Welcome to EWA’s Finlyt podcast. EWA is a fee -only RIA based at Pittsburgh, Pennsylvania. We hope all listeners of this podcast will benefit as we deep dive into complex financial topics that we will make simplified for you.

And we hope that this really serves as a catalyst so that you can make the best financial planning decisions for your family and also save time. Really excited to bring today’s episode on real estate.

Real estate is one of the biggest topics that clients will ask questions about and what are the associated tax benefits. The overall theme of this video is education on what does a real estate investment look like, what are the associated tax benefits.

If you are primary job as a W -2 employee, then it’s going to be very hard for you to become an active participant in the real estate. And in general, the tax benefits are going to come from a passive structure, not an active structure.

So in this video, we break this down in detail. Just want to give an extra disclaimer. We are not CPAs. We’re not preparing your tax return. So we would recommend before making any real estate decision, please consult a professional for tax advice.

We hope this is helpful. And before we get started, we want to clarify a few things on what an active participant in real estate actually means. So the IRS gives a test. And I’m going to rattle these off.

So as a real estate professional, a taxpayer must satisfy one, perform more than 50% of services in the real property, trades, or businesses. That’s the 50% test. And two, perform more than 750 hours of service in real property trades or business.

And three, material participate in each rental activity. So, as you can tell, if you’re working as a full -time employee somewhere and this is just a side investment, it’s going to be very hard to qualify as a real estate professional.

So there are still many tax benefits as you’re building your balance sheet of real estate, but for most those are going to come from a passive basis, meaning those aren’t going to do any benefit to the W -2 side of your income, which climbs the federal tax bracket very high.

There will be benefits for most as a non -active when it comes to offsetting other passive gains such as portfolio gains, maybe if you’re selling private equity investment in a gain, etc. So please reach out if you have any questions and we hope this episode is as helpful as possible.

Welcome everybody to this week’s FinLit podcast. I’m joined here with Jameson Smith and we’re talking about real estate investing. Real estate investing is something we get questions about all the time from our…

Physician clients, executive clients, should we be investing in real estate? The stock market volatility I’m a little bit sick of. I’ve heard about tax benefits investing in real estate. So today we’re talking through an educational approach on one of the pros and cons, what are some considerations?

How do taxes work? Will the taxes actually be beneficial to you as a W -2 income earner? Or what needs to take place for the taxes to actually be beneficial to you? So let’s get rolling first with just a general overview.

So James, as a percentage basis, for our clients that have done real estate investing, how many would you say have said this is a no -brainer looking back? I’m talking about people that have been doing it for over 10 years.

How many people have regretted it? I would say, so we’ve seen it work well, and we’ve also seen it work very poorly. I would say more so poorly than well. I think just talking from people that have done it and advising clients, I think that it’s just like any other investment.

Number one, don’t invest in anything you don’t understand. And number two, it’s probably going to be a lot more time and energy than you anticipate. And so if you want to, like if you enjoy real estate, learning about the real estate market and putting the time and energy into it, just like running a business, then it can be well worth it.

But I would say to directly answer your question, probably more has gone bad than good, I would say. With our small niche of busy professionals. So our clients are not real estate professionals who this is all they do.

These are clients working typically in their top one percenters, they’re working 50, 60, 70, maybe eight hour weeks as physicians, executives, et cetera. And they’re attempting to do the real estate on top of their job.

Just to make that clear, because if this is your profession, obviously, so you can hit the ball out of the park with real estate. So we’re talking specifically with, should a person that’s not a real estate professional be dabbling in real estate?

Matt, what, I know you’ve a good way to talk clients through this. What are the three things, whether any investment, stock market, business, real estate, what should be considered, and then I think this is a good segue into how you can view a real estate investment.

Yeah, no question. So the three factors we decide we recommend to look at. One is the first one that clients want to look at is returns. And returns are important. So returns are something we look at.

What is the return and the risk associated with return? The second thing, when you think about what’s the purpose of a human money? Mexico usually gets to produce some kind of freedom, right? Freedom from having to work, maybe wanting to work instead.

Education for your kids, setting them up, retirement, or… just general financial independence. So the return is important if it’s achieving the goal. The second thing is time, because time is only non -renewable resource.

