retirees Make and How to Avoid Them: Tip 5-Not Addressing Inflation

1:56

10 Mistakes That Retirees Make and How to Avoid Them: Tip 4- Ignoring International Stocks

1:25

10 Mistakes That Retirees Make and How to Avoid Them: Tip 3- Being Too Conservative

1:52

10 Mistakes That Retirees Make and How to Avoid Them: Tip 2- Failing to Diversify

2:15

10 Mistakes That Retirees Make and How to Avoid Them: Tip 1-Underspending

3:55

Why Market Volatility is a Good Thing?

5:18

Student Loans for High Income Earners

7:01

Breaking Down Universal Life Insurance

1:03

Setting Up E-Delivery

2:42

Financial Planning for Physicians

3:56

Why Your Investment Allocation Should Never Be Aged Based

5:54

Should I Participate in my Company’s ESPP?

5:11

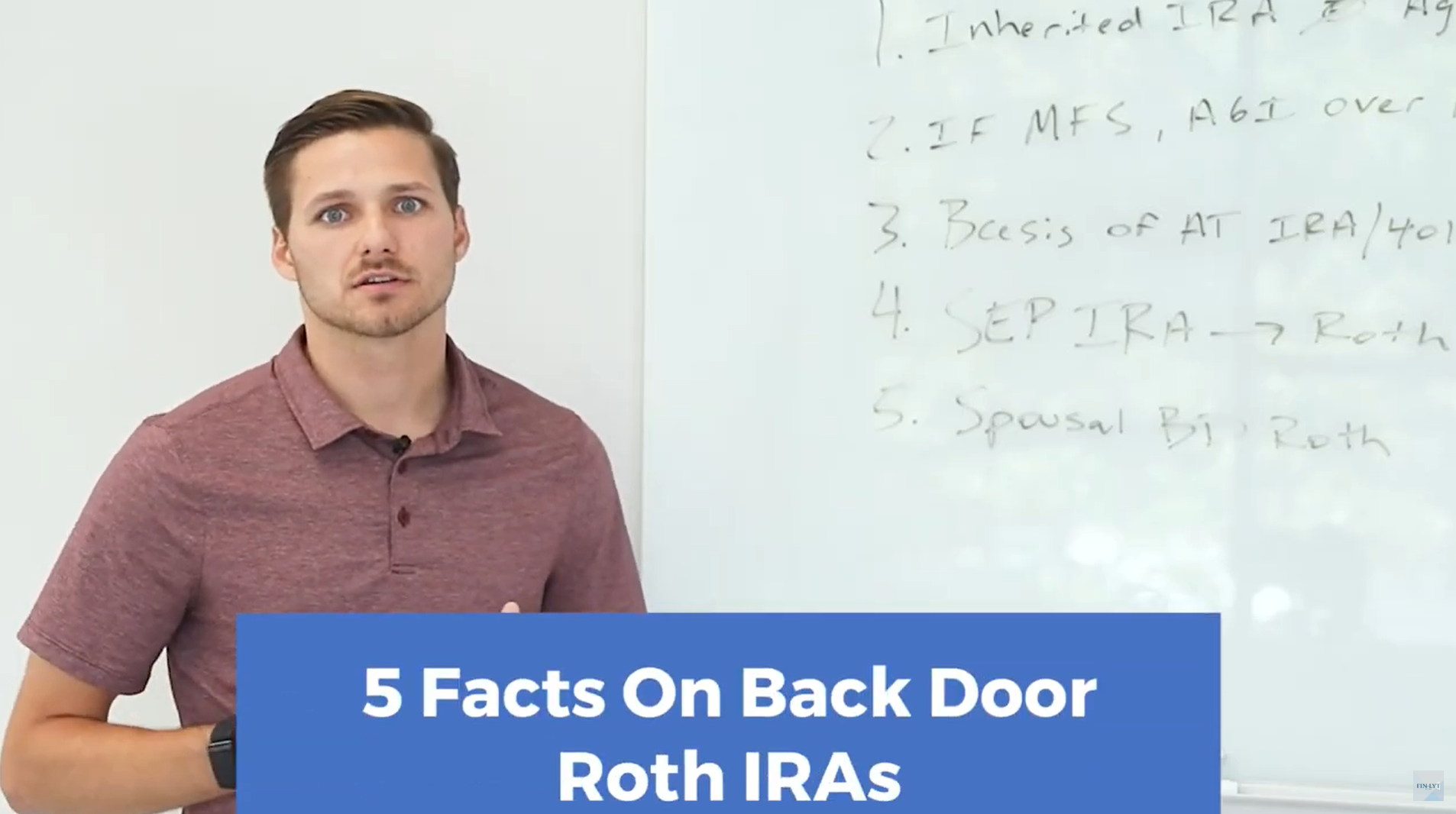

5 Considerations When Funding a Back Door Roth IRA

2:38

Proactive Conversations That Lead to Successful Wealth Transfer

3:34

Why a Buy-Sell Agreement is a Necessity for a Small Business?

6:05

3 Biggest Financial Mistakes We Have Seen

3 Best Financial Decisions We Have Seen

10:43

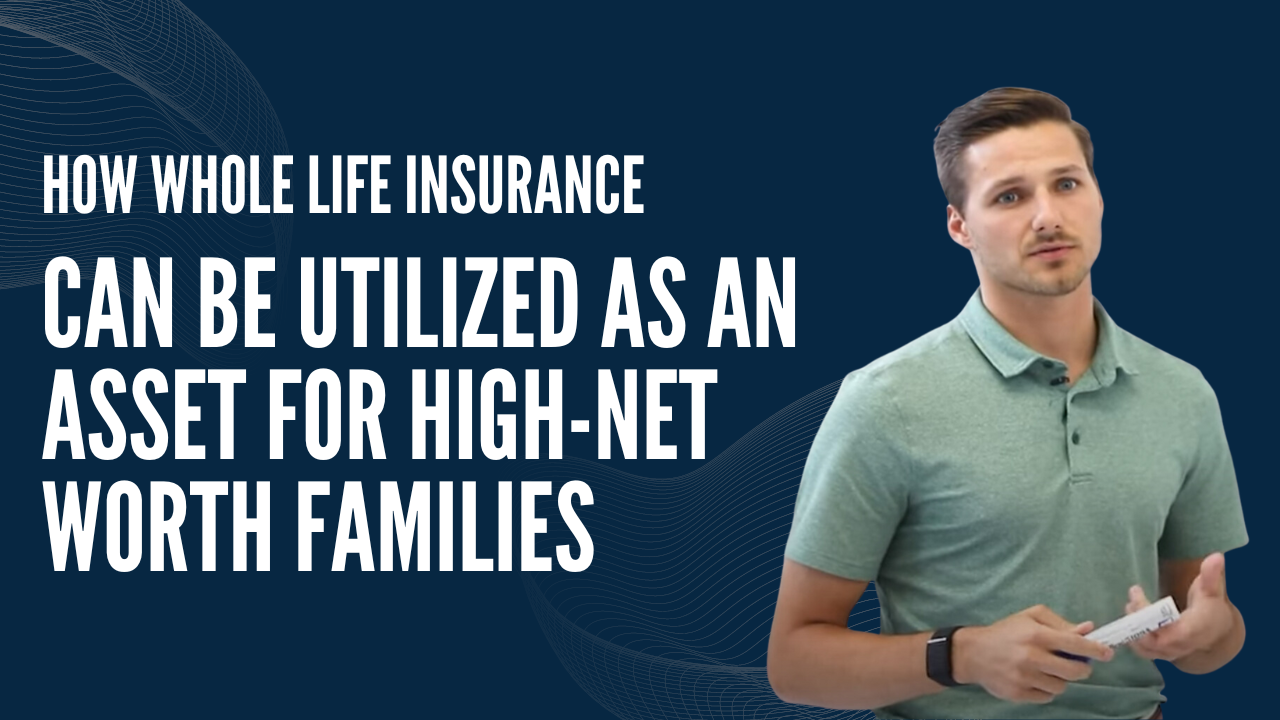

How Whole Life Insurance Can be Utilized as an Asset for High Net Worth Families

1:32

Financial Planning for Executives

6:34

How Rising Interest Rates Can Affect Your Financial Plan?

6:04

How To Take Advantage of Market Downturns?

10:00

Direct Indexing

What is the Difference Between W2 and 1099?

4:23

Firm Philosophies on Bitcoin and Concentrated Stock Positions

5:25

Reflecting on the Biggest Value an Advisor Can Provide

How to Structure a Family Loan

3:59

Weighing the Pros and Cons of Passive Real Estate Income

Should I Buy or Rent a Second Home?

Gifting to Children Under Age 18

Contributing to 457 Plans

4:39

The Difference Between Married Filing Separately vs Married Jointly

3:21

Should I get Married for Tax Purposes?

