In this episode of FIN-LYT by EWA, Matt Blocki and Stephanie Bogden unravel the complexities and paradoxes that often accompany financial decisions, aiming to simplify some of the most common financial problems clients face. Matt and Stephanie shed light on the pivotal role of financial advisors, extending beyond conventional problem-solving to address the emotional and psychological facets of financial management. The discussion underscores the irreplaceable value of financial advisors in overcoming the human challenges of regret, stress, and internal conflict, proving that the true value of their services far surpasses any fee—especially when compared to the limited solutions offered by technology and DIY approaches.

Some key points include:

1. Tax Planning and Control

2. Investing Psychology and Inflation.

3. Market Volatility vs. Hidden Dangers

4. Risk Management and Insurance.

5. Simplifying Complex Financial Planning

6. The Holistic Role of Financial Advisors

7. Embracing Financial Paradoxes

This episode is a must-listen for anyone looking to deepen their understanding of financial planning’s complexities while aiming for a life that balances financial success with personal fulfillment and happiness. Whether you’re striving for financial independence, planning for retirement, or navigating family financial dynamics, listen in to discover how a holistic approach to financial planning can address not just the numbers, but also the intricacies of life itself.

Welcome to EWA’s Finlit podcast. EWA is a fee only RAA, based out of Pittsburgh, Pennsylvania. We hope all listeners of this podcast will benefit as we deep dive into complex financial topics that we will make simplified for you. And we hope that this really serves as a catalyst so that you can make the best financial planning decisions for your family and also save time. Welcome, everyone, to this week’s Finlit by EWA podcast. Today I’m joined by Stephanie Bogdan. We’re talking about problems that financial advisors can solve for their clients, and then also what we believe is most important is managing paradoxes that come up. So a question was asked to me recently, is, what’s more valuable? And I think, by far, the management of the paradoxes, because we’re all human, and there’s always internal competitions. There’s regret, there’s stress.

And if we can manage that, we truly believe that’s invaluable. And then your relationship with a financial advisor, the value will be well above the fee. But if your financial advisor is only focused on problems, there’s so much technology, there’s a lot of do it yourself stuff you can do if you’re just trying to solve problems, like investing index funds, et cetera. So, Stephanie, we’ve got tons of examples here. Let’s focus on the problems that a financial advisor should be solving for their clients. What do you think some of the top problems are?

I mean, the top problems, I would say, is knowing, am I saving enough? Am I striking a balance between saving and spending? Am I going to be able to, quote unquote, retire comfortably? I think if you asked a group of people, what’s your absolute number one thing you’d want to solve? The magic equation would be, how much do I have to save now to be able to retire comfortably and never work again? But we’ll get to that, because that’s not actually.

Well, let’s go right into that so you can buy a financial planning software. A lot of calculators online actually won’t do this accurately because there’s so many factors. But, sure, let’s say a client comes to you, and their number one goal is, I want to retire. Right. The reality is this turns into a giant paradox. A lot of times people will say, I’m stressed out. Let’s say someone’s 45. I want to retire by the time I’m 60.

Right.

Very common. If all we do is solve for that problem, typically fast forward. What happens if that person just puts their head down, misses all their kids stuff, as the kids are actually in the house, is so stressed out, trying to make money, trying to save. They get to 60 now. They’ve been so focused on their career at this point, don’t have a lot of friends, don’t really have a close family relationship. And so now the only thing they know is work is their work.

Right.

And so why would they give that up? So they started with this huge problem of, I’m so stressed, I want to work. And now the solution is financially, it’s taken care of, but the solution is all they want to do is work now. So this is what I believe in financial planning is probably the biggest paradox is figuring out how do we exchange time for money, how to exchange money for time, but also knowing that you can’t get the time back. You can always get the money back, but you can’t get the time back.

Yeah, we kind of jumped ahead, but this is probably the meat of what we do and the value that, like you said, the value that we provide. But the biggest thing is you can accumulate and accumulate, and there’s a diminishing return at some point on money. And we’ll talk about that a little bit, too. But like you said, looking to strike the balance between what we call financial independence. I mean, let’s talk about that for a second. I think we try to interchange the word retirement for financial independence more often than not, because that really has like a completely different connotation.