And a lot of times people forget about time, and they focus on the highest returns, and then they accumulate high net worths. And now they’re more or less, their balance sheet is the master of them versus them being the master of the balance sheet, where the balance sheet is supported in their life by design.

So time is a huge factor. And then the third thing is peace of mind. And so peace of mind with real estate specifically, we’ve looked at it. We’ve seen it work both ways. Sometimes people like physical assets.

They’re not looking at Zillow prices every day. So if you look at a $500 ,000 house, I’m not looking at it fluctuating every day. When reality it is. Like if you had a house and you tried to sell it that day, and you couldn’t, does that mean it’s worth a zero?

No. Well, the same thing works with the stock market. But the problem with the stock market is you can look at it every second if you want. And so you do see this fluctuation. So emotionally, we’ve seen sometimes real estate can provide peace of mind just from that versus the stock market.

And sometimes it can ruin the peace of mind. If you’re not delegating properly and you have a rental home and you’re working a stressful job and now you have a tenant complaining about the toilets broke, that’s certainly not helping with peace of mind.

But those are the three factors that we look at. Awesome. Yeah, I think that’s important for any investment in real estate, especially. But yeah, I think now we can get anything else before we get really nerdy into the apps.

Yeah, absolutely. So I’d say in general, even with property management, if you’re in a part of a real estate investment and you’re doing this alone, it’s going to take a lot more time than you anticipate.

It’s not as easy. When people talk about real estate in general, it’s kind of like someone talking about stocks they picked. They’re always going to tell you about the good ones. Or if they’re betting on a game that’s throwing $100 bucks on a NFL game.

They’re going to tell you when they win. But the majority of people lose in the end. So with real estate investing, just be careful if your friends have. It’s amazing, real estate deal. We find that when people talk about investments, we’re in a very culture of showing lives that really aren’t our lives with social media.

Just be really careful when you think, oh, it’s that easy. It’s this profitable, probably not actually the case. So just make sure you gather the right information. But let’s go right into some of the tax benefits.

One thing I do want to add on that, I think that with social media and everything, we’re in a culture of quick, dopamine, quick satisfaction. And so I think real estate, and just like you said, stockpicking, for whatever reason, it gets put in that category of this get rich quick thing.

And there is no get rich quick. Anything, anybody that’s. been really successful, came out of like a lot of hard work went into it no matter what. So I think it’s really important to understand that will be more work than you anticipate generally.

Statistically people that get rich quickly, it ends quickly. Yeah. So, but people that get rich the right way stay rich. Okay, so James, to talk to us about if someone, now let’s talk about investment real estate.