2:33

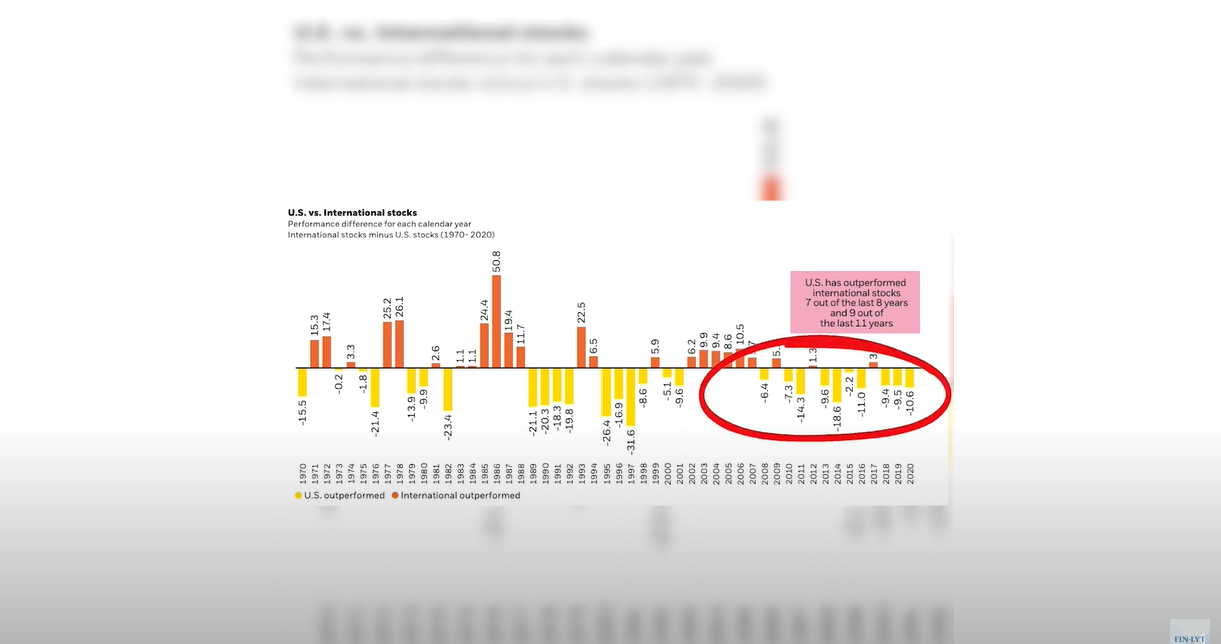

US vs International Stocks

8:34

Tax Planning 101

2:57

Win More by Losing Less

3:06

Feeling Safe May Be Risky

2:49

Investing with Emotions

Ranking Savings Options in Order of Importance

7:27

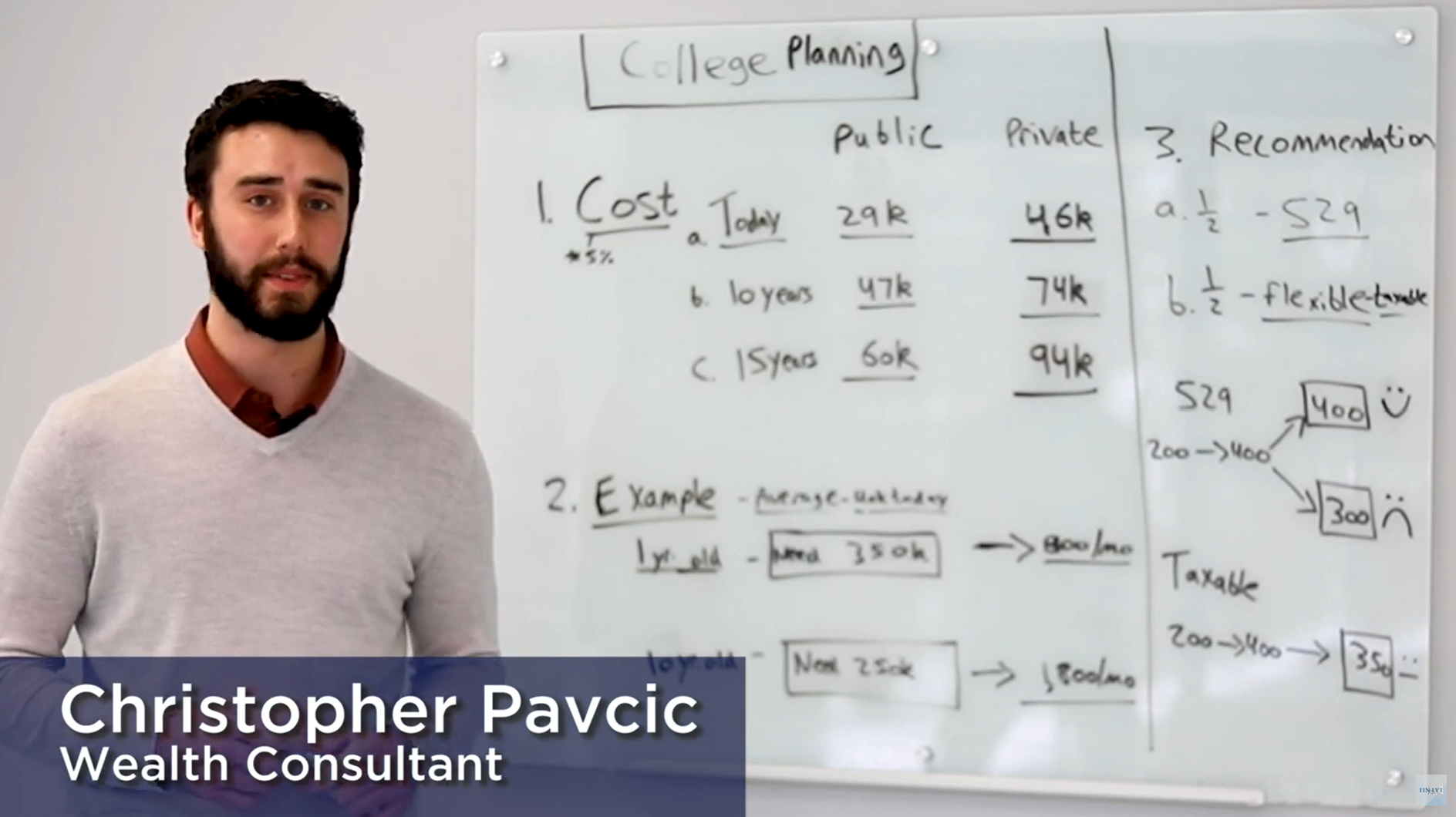

College Planning Basics

The Power of Tax Deferral on Your Investment Planning

Buying vs Leasing Your Car

8:09

Basic Rules of Thumb for Mortgages

Ignore Negative Headlines

5:00

What Does War Mean for the Stock Market?

2:26

Our One-Roof Philosphy

4:33

Long Term Disability Planning for High Income Earners

1:43

Tips for Raising Financially Responsible Kids

The Pros of Roth IRA’s

3:29

Differences Between Revocable and Irrevocable Trusts

Lifetime Gifting

4:05

How Do You Know Which Health Insurance Plan is Right for You?

The Art of Merging Finances

4:21

RSU (Restricted Stock Unit) Basics

Stock Option Basics

3:42

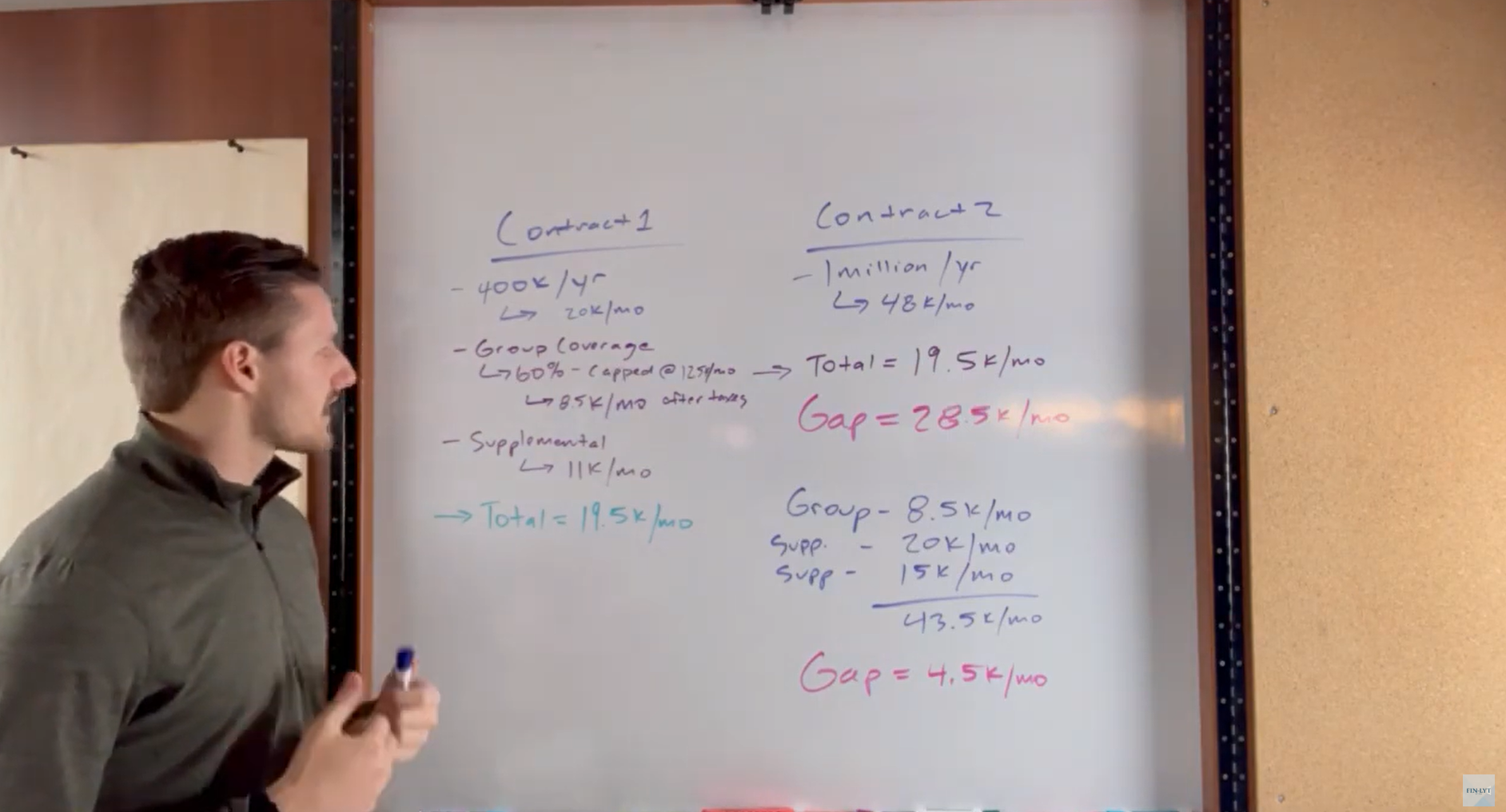

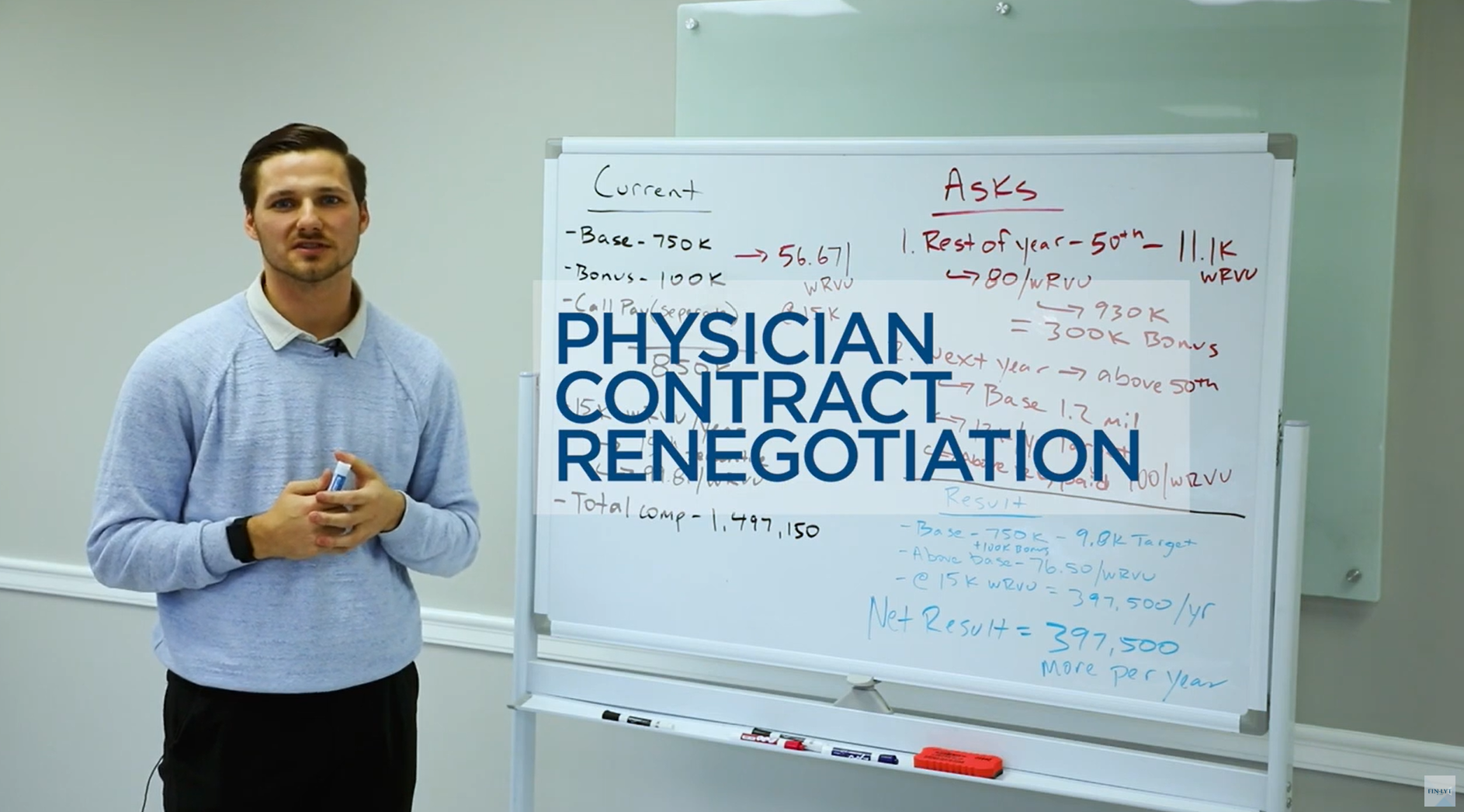

Physician Contract Renegotiation

5:28

Common Questions on Estate Planning

7:17

Variable Annuities Explained

4:27

Should You Have All of Your Money with One Team or Spread Among Several Advisors?