So financial independence may be choosing how much you work or stepping back a little bit as you get a little bit older, being able to make your own hours work remotely, delegate things to a team if you’re a business owner, things of that nature, but not necessarily a full hard stop at age 60 in one day, you’re never going to the office again, you’re never working again, you’re never earning another dollar, you’re never engaged in the business. There’s just such a qualitative aspect to that we strive to help our clients find a way to have financial independence, but also maintain some type of engagement in their life that fulfills them in a way that just having a big bank account can’t.

I mean, it makes you feel good at night, it makes you sleep a little bit better, probably, but it doesn’t make you happy per se, for sure.

And sometimes a good financial planning relationship is many things, but what it’s not is just like a do whatever the client asks. You have to push back and say, why is that important? Why is that important? And get several layers deep, because if you, as a financial advisor solve that problem, you’re really just helping someone wreck their life in the reality. So let’s talk about some solutions around how to manage that paradox. So, first of all, we’d ask, okay, well, tell us what life looks like at 60. What’s changed? If we’re to draw a 24 hours circle that represents your time, want to go into detail how you spend your time right now? Maybe it’s 12 hours of work, 8 hours of sleep, 4 hours of free time. I want to know what you’re doing with that free time.

And then at 60, if you’re so stressed now, if your time goes from four to 14 hours but now your kids are out of the house, I want to know how you’re spending time then. And why is there such a rush to retire away from something when a great life is right in front of you? And we’re still going to recommend to save. We’re still going to recommend. But why not structure a better life today? Let’s try to remove this stress today. Let’s try to knock off some bucket list items today while your kids are here. Let’s also secure the future. But that’s where I think the managing that paradox is invaluable. Plugging your money and your savings rate into a calculator and then telling you, here’s what you need to do. And then meeting every six months to show how your returns.

Literally, my opinion, there’s no value there, right. But having those tough conversations and then executing a financial plan to make sure the money is actually supporting a life by design. Because I would call that first what that client came in and said. That’s a life by default. That’s like what most Americans are trying to arrive at death safely, putting their heads down and just going. But to really live a life by design, typically, and I myself have had many coaches, you need someone to challenge you. You need someone to hold you accountable, and you need someone to have the tough conversations. And really, perspective is everything. And that’s what we’ve had because we’ve had a lot of clients. What’s going to the next one? So let’s say we got to that so late. Clients come into us at 65, right?

It’s a successful physician that’s poured themselves into their work. They’re at the top level of their field. Their intellectual capacity is off the charts. They could show up and do the procedures or whatever. And they’re mentoring young med students, residents, fellows, whatever it might be. They’re having fun so they thought they wanted to retire, but now it’s kind of too late. So what we have to deal with now is not that it’s too late from a financial planning standpoint, most likely they’ve over accumulated assets.

Right. Very common.

And so their identity is really in a couple of things. One is their work, two is their balance sheet, their net worth, but actually reframing that net worth to say, hey, the job description is to support you for the rest of your life so you can go to phase two of your life and figure out your next identity. This is one of the toughest things that a financial advisor has to manage. And there’s a huge conflict of interest because a lot of financial advisors say, what do you want to spend? I’ve got $10 million. I’m going to spend 5000 a month. Well, there’s a conflict right there because the advisor is probably charging an Aum fee. And it’s like the less you spend, the better it is for that advisor.

Sure.

Versus someone saying, wait a second, do you want to leave money to your kids? Maybe, maybe not. It’s not the top priority. And then reframing and actually encouraging that person what a safe spend is, which most likely wouldn’t be in that example. I’m just doing some quick math. After taxes, probably 25 to 30,000 a month is what that person could spend versus the 5000 a month. And then having really good conversations around what gives you purpose. Is it charity? Is it, you could start your own foundation. What is it that you want to do? But again, it’s a huge difference between default and design. There’s lots of paradoxes that exist between that default and the design. And to get there, it’s a lot of work. It’s not just money talk.

Yeah, I mean, I think we can tie this back to what were just talking about too, which the paradox of being financially independent, getting to the big finishing line of retirement, is that oftentimes these clients come in and like you said, there’s a conflict a little bit as an advisor because you’re like, this is great. We can bring in assets under management. We can assist this person with a great portfolio. We can help them do their rmds. All this simple stuff that we kind of probably do with our eyes closed.

But coaching somebody around then kind of making that shift to maybe most likely, I shouldn’t say maybe this person sacrificed a lot of time with their spouse, their children, doing other things that they wanted to do for the sake of this very successful and very meaningful, mind you, and necessary career to now being able to almost, like, backfill a little bit of that. One of the things we see is clients say, well, I’m going to retire. I’m going to spend more time with my family and my kids, my spouse, maybe my grandkids. Well, it’s quite possible that along the way, a lot of that relationship building kind of, like you said, went by the wayside.

