In this video, Matt Blocki explores the timeless lessons of investing amidst a rapidly changing world. He emphasizes the importance of sound investing discipline for achieving long-term financial goals. The discussion includes an analysis of the bond market’s downturn in 2022 due to rising interest rates and its recovery in 2023. Blocki also addresses the stock market’s resilience over time, the negligible impact of election years on market returns, and the positive outlook following periods of high inflation. Highlighting the advantages of diversified portfolios, Blocki advocates for a disciplined investment approach to ensure financial success and stability through the years.

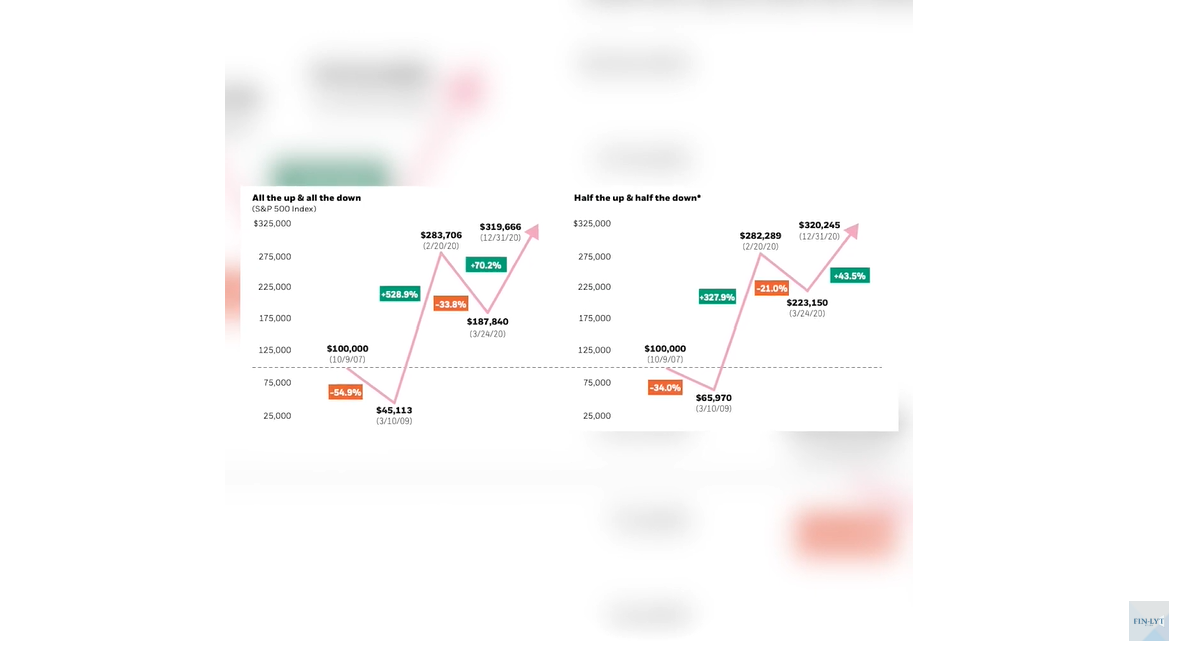

in a world that changes seemingly every day, new technology, we’re on the cusp of change, it seems like around every corner. History, however, when it comes from an investing standpoint, teaches us a lot of very valuable lessons and a lot of things from an investing standpoint, from sound investing discipline, investing really never change. So it’s important as investors that really want to reach long term financial planning goals and having a life by design that’s supported by their balance sheet, not dictated by their balance sheet. It’s important to find these lessons and to make sure that they’re consistently implemented inside your financial plan. So, want to take a moment and look at some of the data that we captured in 2023 and how that’s going to affect us in 2024 moving forward. So, first of all, I wanted to look at bond market. So a lot of people think of bonds as boring, safe money, which they really are. Now, what we found in 2022 was the bonds dropped about 13%. That’s because interest rates skyrocketed, and people that had bond investments paying two or 3%, they weren’t able to go out and sell those to other bond investors who could, with new money, go purchase a bond paying five, six or 7%. So that’s why you see, if you had to sell your bonds in 2022, you’d have had to take a bad loss. And this shows from 1926 to 2013, if you look at the US aggregate bond index, which right now just has an average of a 6.1 year duration, historically, it’s around 4.9, or about five year duration. 2022 was one of the worst years ever. However, if you look at 2023, this fit kind of in the average returns where you’re getting three to 7% to 2023, there was a five and a half percent return in that five year duration bond. And investing after a year like that, the following year is on average return 4.4. So with interest rates coming down or stabilizing, safe money is important to have, especially if you’re retired or if you’re going to have a goal that’s coming to fruition in a short time frame. We wouldn’t recommend to mix this with the equity markets, but it’s really important to understand your liquidity position when it comes to bond investing. Is the money going to be there when you need it the most? And layering the duration of your bonds to have a liquidity plan is crucial. Next up, let’s look at stocks. So if we look at S and P 500 returns from 1926 to 2013, one of the greatest reasons we are big disbelievers in any kind of indexed annuity or indexed insurance product that caps the downside, but also caps the upside is if you look at the data, there are so many years which are 8% or above. And in fact, the biggest block here in the stock market is when you have these great years, typically in earlier mid stage economies that have amazing years. And so 2023 was one of those 26% return, the S and P 500 and the average. If you invest after a year in which stocks had a great year in this block, your average return would have been ten and a half percent the following year. So that’s really good news for investors that want to. Obviously, we recommend always stay in the market. When you look at the really bad years, see how limited those are over here, and you have to go through some of those bad times in order to make sure you’re there for the good times. So you look at how much positivity we see versus the negative. There was 26 years that were zero or negative, and the remaining years, almost over this 100 year period, were positive. That’s why I always say, statistically, the market’s up 75% of the time and only down 25% of the time. So obviously