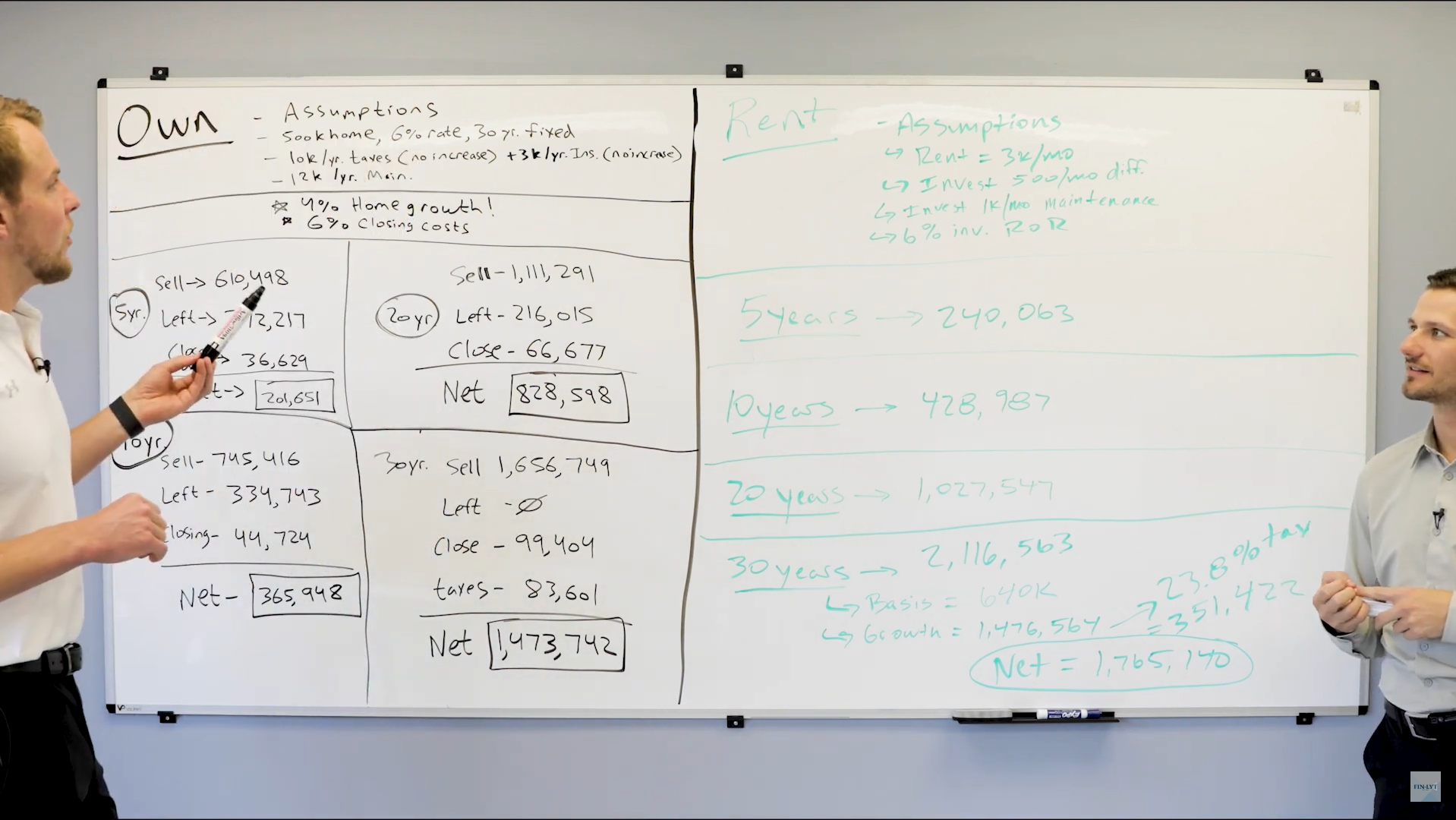

This isn’t someone, you’ve got your primary home set, and we’ll talk about the benefits of a primary home in a second. Let’s just cover those right now actually. So primary home, there’s really two major tax benefits to primary home.

One is if someone is not using the standard deduction, the standard deduction right now is $13 ,850. Single. Single and double that if you’re married, finally jointly, right? So if your salt, state and local tax, which are capped to $10 ,000, and your mortgage interest, both of those are above that standard deduction, which is almost, you know, $27 ,000 in change.

Then instead of using the standardized deduction, you can actually itemize, and then the mortgage interest is a useful tax deduction. For most people, the majority of the population, like 90% of the population, they’re not going to be in a house big enough or mortgage big enough that the mortgage interest is actually beneficial for their taxes.

The majority of taxpayers use the standard deduction. They don’t itemize their taxes. So one common myth is that the house isn’t going to help me tax -wise. Well, no, it’s not. It’s only going to help you tax -wise if you have a house that’s really big, an interest that’s really big.

Do you want an interest that’s really big? No. That means you’re paying someone else, you know, you’re paying a bank to help them stay rich. So one benefit if you do itemize is you can write off the mortgage interest up to $750 after the Trump tax changes legislation went through.

It’s $750, people before the Trump tax code. It was higher than that, but now it’s 750. You purchase a new house up to 750 of a mortgage tax deductible. The second thing is if you’re single and you lived in the house, your primary house we’re talking about, two of the last five years, and you sell it.

Let’s say you bought it for 500 ,000 and you sell it for 600 ,000. That gain will not be taxable if it was truly a primary residence the whole time and you didn’t run that out. Up to 250 actually of a gain is tax -free if you’re a single person on the gain of a primary residence as long as you’ve lived there two or five years.

That’s 500 ,000 if you’re married. Hypothetically, if you purchase a house for half a million dollars and you’re married, you could go sell that 10 years from now for a million dollars and not have any capital gain taxes.