So really, I think encouraging someone to be able to go out, go on vacation with their spouse, do things with their kids, do gifting while they’re still alive, not just look down the line, possibly to legacy and inheritance. These are all conversations that have to happen. It’s not just, yeah, let’s roll over your 401K. You can take ten grand a month, we’ll send it to your bank, do what you want to do, and we’ll see you in six months. So it’s a much bigger conversation, and it’s much more qualitative than quantitative, truly. Even if someone has accumulated far above what they actually need to live life. Right.

Yeah, no question. Okay, let’s talk about education.

Yes.

So a lot of our clientele, high income earners, high low time, busy executives, physicians, business owners, et cetera, most of the time, I would say 90% of the time, they’re like, non negotiable. I want to fully fund my kids stuff like their college, maybe private school, maybe college, maybe postgrad, et cetera.

Right.

And so this is where a huge paradox exists, because if I were to say, how could you help your kids fully funding all their stuff would be, like, pretty down the list. Right? The first thing would be, no one’s going to raise your kids for you. And if you let society raise your.

Kids, then that’s a whole nother conversation.

Yeah. You fully funding their education is going to pour gasoline on what society has built. I’d say the first thing is, do you have a career that allows you to have the time to raise your kids as your values, your standards, et cetera? That’s the first thing you can do. If they have to go to school and fully get debt, but you raise them and society doesn’t. I would say you’re a success 100%.

Right.

On the flip side of that, if you are not there because you’re just so focused on making money because you want to fund their stuff, that’s a huge paradox. It’s like you think you’re helping them, but maybe you’re actually hurting them more than you’re helping them. And then they take five or six years to go through undergrad, and then we see this all the time. They cycle. So I think to balance that cycle where you have a really successful parent and then the kid who’s like, oh, I don’t want to go through what my parents did. And then they have kids and they’re like, oh, I don’t want to go through what my parents did, not making any money and living off of like a trust fund or whatever.

And so it’s like this huge cycle, I think, to even that out, there has to be this management of these paradoxes, like, yeah, fund your kids college, but first of all, make sure you have enough time with them to raise them the right way. And part of that is along the way, I’ve seen it very successfully where we have amazing clients that fund their amazing kids college fully and their kids come out 4.0s, fully motivated and just go right off the bat running. And then we see it on the opposite end where it’s fully funded six years later, then it’s like now they’re right back in their parents basement living.

They don’t know what they’re going to do with their life.

Yeah. So this isn’t just an equation of like, let’s save and make sure the money is there. Let’s do that. But let’s make sure we have the right philosophy in place to give them the skin in the game and to put boundaries in place to teach them what made you successful, how you got to where you are, and to pass the values of, most importantly, to your family, to your kids.

Right. I will speak to this one personally, is that I’ve got kids that are all completely different, too. And I think sometimes we apply. Again, this is a paradox where you have your kids and you want to give your kids each the same, quote unquote opportunity. And that’s a word just that’s filled with things on its own. But opportunity looks different for every child. You may have an athlete, you may have an academic, you may have a blend of the two. You might have someone who’s interested in trade or arts. That path does not look the same. And that quote unquote opportunity doesn’t look the same for every child.

And you can’t really assign, like, a dollar value to that because I think you can say, okay, well, I have an academic kid and they’re going to get a scholarship, or maybe they’re not, but I’m going to pay for Ivy League school and they’re going to come out and go to law school or med school, and it’s going to be great. But that opportunity that you gave that child is maybe monetarily more costly than it is to help one of your other children engage in the arts. Right? Go to art school, provide them with opportunity for trades, and maybe that’s monetarily like, that costs a lot less for you.

But it’s the same in terms of the actual opportunity that you’re giving your child to do something that they love, hone skills that they want to learn, and ultimately live a life that they’re designing, which they are going to be happy. It’s interesting. It’s hard to take away the desire and the kind of tendency to say, well, okay, if I give this child $100,000 education, then I need to give this child $100,000 education to give them the same opportunity. But the math just doesn’t really work that way.

Let’s talk about that, because that’s so common. We have clients that have, let’s say they have two or three kids.

Yes.