3:23

EWA’s Time Management Philosophies

Why We Disagree with the FIRE Movement

8:57

Why Roth Conversions?

5 Tips to Protect Your Identity

3:26

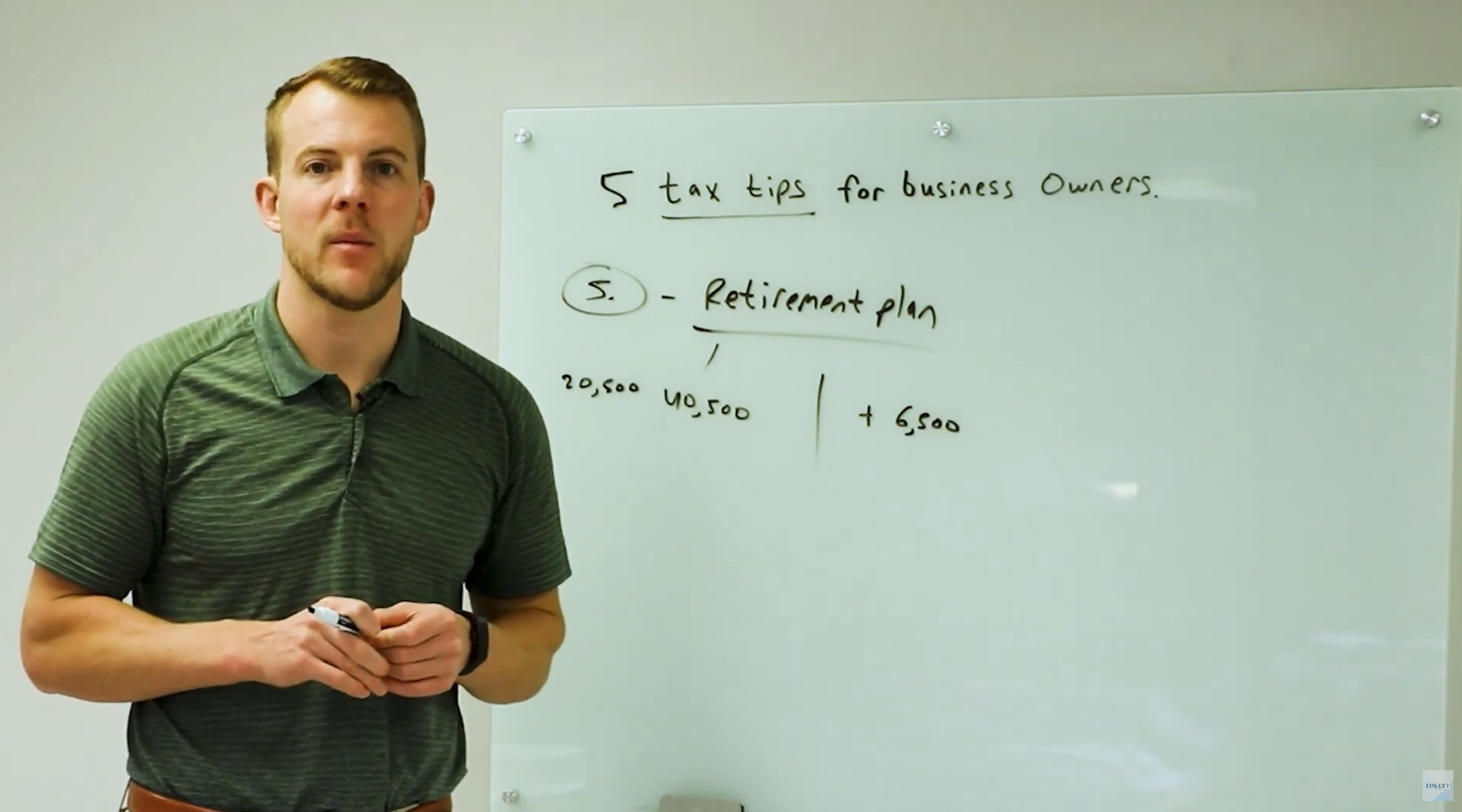

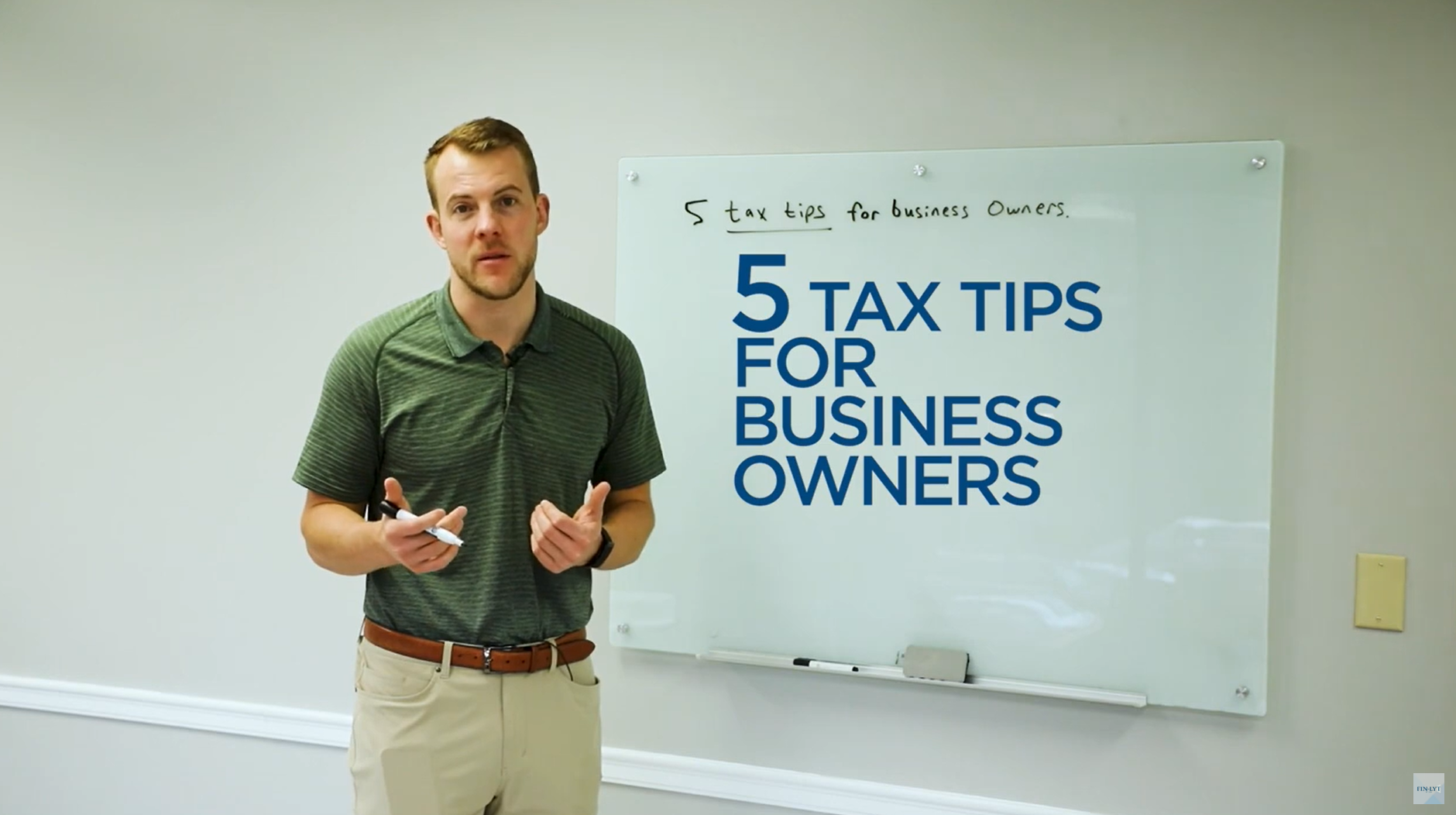

5 Tax Tips for Business Owners- Tip 5- Implement a 401k and Cash Balance Plan

2:45

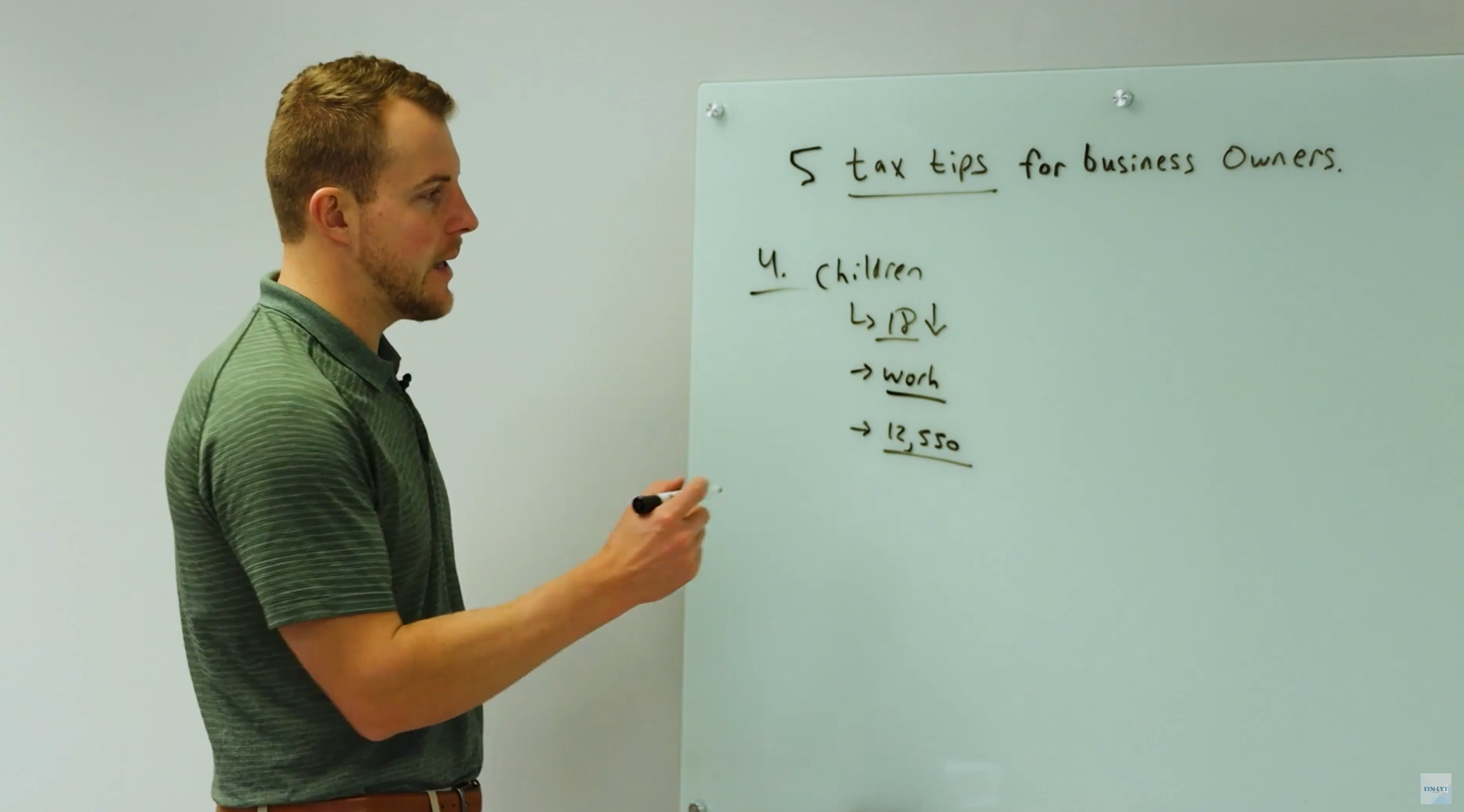

5 Tax Tips for Business Owners- Tip 4- Hire Your Children

6:44

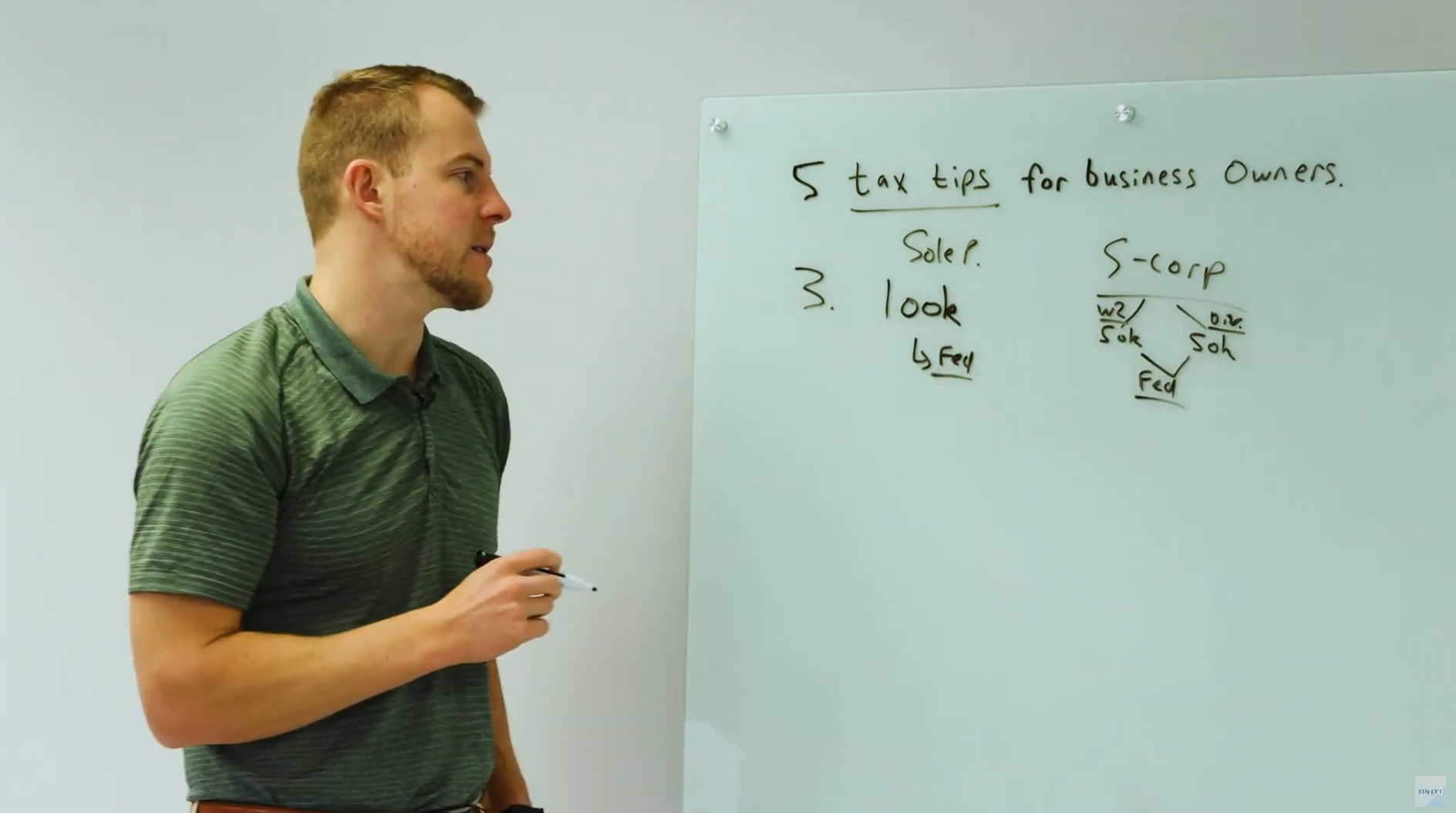

5 Tax Tips for Business Owners- Tip 3- Use S Corp Election to Lower Salary

2:09

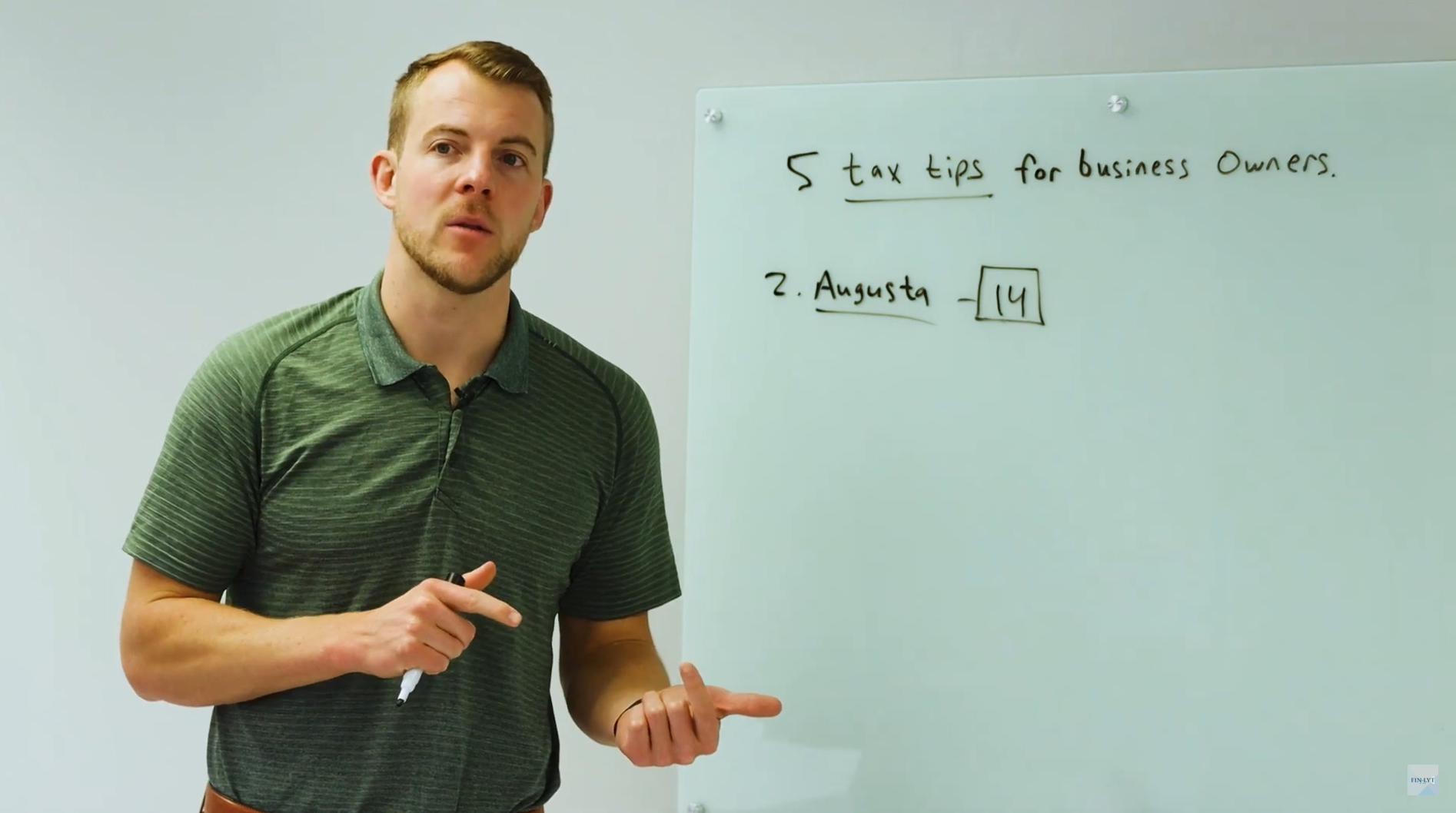

5 Tax Tips for Business Owners- Tip 2- Use the Augusta Rule

3:07

5 Tax Tips for Business Owners- Tip 1- Section 179 – Accelerated Write Off for Vehicle

2:10

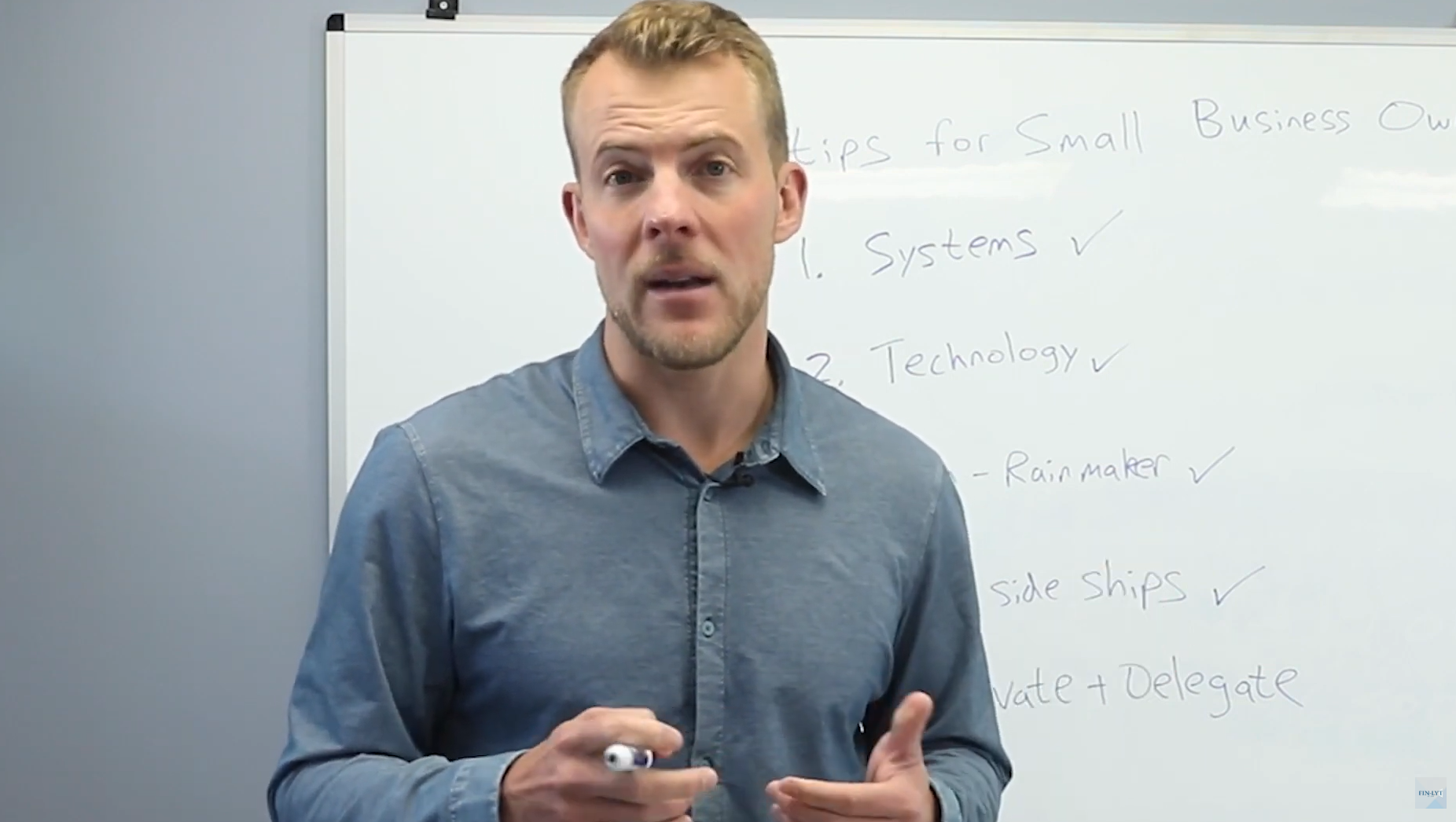

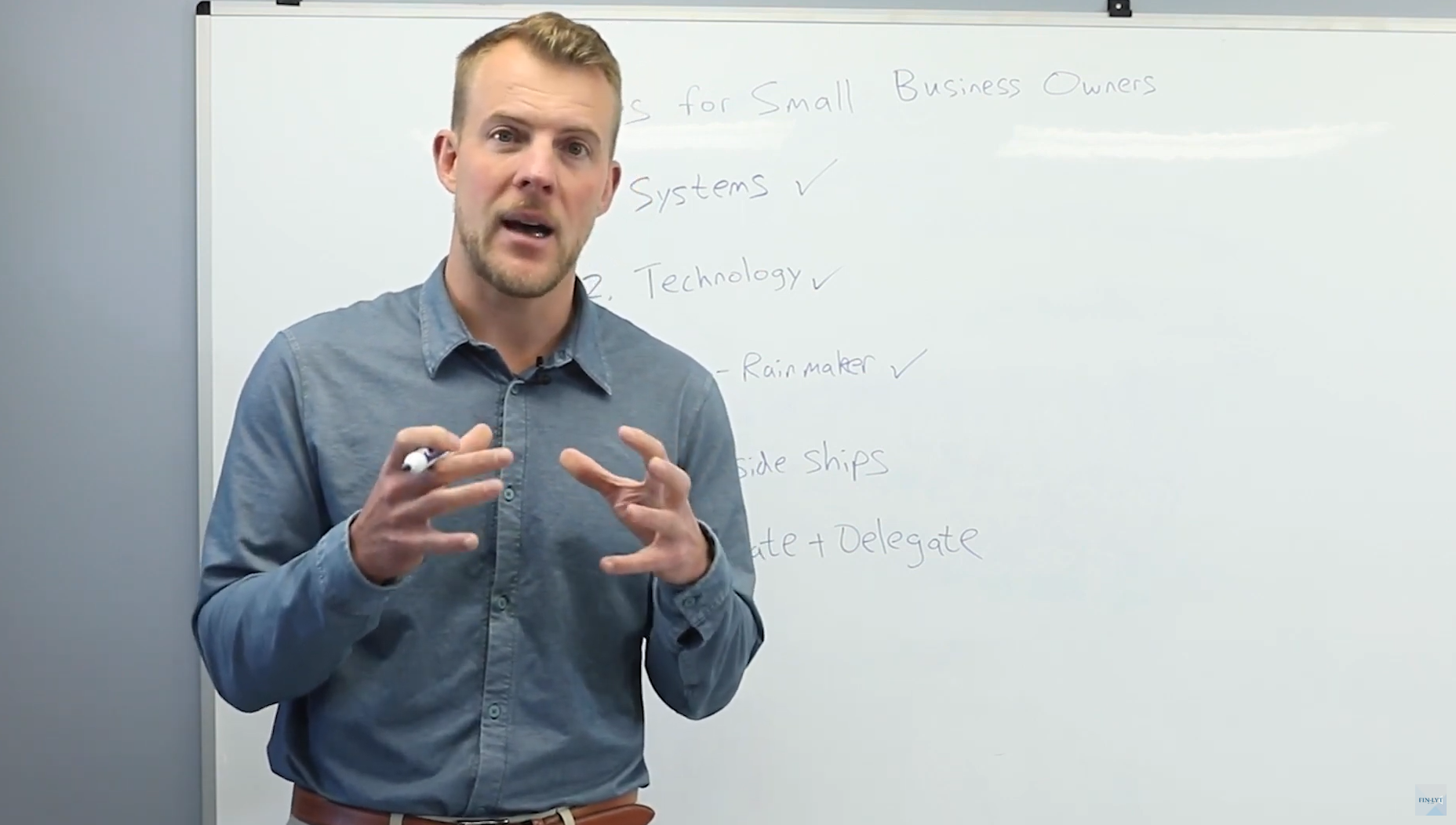

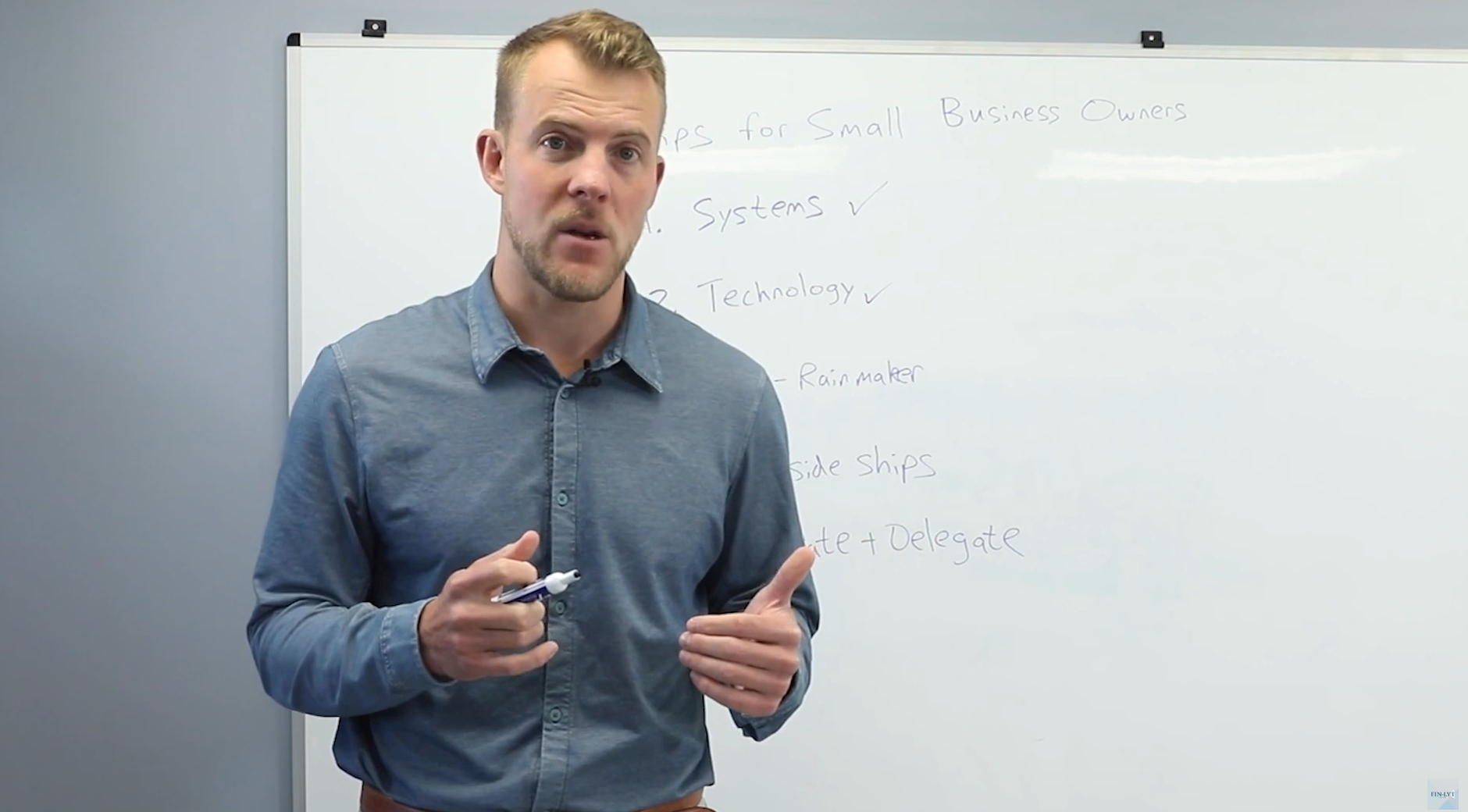

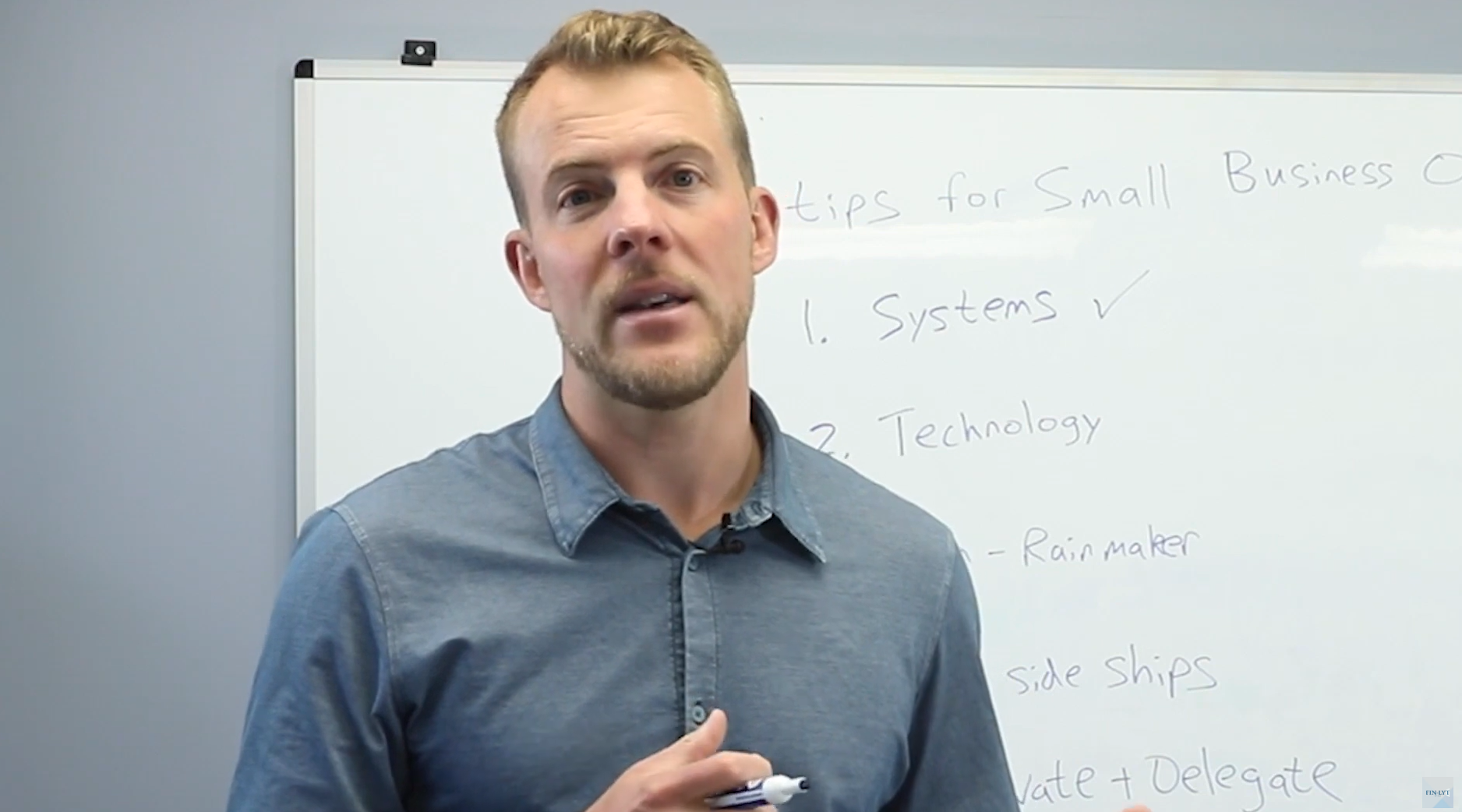