Good tax benefits of the primary mortgage really boil down to those two factors. Now let’s say someone has their primary mortgage and now let’s say that they are starting to dabble and purchase. the investment properties.

So there’s residential properties and commercial properties. The best, you know, easiest to understand deduction is depreciation. So break down how depreciation works for us, James, and residentially and commercially.

Yeah. So this is probably one of the biggest tax, maybe the biggest tax benefit of having rental properties or investment properties has to be done correctly. But basically what depreciation is, it’s the wear and tear of a property that occurs over time.

And then you’re able to take a tax deduction on that. So there’s an accounting mechanism where basically you can take it all in one year. I don’t really know if there’s any situation where you can think of that that would make sense.

For accelerated depreciation. It’s if someone’s selling a big gain that year. Yeah. Maybe if you have, they sold another property or something, but generally spread it out over 27 and a half years if it’s a residential building.

So you have just like a rental house. And basically, let’s say you bought bought this property for $1 million. Literally divide that by 27 and a half. And this is like closing costs. Some other things could be affected, but just for simplicity here, divide that by 27 and a half.

That’s about $36 ,000 and some change per year in depreciation expense for the next 27 and a half years. So that can be used to offset income. So if you have 30 ,000 of rental income coming in each year, the first 36 ,000 essentially is tax free because of that depreciation.

The I guess the caveat is then that works off of the basis. So if you bought that house for $1 million and you’re depreciating $36 ,363 per year, let’s say 10 years from now you go to sell that house, the basis of that house.

And obviously if you put in any renovations or anything that would go back and assume that didn’t happen, the basis of that house now $363 ,000. comes, works off of that basis, and now the basis is 636 ,000.

So when you go to sell the house in the future, that you’re going to have a larger gain versus if you just sold it immediately and that basis was higher. But high level overview depreciation allows you to offset the rental income from a tax standpoint as you’re depreciating that over the 27 and 1 1 half years.

And then for commercial buildings, similar thing, but you can do it over 39 years. So same thing, take the cost basis divided by 39, and that’s what could offset income. And you said, thanks for breaking that down so clearly.

So if you had a new building you purchased, let’s say hypothetically, it’s a commercial building, it’s an office building, and you depreciate it, then you have other tenants that are paying your rent.

That depreciation will help offset the rental income. So you won’t have to pay tax on the rental income up to whatever that depreciation is. You can also do what’s called a cost segregation study. So there are certain parts of the building if you do improvements, say an HVAC, new HVACs, that can all be accelerated to take in one year.

So if you have a big income year, a passive income year, the cost segregation study could be really beneficial to offset that. However, one, so let’s make, I’m gonna make a case for how real estate could be amazing.

And we could never pay taxes on real estate. So let’s say hypothetically you buy a million dollar house and you get the 36 ,000, and let’s just say this is a residential property. So you have 36 ,000 in change of depreciation.

You’d exactly 36 ,000 dollars a rent. And so you’re never paying taxes on that rent. Now, 10 years from now you go and sell that house. Now your basis isn’t a million dollars. Your basis is a million dollars minus the 36 ,000 dollars less.

It’s now 640 ,000 in change is your basis. But we’re gonna talk about this in a second. You could do a 1031 exchange, which is, you transfer instead of paying the gain, let’s say that million dollar house that now is a basis of 640 in change.

You’re now selling it for 2 million. We can take that 2 million and do a tax rate transfer as long as we go directly into another property. And you’re not gonna pay any taxes on the gain. The basis gets transferred over.

And then hypothetically that property I could keep for another 30 years. And then depreciate that, get rent told, depreciate that, I’ll be tax free. And if, this is a big if, the tax code holds up over the next, let’s say 50 years, and I die, my daughter, been my beneficiary, she could receive that property and get what’s called a step up in basis.

Step up in basis means, if that property is still, has grown from two to three, my basis was stuck at 640 from the original 1031 exchange. her new basis when I die would be three million. So hypothetically, I didn’t pay taxes on the rent for building one, I didn’t pay taxes on the rent for building two, and my daughter received it, capital gain tax free, now she’d still have federal inheritance taxes, but there are some big benefits in the long term with real estate.