One kid goes Ivy League and starts making two or 300 grand a year. One kid goes to arts and they’re making 30 grand a year. And so now the paradox is, well, we love our kids all equally. How do we take care of them? How do we make sure? And here’s where I think the paradox is. There’s no right or wrong. Money is not just a means to an end. It should be to support. And if the person making 30,000 doing the arts may be ten times happier than the kid on Wall street. Exactly. The professional on Wall street, not a kid anymore.

So the reality is, now, here we go with another paradox of how do we make sure that our kid making 30,000, who’s used to our lifestyle, that he’s brought up under our roof, that’s maybe like a household income of a half a million dollars. He’s used to staying at a certain type of vacations, hotels, et cetera. So how do we manage that where maybe that child doesn’t value all those fancy stuff, but doesn’t have the financial literacy to know, oh, no, I can’t do that.

Continued to do this on this paycheck.

We see this literally all the time, and now there’s the conversations of, okay, do we favor, do we start supporting that person over this person? Do we set up a trust? Because we don’t think this person is that savvy with money? So again, I’m going to go back to the paradox of making more or having more does not make you more valuable or more successful. But it’s just a paradox that you have to manage to make sure that your kids are okay. And so now back to when you’re raising your kids or after it’s having a financial advisor that’s willing to navigate the whole family dynamic.

Yeah, I mean, it’s really difficult. We can even take it like a step further and talk about if you have, let’s say, three kids in that situation, everybody’s kind of in a different economic standpoint. You have someone who’s a physician, and they’re accumulating as well, all of a sudden for their own retirement and looking ahead 20 to 30 years, you know that person’s likely going to be able to fund all their financial goals. They’re never going to hopefully not be like an extreme amount of debt after student loans are done or whatever they’re doing. But then it’s like, okay, well, something happens to me as the parent. I know that this child’s probably already kind of set up financially for life, and this person might need some more help. So how do you structure that legacy planning and that estate planning around that?

Because you can go ahead and say, great, well, this person’s better off. We’re going to give them 50% of what’s left and 25 here. But then you have to really think about, well, what does that do to the family dynamic after the fact? It’s tough. It’s very tough. The answers to those, I think, are very highly individualized. It’s very much a conversation that isn’t really about the numbers. It’s about what do you need and what does your family need in order to. You want to know that your family is going to be happy long after you’re gone, right?

No question.

These are very far reaching.

All right, well, I got a couple more, and we can talk about the problems, but the next one is run legacy. So best savers are the worst spenders. You accumulate this $10 million net worth, let’s say, hypothetically. We’ll use the physician as an example, because that really puts you in the top 1%. And the funny thing is, people that have $10 million think they have no money.

They don’t think they’re in the top 1%.

No. And the people that have two or 3 million are like, that’s typically what we see. I’m good, but usually they spent a lot, so they have a good balance. And some of them are like, maybe they’ve overspent a lot. So we need to calibrate a little bit. But there’s a sweet spot. Not of, like a net worth or a number, but of how well along the way you’ve calibrated your spending versus time versus spending, time versus working, saving versus spending. How well you keep that as an artwork, I believe has a direct correlation to the happiness factor that you can have for the rest of your life. Because if not, you’re going to be constantly overthinking, constantly stressed about, am I doing the right thing? Am I not doing the right thing? Et cetera. So let’s talk about.

Here’s what we see with our retired clients. We get there and let’s talk about a three or $4 million net worth client. And just in general, I would say 90% of the time, the wife’s like, we just fully funded our kids college. Our kids are good. They all own a house. We help them with the down payment house. Can we please start spending our money?

Right?

And I want to go travel. I want to do all this stuff because typically the husband’s like, the cheap one, and the husband’s like, I want to check my account every day. I want to see this grow. I want to see this grow. And if it grows, maybe. And then if it grows, then it’s like, no, this is so fun. So this is where we see a huge. Yeah, there’s a misalignment, sure. But then it goes further. Then we start asking the questions of, do you want to leave money to your kids? And typically we see one of two things. One, it’s like, you know what? We took care of them, so, well, if there’s money left, sure, we want it to go to them. We go to taxes or government, but we don’t really care.

And then the second time we say is, yeah, we definitely have money left over for the kids. So let’s focus on the kind of the wait and see approach.

Yes.

So now the husband doesn’t want to spend money, the wife does. And now I ask the question and they say no, maybe like, if it’s left over.

Yeah, if it is.