5 Tips to Run Your Business Stress Free- Tip 5- Elevate and Delegate

2:22

5 Tips to Run Your Business Stress Free- Tip 4- Have a One Ship Mentality

2:25

5 Tips to Run Your Business Stress Free- Tip 3- Make Your Firm an Established Rainmaker

2:28

5 Tips to Run Your Business Stress Free- Tip 2- Adopt, Don’t Fight Technology

2:53

5 Tips to Run Your Business Stress Free- Tip 1- Have Great Systems In Place

5:24

Tips for Maximizing Social Security Benefits as a Business Owner

5:37

3 Tips for Structuring an Operating Agreement for Your Business

7:09

Sequence of Returns

2:18

EWA Principle: Standards Over Feelings

3:49

EWA Principle: Methods to Avoid Task Switching

3:04

EWA Principle: Having Uncomfortable Conversations Leads to Greater Success and Happiness

3:44

EWA Principle: Easy Choices, Hard Life. Hard Choices, Easy Life.

4:34

Did You Know You Can Have Multiple 401k Plans?

2:52

Cash Balance Pension Plans

7:55

Whole Life Vs Term- What are the Differences?

Best Practices When Switching Financial Advisors

3:28

Common Misconceptions About Bonds

Asset Protection Strategies

3:19

What To Expect Before Your First Meeting with EWA?

9:40

The Truth About Target Date Funds

4:06

Tips for Long Term Investing

3:13

Top Financial Tips When Switching Jobs

Index Annuities Explained

9:20

Fixed Annuities Explained

3:54

Tips for Retirement Distribution Planning

3:14

Secured Lines of Credit

3:30

Asset Location Explained

11:22

What are Donor Advised Funds?

8:33

Social Security Basics

7:39

The AHN Mega Backdoor Roth

7:04

The UPMC Mega Backdoor Roth

5:08

Estate Planning Basics

1:19

How to Access Your QPR

5:22

Accessing the Client Service Portal

What is a QPR?

1:29

Refinancing Your Home Mortgage

6:10

What is Your Money Temperature?