And that’s just a case analysis. If tax codes stay true for like the next 50 years, that could be really beneficial from a tax perspective. However, personally, I’m very busy, and I’m very passionate about what we do here at EWA.

I don’t like distractions outside of EWA. And so real estate to me would be, even my primary home is a big distraction to me. You add other people in that house, and it would just be a no go. So the big assumption there is you have to be okay as a landlord for your entire life.

And for me, the tax benefits are not worth. The stress. and the time, even if I have a property manager, to address that. However, some clients have the question of, well, it sounds really tax efficient.

Well, if that client’s a W -2 income earner, making a million a year, would they actually benefit them tax -wise? So let’s just say they put into it, they have the depreciation, they have the rental.

Let’s say they didn’t have the rental income to offset all the depreciation. Can that depreciation then help their, let’s say it’s a physician making a million dollars a year, would that help them lower their taxable income on their regular income?

No. Why is that? Because it’s so active, basically we have break down active and passive income. If you’re a W -2 physician working at a hospital, that’s active income. You’re actively doing something, putting time in, putting your skill set in to earn that income.

And if you’re not classified as a real estate professional, which we can get into in a second, it’s active, it’s passive income. So passive income cannot offset active income. Okay, so there’s two universes here of income, right?

So there’s active, let’s say a doctor’s making a million a year, and then he has this totally separate universe of passive. And so let’s say that’s 50 ,000 a year of a deduction. That universe stays over there.

Like that can offset stock gains. Stock losses could offset real estate gains. So everything that’s passive in this separate tax universe can help each other. But if you’re a high income W -2 active employee as a physician, executive, et cetera, the real estate is gonna operate in that separate universe.

It’s not gonna help your universe of your main income, which is probably the primary goal of why you’re investing in real estate for tax benefits. It’s not gonna do you any good. And unless, what? If you’re you have to designate on your tax terms at your real estate professional, what does that mean check a box?

But what that means actually is you have to work for 750 hours per year I believe the math’s like 15 hours a week is what it comes out to roughly somewhere about 15 to 20 hours a week So if you’re a busy physician and you’re working, you know, most physicians that I know don’t work 40 hours a week They probably work 60 hours a week Where are you coming up with the other, you know, 15 or 20 hours to do that?

There are people that do it, but I would say generally that’s not realistic. And so that’s a huge You know the IRS is gonna look at that and be like you’re working. You’re making a million dollars a year as a physician There’s no way you’re a real estate professional most likely So if you again back to like if you’re doing this full -time And that’s your job and you’re managing these properties you’re flipping houses or something like that very easy to check that box And your tax returns and then then it’s active income So just in general, I mean, this is where the IRS kind of puts the stop to all the tax craziness.

If you’re a million dollar per year income earner, a partner, an attorney, an executive physician, you don’t have the time to be an active real estate participant to be managing this for 750 hours a year.

So therefore, the real estate investments that you do can be very beneficial from a passive universe. It’s not going to do anything for your active universe, which is the majority of your wealth. So that’s where I feel a lot of people are misunderstand and misled.

Not saying that real estate can still be an amazing investment, amazing tax benefits. That’s very misunderstood, where most people think they’re actually in a tax benefit. It’s going to offset their W2.

Not going to happen unless you’re an active participant. So now let’s talk about Airbnb’s. So if you have a house that’s an Airbnb, the rules are a little bit different. You don’t need 750 hours. What you need is you need to be the highest participant in renting and managing that property.

And if you do that, there’s no hour test. You pass the test to be an active participant. Again, what that means is depreciation, expenses, fixing up the property. Those could first offset the rental income that you’re getting from the Airbnb tenants.

And then if there’s anything left, it could offset your W2 income. So this is a hack where it could work out. It’d be a very high audit risk though, because if you have a salary high enough to be looking for all these tax benefits, you probably also don’t have the time to put in to qualify as an active.

Because that means you have to have put in more time than the cleaners who are flipping it every time. The people repairing it, the property manager. And typically when you look at it, someone busy and successful, they’re not going to have the time to be the number one person putting in the time to be an active person.

Totally. Can you break down, I think it’s important too, the tax difference, how passive and active income, the difference in taxes? Absolutely. So active income. from a, there’s several taxes you’re gonna pay.