Well, your actions are telling me all you want to do is make your kids like multimultimillionaires. Because if you don’t start spending your money, here’s what’s going to happen. It’s going to grow, and your health is going to kick in, and you’re not going to be able to do this travel. So the spending versus legacy and figuring out the relationship dynamics between two spouses is absolutely huge. And this is something that the investments, the taxes, all that kind of stuff. I mean, yeah, there’s hundreds of thousands, if not millions of dollars of savings a good financial advisor can do. But I think more important than that is getting the philosophy down, because what does any of that matter if the money is not even supporting the life you want to live, right?

And that is, by far, I think, one of the toughest ones to manage. And you’re going to see this the biggest wealth transfer in history over the next 2030 years. So being able to navigate these conversations or as a client, being part of a good conversation like that is going to be the make it or break it of whether you had a successful retirement plan, not from a financial result. You could be the richest person in the graveyard. But I’m talking about by the life by design ranking, for sure.

I mean, this is crazy because there have been so many clients that I’ve come across in the last like 15 years where they have no idea that the behaviors that their spending behaviors that are going on in their retirement are going to inadvertently leave them with a very big, I don’t want to say a state problem, but with a state to deal with, I mean, most people think, well, I’m going to spend and spend, and I might have $100,000 left when I’m 85 or 90, but that’s typically not the case. So like you said, navigating these things are really important and thinking about the age factor and the health factor.

And there are people that say, well, okay, I’m going to do, I’m going to spend a whole lot in the beginning, and then my expenses are going to go down so much. Probably not. They’re just going to shift. Like, you might spend more of your money in the early years of your retirement, traveling, doing the fun stuff, hanging out with your grandkids, going on vacation, all these things. But then that shifts into potentially health care costs. What happens if you get sick? What happens if you can’t live your life the way that you were and you need assistance? So maybe the expenses don’t go down, but they change. So that’s kind of a thing to talk about, too. But you either are going to spend it or your kids are going to spend it, right?

And I think you use the term like, you should probably take a great vacation. If not, you’re setting your kids up to take a couple of those later on. So you really have to decide where that balance is. But on the other side of the coin, there’s people that say, yeah, I want to leave as much as I can to my kids. I want them to have everything in the world when I’m gone.

That’s a whole, that’s a paradox in itself, because my opinion would be, why, when you’re gone.

Yeah.

Why not start transferring it now to see how they interact with money? Are they responsible?

Right. That’ll help guide your decision making over the rest of your.

Absolutely. Is gifting money to your kids now. They’re going to need a lot more now because today’s generation, it’s the first time in history, I think if you’re in your lower, you’re less successful when you adjust for inflation than your parents were when they were 30.

That’s an amazing statistic.

That’s the first, my mind, the first time in history. Usually it’s like the goal is you want your kids to be more successful than you. Well, this is the first time in history kids are getting out, interest rates are high, economy, whatever it is, costs.

Of education, just housing, everything not happening, to be able to kind of get into that starter home and have a starting point, and that’s a really big hurdle anymore. So, yeah, I mean, it’s a concern for people like us who have young kids, and I have a kid who’s going to be in college in six years, and, yeah, it’s like, okay, well, what is that’s going to look like for her? So really thinking that through and thinking about now versus later and thinking about time, value of money and what even investing in private schooling is something to think about, too, because do you invest in tuition now at the cost today in hopes that parlays into potentially, like, scholarships or whatnot at a probably higher price tag six years from now? I mean, it’s a balancing act right there.

Absolutely.

Lots of decisions that aren’t, they’re not black and white, they’re very gray.

And I’m a big believer in that. You become the average of the five people that you surround yourself with. So if you’re in a fancy neighborhood with other people that all are doing XYZ, it’s going to be really hard for you not to also do XYZ. Pressure of spouse, pressure of kids, et cetera. So one good question I always ask myself is, are my actions actually my actions? Are they someone else’s influence on me? And are my goals? And so it took me ten years to learn how to really realize when something was actually my actions versus someone else influencing me versus. So, in a financial plan that exists, and it’s so important to set time aside, with a good advisor and figure out are my actions, are my time, is my alignment actually mine, or is it influences?

Because life’s just whirlwinding around me, I don’t have the time to really think for myself.

I mean, that’s the whole, like, controlling your money temperature conversation. I always think about it. If you drive into a neighborhood and, like, you’re in a cul de sac for some reason, this always the visual pops up to me. If you drive into a beautiful neighborhood with a cul de sac. And the homes are probably similar in architecture, but if you also look around, there’s a lot of other similarities. So it’s not only the homes, but it’s the vehicles, it’s the decor, it’s everything. So there is this tendency, like you said, to basically, I don’t want to assimilate to your environment and to pull in all of these traits and these behaviors of those that are around you, even if you’re not cognizant of that.