a good year to be in stocks and moving forward, it will always be a great year to be in stocks. Great decade, hopefully multidecades for the rest of your life. Just always having a fail safe and plan, because during those 26 years, obviously, you don’t want to have to pull from anything at a loss. That’s the number one rule of money, is don’t lose money. Okay, so we also have an election year, and actually, statistically, 49% of the population in the world will be voting. Many, many countries across the world have major election years. So there’s going to be, 2024 is really the year of the unknown. What does this mean for the stock market? Well, if we look at historically stock market returns during presidential election years, the first two quarters are typically slow, and then the third quarter and the fourth quarter are much bigger. But we never recommend to mix politics with your investment policy statement. Republican and Democrat, specifically in the United States, have had very similar within 1% differential in returns over history. Sometimes Republicans being better, sometimes Democrats being better. What’s in common is most people that say, oh, it’s going to be bad. Usually it’s good. Most people that say, oh, it’s going to be good, it’s going to be bad. It’s typically the inverse of what most people think best thing is don’t mix your politics in with your investing statements. This is some interesting data on inflation. If you look at the returns following when inflation rates peaked, all but one time in the following twelve months have been positive. The only negative return that we saw was during the financial crisis in 2008, when inflation had peaked. Every other time inflation had peaked. There have been very substantial returns in equity markets and in bond markets. All but one time when interest rates crushed in 2022, went way up, obviously there. So with inflation rates, if in fact they have peaked and now they’re tapering down, that’s usually a good sign for investing. So, some other data I wanted to look at is a lot of people look at what did the SB 500 do last year? It did 26%. Why didn’t my diversified portfolio do that? Well, well, if you have a one year goal, you shouldn’t be invested anyway. So we shouldn’t be paying attention to anything over one years. But if you look at the last 20 years, and this is the S and P 500, so this is if you had s and P 500 investment on $100,000 investment versus a diversified portfolio, 24% large, 24% mid, 5% international, 2% small, 5% emerging, and then 40% between the mix of bonds. So the first period we’re going to look at as a tech bust, SP lost 40, diversified portfolio lost 15. Then the US market recovered great, 82.9. Diversified went up even more, 91 and a half financial cris hit. You lost money no matter what, but obviously less money with the diversified. Now, the next ten years were tough because SP 500 absolutely crushed it, 350% versus diversifying 237. And then there was another down year during COVID and then up year, and then we had a down year during 2022 and then up year. And so despite you feel like, oh, this diversification, I still lost money when the market down and I didn’t make as much money to the upside, limiting that oscillation. If you look at the two results here, 100,000 and straight up, s and p 500 grew to 490,000 over those 23 years, versus if you were in a diversified portfolio, 100,000 grew to 491,000. So you actually essentially halved your risk and got a little bit better of return along the way. And by the way, if you needed money along the way, you had the optionality of which bucket to pull from. Obviously, diversifying from so many levels is the way to go. If you are a long term investor, which anyone that has a financial plan in place, I would categorize as long term investor. Anyone that has a short term goal in place, such as buying a house next year, your money shouldn’t be invested in anything under any circumstances. It should be in some low duration treasury bond, or even cash or a money market, et cetera. So hopefully that data was helpful and obviously excited for the good times ahead in 2024 and more importantly, the decades 1020, 30, 40, 50 years plus where compounding interest in diversified equity markets can really be a catalyst for your financial success.