You’re gonna pay federal, starts at 10, 12, 22, 24, 32, 35, 37, it goes all the way up to 37. That’s in the mid -600s, anything above the mid -600s. If you’re married, fine, jointly goes above, it goes to 37.

And that act of universe, in some states you pay state taxes, in some states you pay local taxes, and you pay social security taxes up to about 160. That’s another 6 .2%, plus you pay Medicare taxes on that money as well.

So there’s federal, state, sometimes local, sometimes state, sometimes local, the Medicare and social security. So basically five taxes you pay on the active. On the passive side, it’s really just two.

You pay, and it depending. If it’s short, sometimes the passive side, if it’s short. term income, it can be taxed the same way as active side. It can’t be used to offset the active side, but it can be taxed that high.

And if it’s a long term, like if you hold a property and flip it, if you hold it for more than 12 months, it can be taxed as a capital gain rate. And capital gain rates are either 0, 15, 18 .8, or 23 .8.

And those are all dependent on how high of an income. So if someone’s making 100 ,000 a year, they’re going to pay 15%. If someone’s making under 40 ,000 a year, they’re going to pay 0%. If someone’s making above in that top 37% bracket on the active side, they’re also going to pay the highest capital gain rates of 23 .8%.

That’s just a high level, quick, concise overview of the active versus passive. Awesome. This will be a good segue into another question that we get all the time about holding real estate in LLC. But one thing actually on that too, so if you’re flipping houses, we have clients you work with that will flip a couple of one or two houses a year.

If you’re doing the actual work, you can qualify as an active income that you’re the one doing the job to earn that income. So one opportunity from a planning standpoint, again, this is totally case by case specific, but you’d have the opportunity to open up a 401k or SEP IRA or some sort of retirement account through that if it’s active income.

So it could be some tax benefits, an opportunity to save more money for retirement. But one question we get all the time, should we hold real estate in an LLC? If we think about an LLC, I like to think of an LLC as just like a vehicle, a mechanism to hold an asset.

And so if you have rental property, yes, it can be a good idea. Obviously consult with an attorney to get specific state by state legal advice, but could be beneficial to hold the rental property inside of the LLC.

And then if a tenant ever sues you or something happens from a liability standpoint, your personal assets can be protected because they’re suing the LLC and not you individually. And so a question we get all the time is, well then, if I’m doing that and I have this rental income, should I make the LLC an S corporation?

And exactly what you just said about the act of passive. So if it’s passive income, you’re avoiding some of those, like the self -employment taxes or security of Medicare. For you to file as an S corp, you have to pay yourself a W2 salary for whatever you’re doing.

So let’s say you have $100 ,000 a year of rental income and you pay yourself 50 ,000 of the W2 salary, you’re paying all of those taxes. And then the pass through, the distribution, you would avoid Social Security Medicare.

So most of the time it doesn’t make any sense to have a real estate business as an S corp because you may be volunteering to pay more taxes if it’s passive income. So this would be a situation specific, but I would say generally avoid an S corp for real estate if it’s passive income.

And the LLC is really for asset protection purposes versus any kind of tax benefits. You can get the same tax benefits outside of an LLC that you could inside an LLC. Makes no difference. Well, James, before we move on to some more common pitches that clients get, one thing that we see all the time right now is real estate.

And the gets very popular, kind of blowing up. You could just scroll through social media and start investing in real estate through social media now. Before we go through that, let’s talk about the 1031 exchange.

I know I mentioned that. That’s a good way to avoid taxes. Not something I would do personally, because I don’t plan on real estate being a big part of my portfolio. And maybe I’m dumb because it’s going to be a great return.

I’m just saying for peace of mind, that’s where my decisions come from. But let’s say someone is planning on doing a lot of real estate, whether it’s residential or commercial, break down the wants to never pay taxes during their active year.

So they’ll go exchange to exchange. And they’re not ever realizing the capital gains during their working career. Let’s just talk about the rules of 1031 exchanges. I know there’s tight time frames that you need to work in to qualify.

So give us the rules. Yeah, basically you have a 45 day window where you have to identify the property. So if I sell a property, I have to identify where the money is going within 45 days. And obviously, if you’re buying a new property, you can’t close on it immediately.