It might not be your spouse, might not be your parent, might not be your child, it could be anyone that you’re in contact with or in your environment regularly.

Yeah, it’s interesting.

I love it.

Okay, so a couple of other ones to bring up. So, one is a huge tax. Everyone is so focused, and I’d say most cpas are focused, how do we save taxes today?

Right?

But if that’s all you do, just wait till you retire and it’s going to be a huge paradox that kind of slaps you in the face is like, what your tax bill is going to be then is going to be totally unexpected, with Medicare surcharges, tax brackets potentially going up, and rmds forcing you into higher tax brackets on top of your Social Security, on top of the dividends in your non qualified account. So you have to have a good balance of roth versus pre tax, and making some tough after tax decisions today to set yourself up for the future. Not only that is the control factor, because the more you try to that immediate satisfaction, that savings today, you’re actually giving control to someone else. So for me, it’s not even, I don’t care about taxes.

I’ll pay more taxes in the future, give me control for the rest of my life, and I’ll take that any day, and I’ll pay whatever it cost, essentially. And so the reality is, that’s why I love Roth money, where I have full control forever of it. No matter what the government does. I take it when I want to, no matter what the government does with taxes. It’s coming out later at 0%. That’s why I love it.

At least a third of your assets for retirement should be in your tax free.

Yeah. So the other thing that I think is very interesting. So we’ve talked about the worst savers and spenders. I would say there’s a huge paradox in the psychology of investing. So a lot of investors are like, I want to live off of interest. I don’t want touch principal during retirement. Well, the way you can double, triple, or quadruple to keep up with inflation is you got to have a good exposure to equities in retirement. And so principal is going to fluctuate over time. And so what’s going to make you feel safe in the moment long term is going to be devastating if you want to put yourself adjusting a stable and move off interest, and inflation is just going to crush that.

And if you enter retirement with $2 million and you live for 20 years and you still have that $2 million, well, just because of inflation, that’s cut in half. You only have a million dollars at the end, even though it’s a $2 million balance. There’s lots of psychological paradoxes, of mindset that’s going to prevent people from making the right decisions without guidance. I don’t want touch principal. But you’re saying you don’t want to leave money to your kids. I don’t want touch principal. But you’re saying you want to maximize income. That’s not necessarily how you do it and reduce risk.

And it’s a very od statistic that we’ve talked about this in a previous podcast, is that actually the rates on fixed income and the yields on fixed income are actually, over the long term, have been more volatile and have more standard deviation than the stock market in general than the S and P 500. And it seems contradictory, but in reality, it’s in the numbers.

This is one. I found an article, termites do more damage than tornadoes.

I didn’t know this, actually.

Yeah, this is crazy. So termites cause $5 billion in annual damage.

It’s incredible.

And I love this because termites, you don’t really see, they’re kind of happening behind the scenes. The termites could be inflation that you see a little bit. Oh, that coffee cost a little bit more. The termites could be a.

It’s like a slow eating away at the foundation of my care brackets.

My health care went up a little bit.

Right.

Or could be taxes went up a little bit. Well, slow. But surely 5 billion per year in damage. Now, tornadoes only cost 400 million. Now, if you think of tornado, you think, oh, my goodness.

Like catastrophic, right?

So my analogy here is a tornado is a market downturn. 2022 SP drops over 20%. 2008, it drops over 40%. Those are tornadoes, right. Well, if you’ve got a good plan, if you got a good shelter that you can go hide in for literally a little time, you’re totally fine. And if you’ve got a good fail safe in place, zero damage to you.

Right.

The termites, if you don’t go check and calibrate, devastating.

Absolutely.

It could cause your whole house eventually to collapse. So people worry so much about market downturns when they’re totally normal. In long term investing, it’s healthy. The ups and downs, they’re just business cycles. Every business goes through cycles, ebbs and flows. But you have to have a balance sheet that supports those so you can still live your life by design. Even if the market’s down, you’re not pulling anything at a loss.

No, I love that. I mean, just something can slowly, in small little pieces, can completely erode your plan. And by the time you realize it, like you said, the damage has been done and it’s almost impossible to repair completely without ripping everything down and starting over again. Unbelievable.