3:40

EWA’s 3 C’s

2:00

10 Tips for Current Retirees – Tip 10- Plan Your Travel

3:41

10 Tips for Current Retirees – Tip 9- Have a Game Plan Around Social Security

2:55

10 Tips for Current Retirees – Tip 8- Have a 7 Year Spending Back Up

10 Tips for Current Retirees – Tip 7- Consider How You Will Spend Your Time

3:22

10 Tips for Current Retirees – Tip 6- Don’t Base Investment Allocation on Your Age

2:23

10 Tips for Current Retirees – Tip 5- Track Monthly Spending

1:59

10 Tips for Current Retirees – Tip 4- Have a Game Plan for Long Term Care

10 Tips for Current Retirees – Tip 3- Be Aware of Annuities

1:28

10 Tips for Current Retirees – Tip 2- Recognize Your Investor Bias

10 Tips for Current Retirees – Tip 1- Have a Team of Trusted Advisors

5 Tips for Retirees- Tip 5- Set After Retirement Goals

5 Tips for Retirees- Tip 4- Exercises to Prepare for Retirement

4:47

5 Tips for Retirees- Tip 3- Social Security Do’s and Don’ts

5 Tips for Retirees- Tip 2- Medicare Planning

6:14

5 Tips for Retirees- Tip 1- Tax Bracket Management

5:43

Tips for Staying Calm During a Recession

5:17

5 Tips for Parents- Tip 5- Financial Aid Appeals

9:05

5 Tips for Parents- Tip 4- General Tips on School Loans

3:51

5 Tips for Parents- Tip 3- Put Proper Time Into Researching Additional Scholarships

1:39

5 Tips for Parents- Tip 2- Stay Open to Out of State Opportunities

2:14

5 Tips for Parents- Tip 1- Do Very In Depth Research

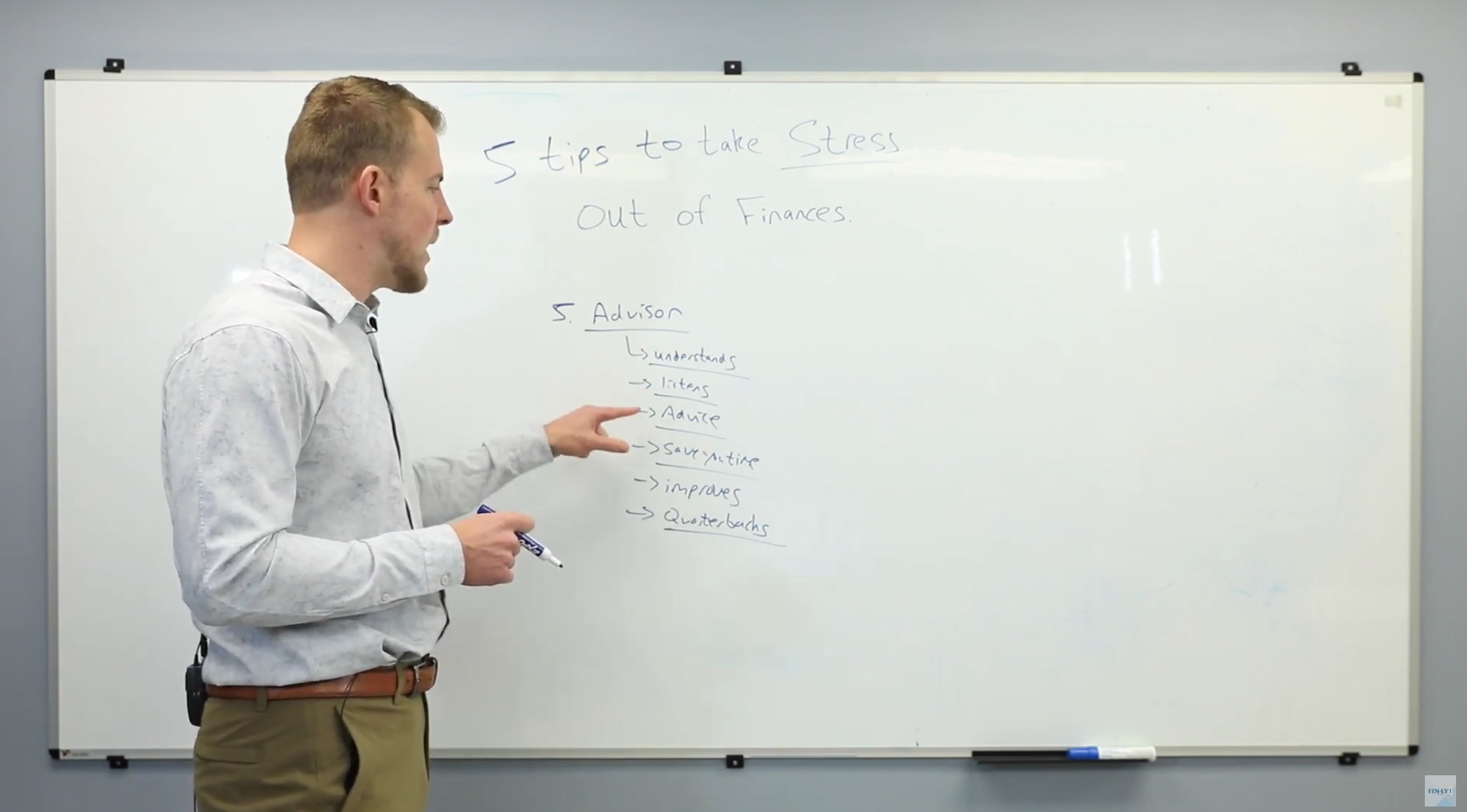

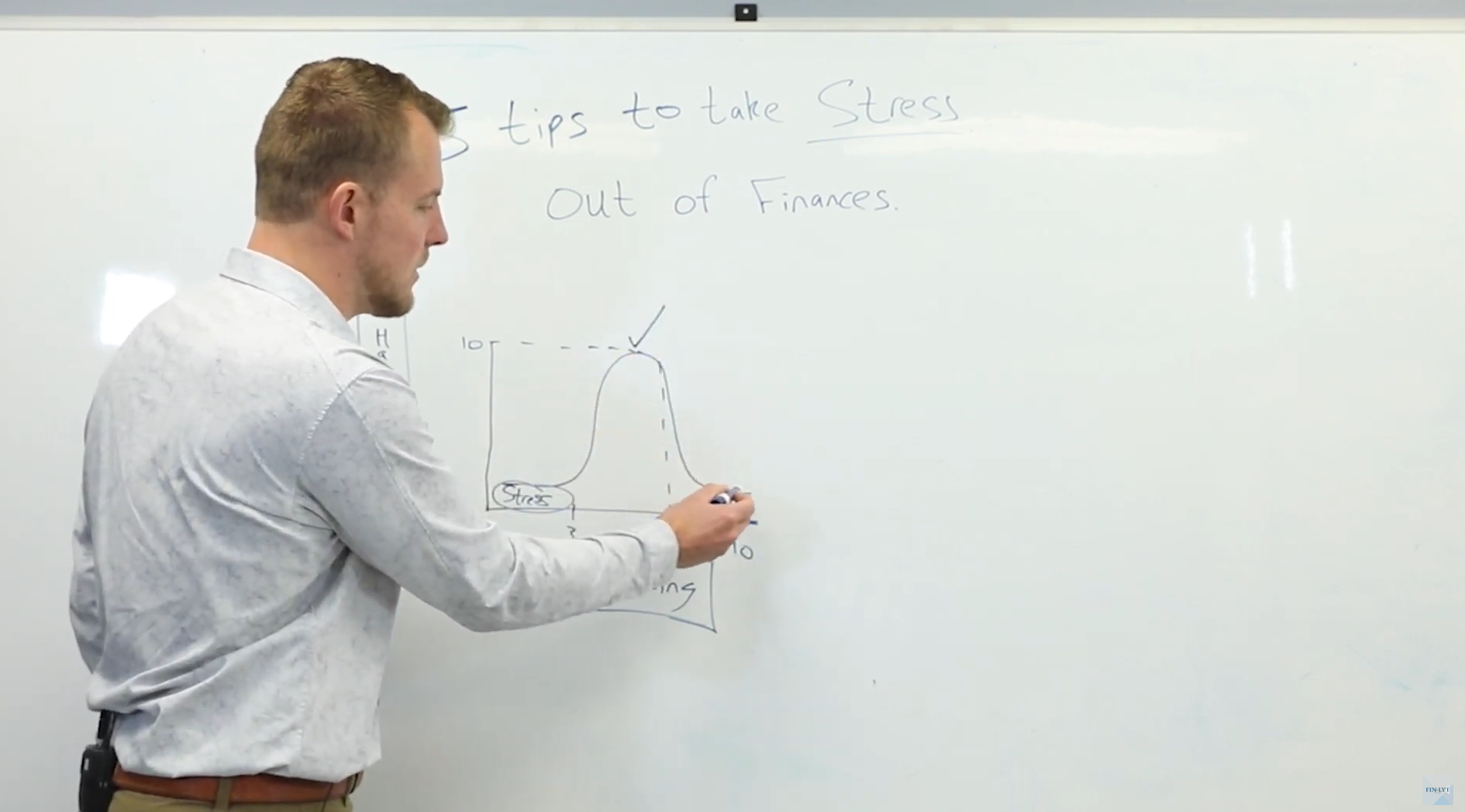

5 Tips to Remove Stress From Your Finances – Tip 5- Hire, and Know When to Fire, An Advisor

4:50

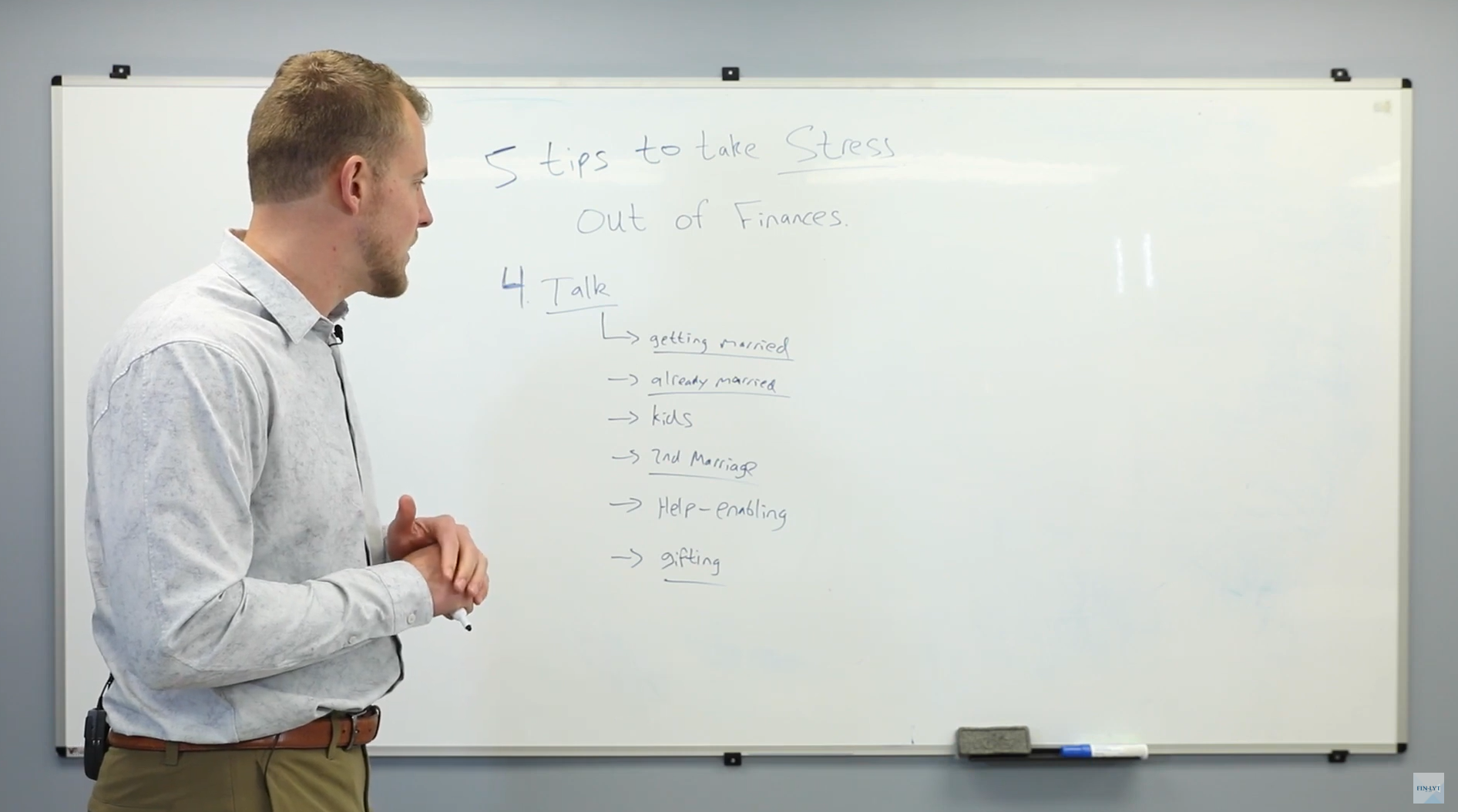

5 Tips to Remove Stress From Your Finances – Tip 4- Talk About Money

5:16

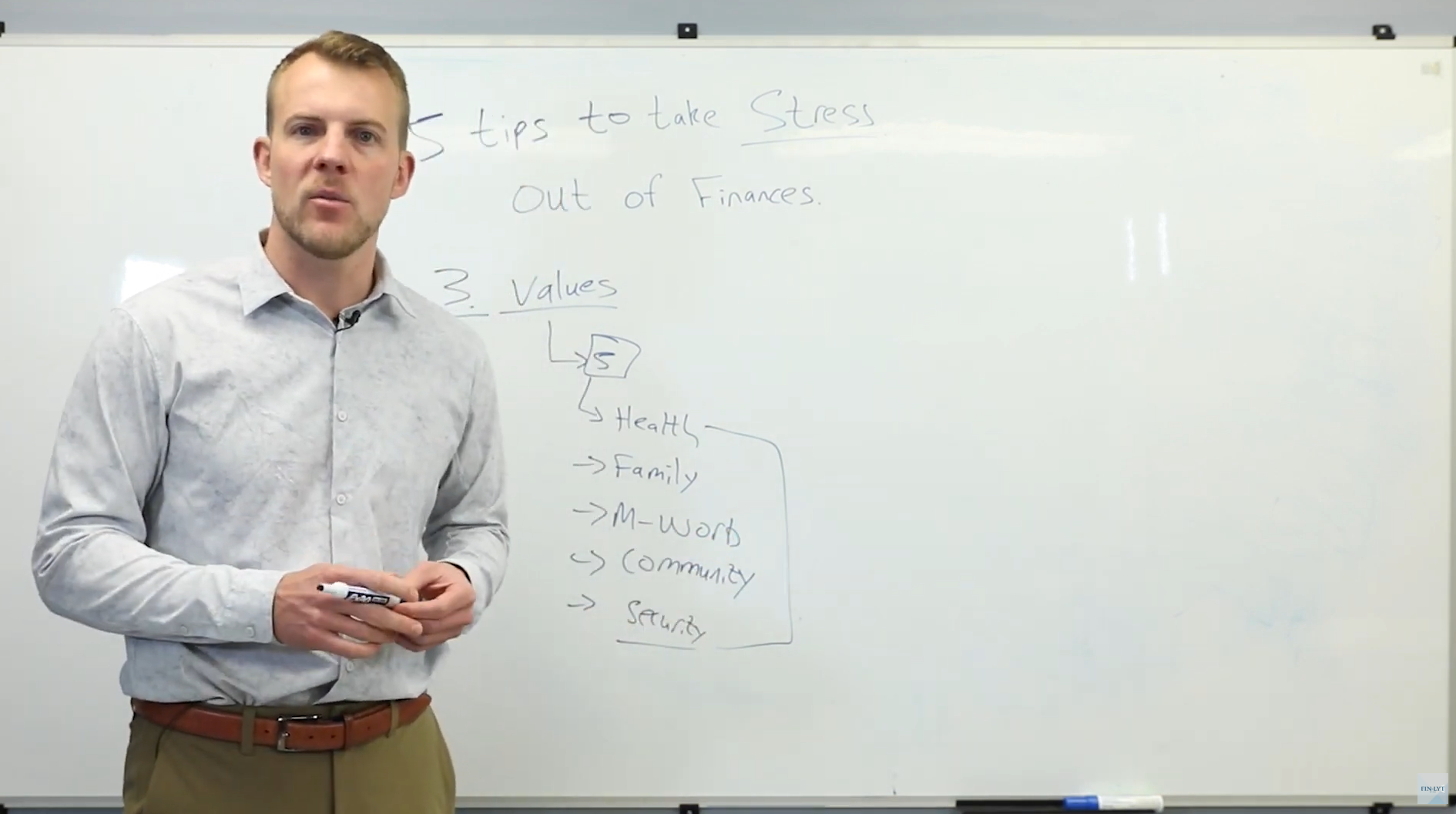