So once it’s identified, then you have 100. From the day of the first sale, you have 180 days to then complete that. So if it’s outside of those two windows, then you lose the tax benefits. Got it. OK.

And there could be some timing issues, because typically you’re either buying high or buying low, or selling high, selling low. And so you’re not able to get 180 days. If the market’s great and it’s great to sell, you’re also buying high.

And six months is probably not going to be big enough, or 45 days especially. You have to negotiate. You’re probably selling high and also buying high. So that takes a lot of people with real estate, the wait for dips, the wait for market corrections.

And so the 1031 exchange in general, I’m going to say. is great tax strategy, but if someone is looking for deep discounts in real estate, that would take some of those strategies off the table. Yeah, timing is huge.

Timing is tight. Well, let’s get into these real estate syndicates. I think specifically with the type of clients we work with, like high income earners, they get pitched this stuff all the time because they obviously have the money to put into it.

Absolutely. I’m reviewing one literally today. Yeah. Probably one a week. But let’s put this into literally the simplest term. So this is how these work. If me and Matt want to go buy a big, let’s say we want to buy this huge luxury vacation property, it doesn’t matter.

One of us individually, let’s say we can’t afford it, we’re going to put our money together and we’re going to buy this property together in what they would call a syndicate. So it’s basically a group of people pull money together into this syndicate to buy some sort of property or construction build.

And then each person that puts money in has some sort of ownership or equity in that pool of money. So you get, you can take. Profit distributions if there’s profits we’ll get into that in a second But basically all the costs and profits are shared by the owners and then how these generally work is they’ll guarantee They’ll promise some sort of like income stream and then they’ll try to sell it for anywhere between you know two to ten x the return so if you put Very high -level or review let’s say you put a million dollars in to one of these syndicates and they say we’re gonna give you 7% per year rate of return so they’re gonna pay you 70 ,000 a year of income simple interest simple interest I just want to get my high horse real quick it drives me crazy because these syndicates I always quote Rate of return six seven eight percent.

I hear that all day. It’s simple interest. Yeah simple interest is not the eighth Wonder of the world its compounding interest is the eighth wonder of the world and so right off the bat You’re eliminating so much Appreciation that you could have versus it being compounded I do think that’s very misleading a lot of times the people pitching the syndicates Don’t know the difference of simple versus of compound interest when I ask that They’re not even gonna give me a straight answer and then I have to ask for the documents And then we find out it’s simple interest like 90% of the ones I reviewed are simple interest.

I just want to be really clear I’m off my high horse good So put a million in let’s say they give you 7 ,000 7% a year They’re paying you 70 ,000 and let’s say five years from now. They sell it for 2x you get 2 million back That you can use the depreciate depreciation can be used to offset that income And I would say when this makes sense is exactly the scenario you you said What to say we’re gonna put money in we’re gonna collect that tack can be tax -free income And then we’re gonna 1031 that into another Another real estate syndicate if you keep doing that and you want to make that an investment strategy can work Well, the caveat is though these get pitched to Almost everybody that we analyze these for they’re getting pitched by a friend somebody that they’re friends with is either Involved in it or their friends investing in it or a neighbor or a neighbor or whatever and I think just personally that’s a horrible reason to do it.

And maybe if it’s play money and it doesn’t impact your financial plan, go ahead. But if I were to ever invest in one of these, I have no interest in it, but it would be looking for somebody that the manager that has a very long track record of success in higher returns.

So there’s people that do this for a living and last 50 years if they’ve never lost money or lost very little of it, then great, maybe one to consider. But I would say generally speaking, people want to do this because they’re friends, they’re neighbors, whatever want to get into it.

And so they end up being a lot more complicated than most people think. So back to what we originally said, don’t invest in something you don’t understand. And then another thing to talk about on these is there’s general partner shares and limited partner shares.

The general partner is going to be making all the decisions. They’re doing all the day to day management. Generally, they’re paid first in the distributions. I’ve seen these work different ways. But the general partner They may not put in as much money.

Generally, the limited partners are funding it most cases. And then the general partners are going to get paid first. But they’re also taking on the liability. So if you’re a general partner, you have personal liability.

If something happens, your personal assets can get impacted. Whereas a limited partner, you have limited liability. You’re not making decisions. The return could not be as high. And generally, you’re putting in the capital.