All right, so I’m going to just rapid fire through a couple more. There’s a risk versus return paradox. I love this one because everyone’s like, did I beat the SP 500? I’m actually doing a couple of videos on this. Asset allocation is not only will beat the S and P 500 in a lot of time periods, but when you actually are like, oh, I need to use that money for my life, then it’s ten x more efficient than just investment. So more videos on that. The second one is the risk versus return. Just to tie that up, we want the highest rate of return, but we also need a low amount of risk to correspond. And marrying those two things is a paradox, because we’re humans, we’re competitive. We want our balance sheets to, well, outseed what we actually need.

But getting that dialed in and having that be a support system can really allow people to stop gambling and make healthy financial choices.

Absolutely.

Second one is insurance. A good financial planner should be advising on insurance, right? Not necessarily selling it like property and cash, but advising, here’s what you need, because if you don’t have it could be catastrophic. If you have too much of it could be catastrophic because you’re spending too much. That’s a paradox. The problem is getting the insurance in place. But more importantly, the paradox is making sure you have the right amounts and calibrating that as you go. There’s so many simplicity, complexity, paradox. Obviously, if you’re high net worth, there’s going to be some complex stuff if you want to save millions of dollars in taxes. But a lot of times, what makes people successful is keeping things simple.

So being able to navigate that artwork, if something does get complex, putting in terms and analogies that the clients can understand, and making sure the time involved in the more complex stuff is off the client’s plate. That’s how I think a good financial planner is, making sure there’s an understanding and education that aligns with the philosophy, but then managing it all well, and.

To kind of negate, I think, making those terms like equivalent, where complexity equals something that’s better or more sophisticated, or that’s going to be more effective, that’s not necessarily the case.