5 Tips to Remove Stress From Your Finances – Tip 3- Establish Your Top 5 Values for Decision Making

5:13

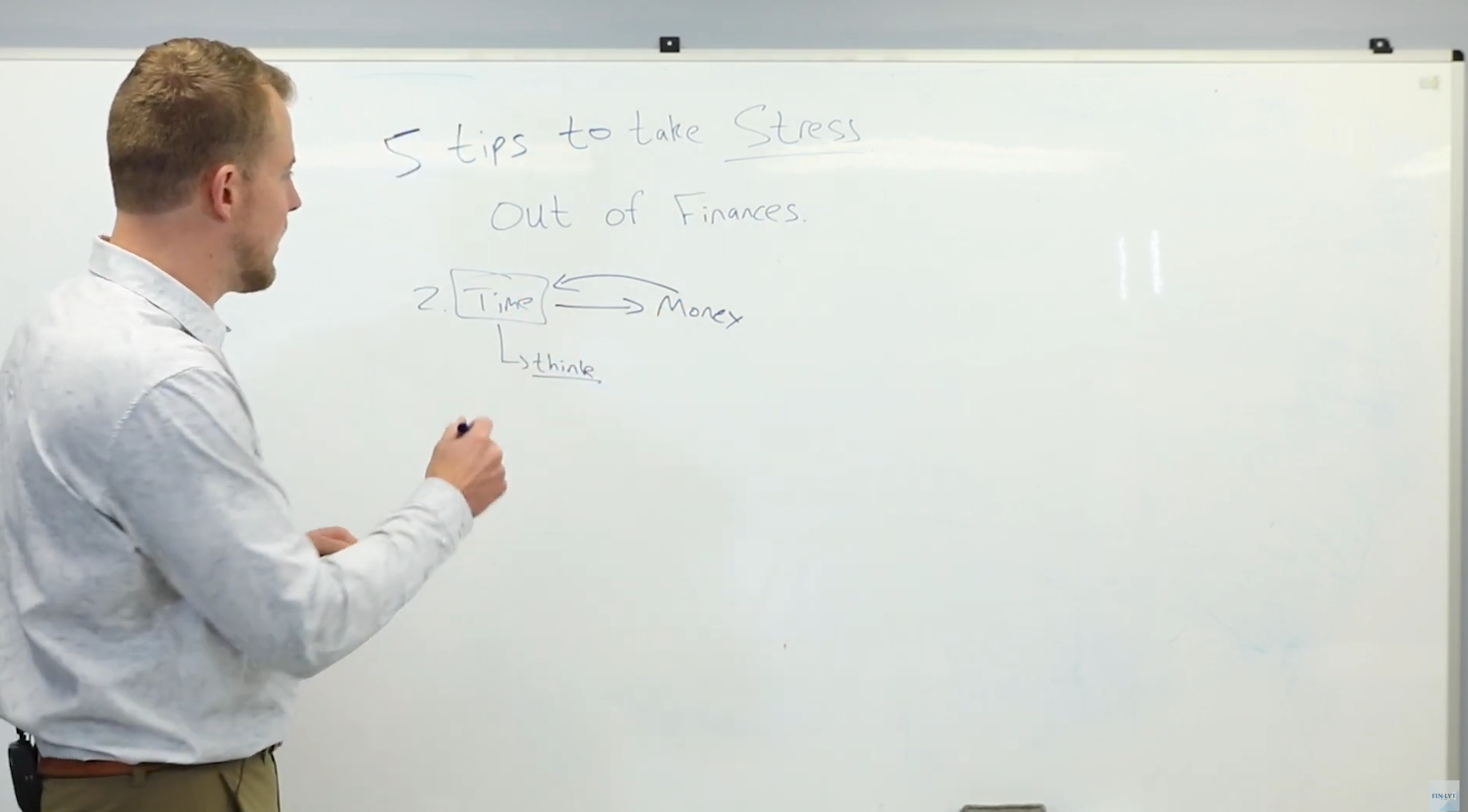

5 Tips to Remove Stress From Your Finances: Tip 2- Evaluate How You Trade Time for Money

4:15

5 Tips to Remove Stress From Your Finances: Tip 1- Healthy Tracking vs Unhealthy Tracking

6:41

What is the Difference Between an LLC Partnership and an S-Corp?

7:02

Updates to AHN Mega Backdoor Roth 401k

21:04

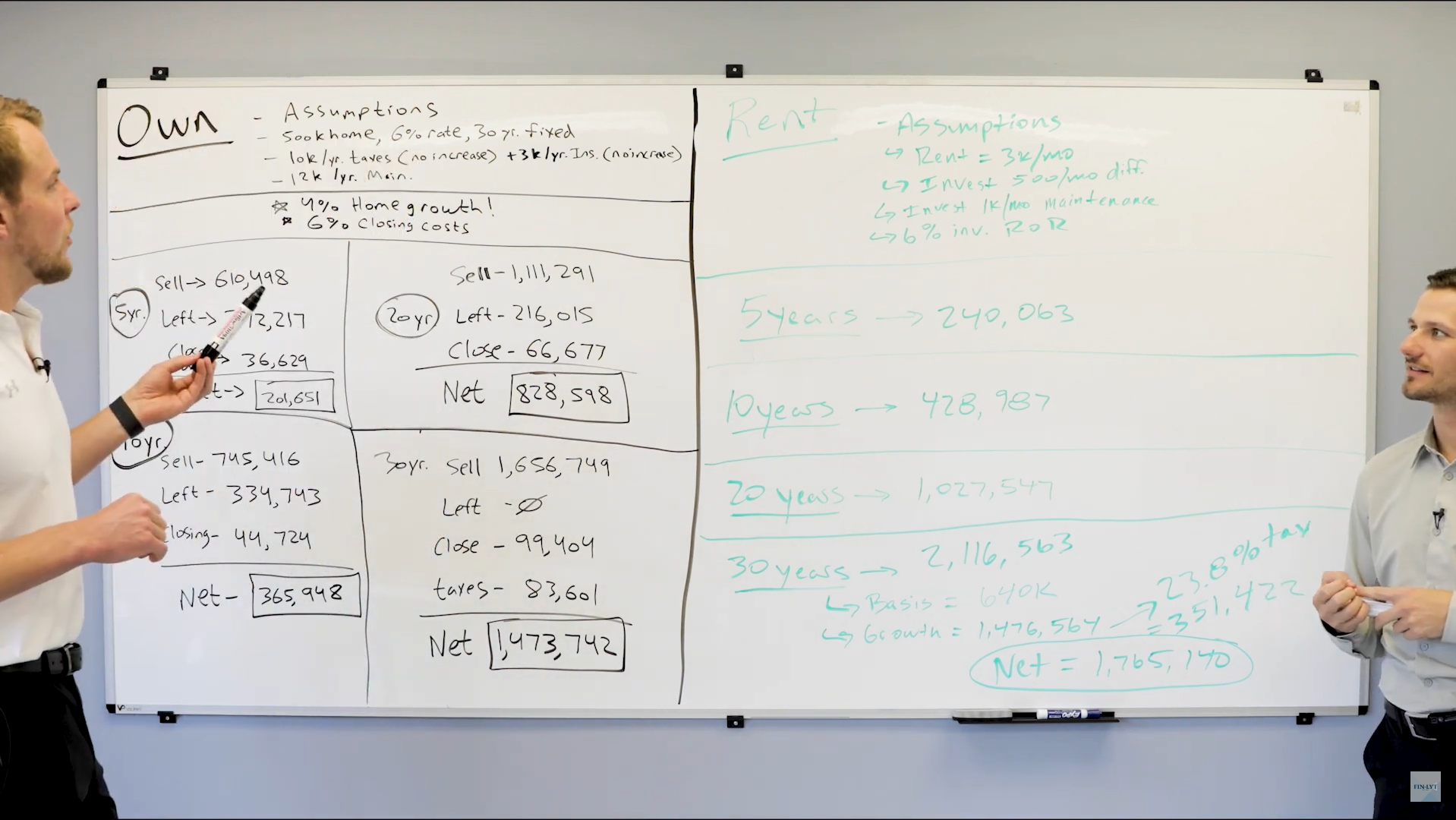

The Great Debate! Which is a Better Financial Decision, Buying or Renting Your Primary Home?

4:44

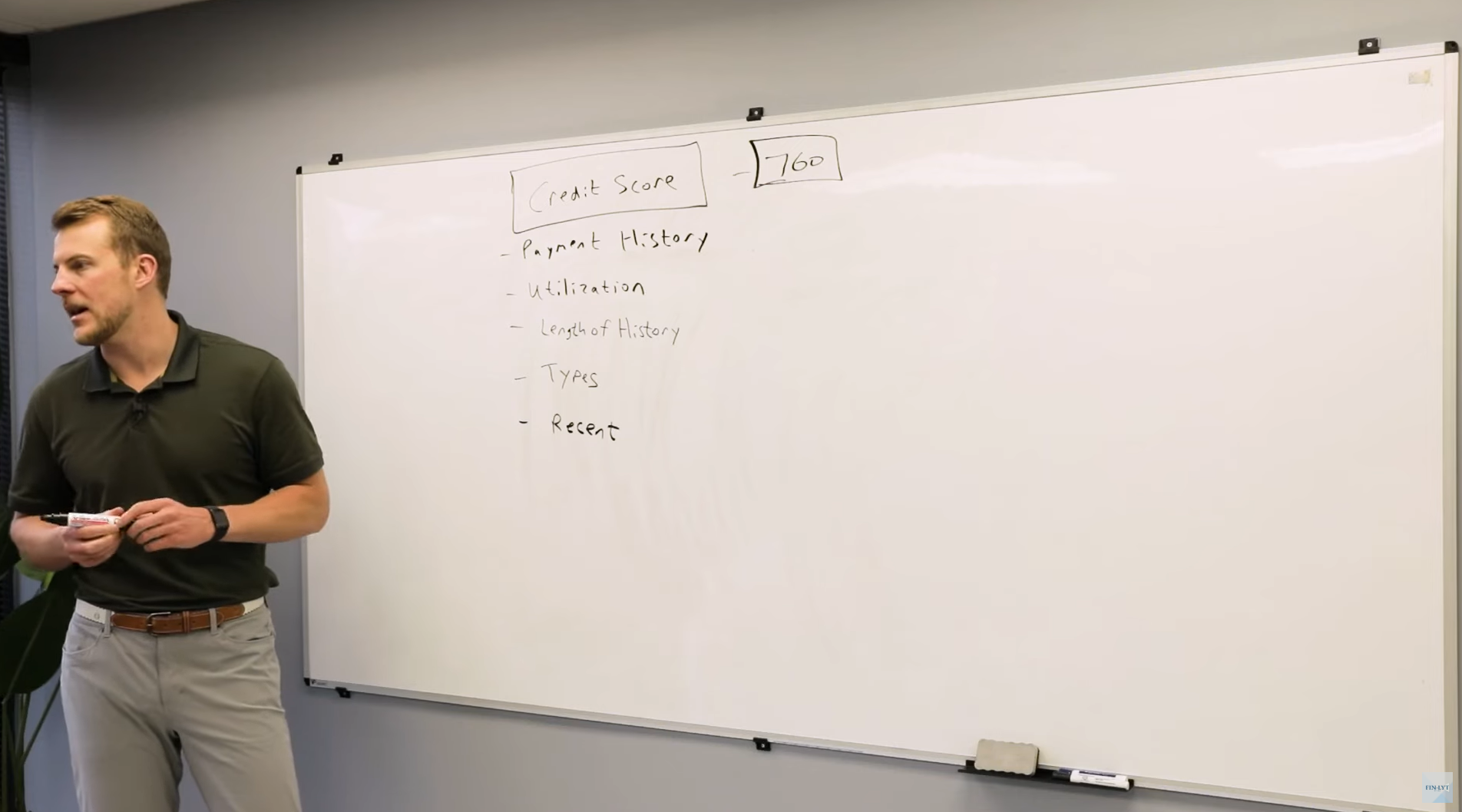

Traveling With Credit Card Points- Video #6- Tips For Managing Credit Score While Travel Hacking

6:02

Traveling With Credit Card Points- Video #5- Logistics of Paying Taxes with Credit Cards

8:25

Traveling With Credit Card Points- Video #3 – A Blueprinting for Credit Card Points