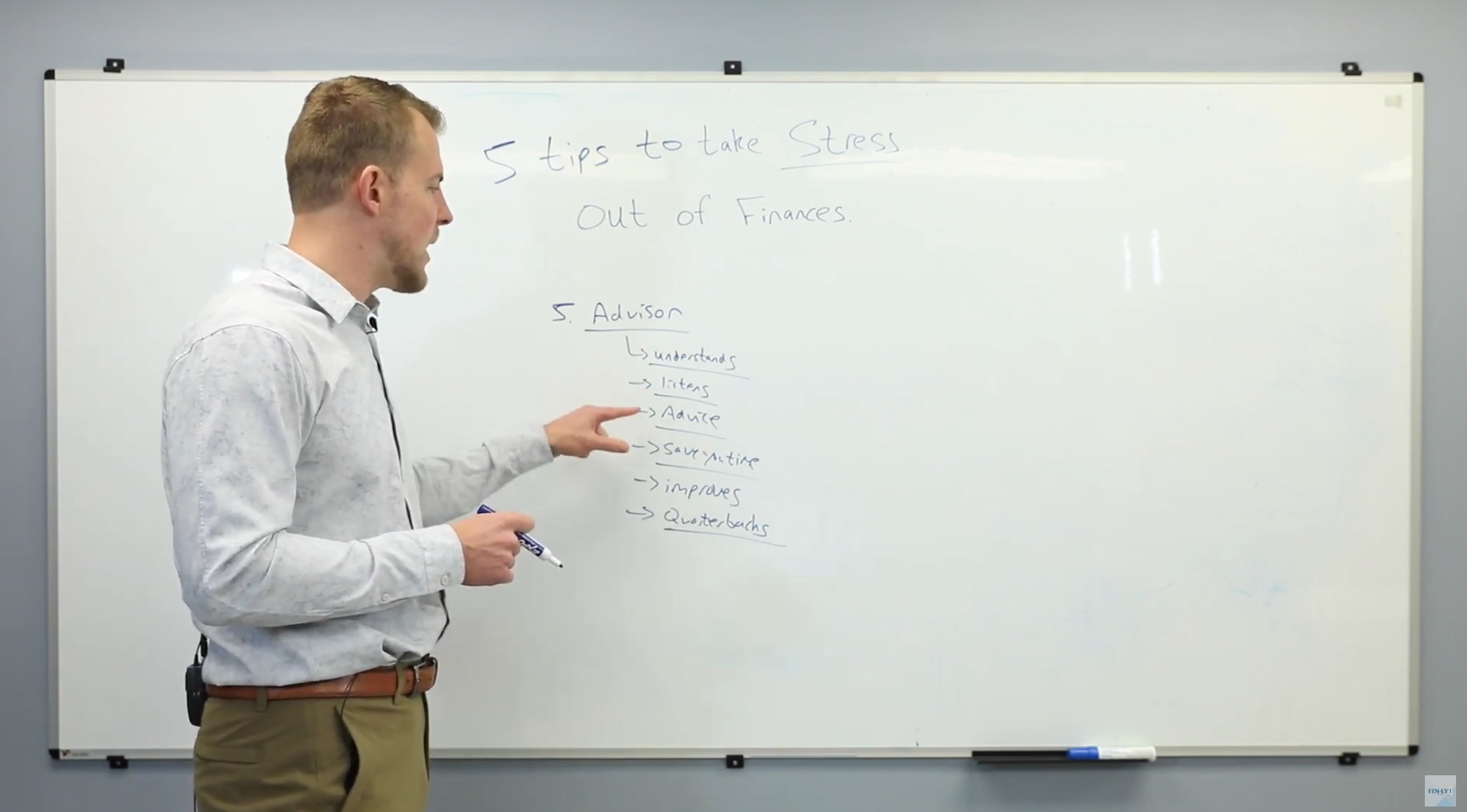

Absolutely. Okay. We obviously love, I think, the management of the paradox, especially if you’ve had some success in life, it just naturally comes. But as far as problems go, there’s many problems a good financial advisor can play. It’s going to be well outside of the fee. But I would break these down into income tax benefits. So, claiming the right deductions, getting the right retirement plans in place, tax deferral, tax bracket arbitrage, that can be worth thousands or hundreds of thousands or millions per year, literally, depending on your net worth. The second would be investment planning. So there’s been many studies from Vanguard, from Dalbar, et cetera. What is a good financial advisor worth from an investment perspective? Stephanie, what are some of these, and how would you value those?

Yeah, I mean, from an investment know, rebalancing, diversification. But as we kind of move down our chart is, like you just mentioned, insurance planning. One catastrophic event in life that could be prevented is worth. I can’t even quantify that in terms of, you can’t get that time back, delegating of benefits, making sure that we’re taking things off of our clients plates, making their lives more simplistic outside of what’s probably already a complex career and family environment. And then the big thing we just talked about, this entire podcast, is just managing the expectations and the behaviors that sometimes are very contradictory, very conflicting, whether it’s just with yourself or within your spouse, your family relationships.

Absolutely. We’ll put this slide on the end of the screen. If you’re watching this on YouTube or Spotify, this literally quantifies the value on a percentage basis or a dollar basis of income tax benefit planning, investment planning, estate tax planning, retirement planning, managing Medicare rates to tax rates to withdrawals safely, maximizing how much you can spend, insurance planning, delegation, and then the paradox are all at the end and all says priceless. I love that. So spend money to free up time, ensure things actually get done. Debiasing financial coach I would end the most valuable one that’s not on here is the management of the paradox, not just solving the problems, but managing the paradoxes that occur when the problems get solved. Because more and bigger problems will come if you don’t.

And a quote I love is this college basketball coach I’m trying to remember where I heard this but said everyone thinks if I get through school, if I get through high school, if I get through college, if I get my first job, if I buy my house, if I life’s going to get easier, when the reality is I can speak from experience, every milestone, life actually gets harder. But what you do is you learn how to handle hard better, and so life gets better. And so that’s what I would use analogy for financial planning. You could solve all these problems, have all this money, life will actually get harder as it goes. But if you manage the artwork of managing the paradox as well, it will get easier and it’ll work for you, not against you.

Agreed. Very well said.

Well, thanks for joining and we’ll catch everyone next week. Thanks for tuning in to our podcast. Hopefully you found this helpful. Really hope this is as beneficial and impactful to as many people across the nation as possible. So hit the follow button, make sure to rate the podcast and please share with any friends or family members that would also find this beneficial. Thank you very much.

In 15 minutes we can get to know you – your situation, goals and needs – then connect you with an advisor committed to helping you pursue true wealth.

EWA, LLC dba Equilibrium Wealth Advisors, is an SEC-registered investment advisory firm providing investment advisory and financial planning services to clients.

Investments in securities and insurance products are not insured by any state or federal agency.

To view EWA’s public disclosure, registration, Form ADV and Part 2B’s, click here.

To view EWA’s Client Relationship Summary (CRS), click here.

COPYRIGHT 2024 EWA, LLC. ALL RIGHTS RESERVED