So anything to add on that? No, that’s great. I see you have a simple versus compounding dress. Oh, yeah. Give me the break down. So that’s 7% per year on $1 million. Simple interest. Again, if you just took $70 ,000 per year for five years, $350 ,000.

If you took $1 million and compounded 7% per year, that’s $417 ,000 of interest. $67 ,000 over five years. But compounding interest goes. The longer. Yeah, we should do an example over 30 years. So I’m going to go through this.

Do you have that on the calculator? Let’s do one over 30. Because if someone’s doing, I mean, generally, if you’re doing real estate, which for all the clients we do encourage you to do real estate, it’s a long -term play.

If you want to be tax beneficial long -term and start building up this empire of passive income to supplement active income, the bigger the better. Because the more passive income you have, then the passive loss is offset.

So the best people, tax -wise with real estate, do a lot of it. And so once you’re in it, you’re in it for a long, long time. For it to be most beneficial, tax -wise. So with that being said, these syndicates are great from a time perspective.

Because you could just write a check for $100 ,000. You could write a check for $1 million, whatever it might be. And that’s it. But when you break down the deals, the fees are pretty high. Because generally, like Jameson said, the general partners, so you’re paying 1% to 5% right off the bat.

And then above that 7%, usually the general partners are taking about 30% of those profits on average above that 7%. Which is $1 million. is pretty significant because if you have a good year and you do 20 and you’re getting seven, that’s 13, and the manager is taking 30, that’s 3 .9% of a fee, plus let’s just say they’re charging 2% off the bat.

So that would be 5 .9% of a fee. And generally speaking, like stock market and real estate, you can get similar returns and most likely you can find a money manager that’s gonna charge you 1%. So the fees, the returns may be better with real estate, and they may be way worse in real estate, but in general with these syndicates, when you break down the fees and how they work on paper, it’s like, oh yeah, it guaranteed 7%.

Who would want to do that? Thanks for paying 2%. Well, the reality is you’re taking on a lot of, not liability risk, but risk with the real estate market, interest rates, et cetera, but you’re also paying, probably it’s the highest fee investment you’ll ever do in your life.

Yeah, for sure. All right, so did you figure out the yeah, so basically so let’s say you put a million in paid you 7% for 30 years 70 ,000 a year that’s 2 .1 million in interest I Would hope you got more than your principal back, but let’s just say after 30 years you did get your million back So that’s 3 .1 million is the end result Whereas if that’s 7% compounded for 30 years a million dollars compound at 7% that’s 8 .1 million So it’s a five million dollar difference.

Yeah, someone’s saying in the fine print You’re getting guaranteed 7% and you know to ask the right question is that simple compound that one word Simple versus compounded on your million dollars just cost you five million dollars over a 30 year time frame Let’s even give real estate benefit that let’s say that’s all tax -free with depreciation and Probably unlikely that it is but it’s all tax -free and let’s just say even if there’s a capital gains change to we’ll say 39 .6 We’ll say 40% That ends up being basically even after taxes.

They’re still gonna make out so 7 .1 million times 25% Okay, so 1 .7 to call it 2 million is going to taxes you’re still netting six So the simple interest you’re getting three in the compounded interest even if they’re taxed at the end You’re still netting double that so okay.

I thought that was really important that to point out so recently There’s some that’s become pretty popular called these qualified opportunity zones And in general, this is a tax play James I know you with a client just went into super detail with one.

Can you break down? What is this? Is it something you’d recommend is a case -by -case basis and what should someone look for if they’re getting pitched or you know Want to avoid taxes and going in a qualified opportunity zone.

It was the details total case -by -case This was put in place with the trump tax cuts that made this available Basically what it is it’s a similar set up as the real estate syndicate that we just explained but there can’t can be tax benefits.

So it’s basically the government saying, we’re going to designate these zones that encourage development and investment into these specific areas. So the tax benefit is you can fund it with an appreciated asset.

So let’s just say you have a stock that has a basis of $100 ,000 or anything that’s appreciated. And let’s say you have huge appreciation on it to $1 million. If you were to sell that, you’d pay capital gains taxes on that $900 ,000 of gains.

What you can do with these is you can take that money. You still have to sell it that year. So you make, let’s say 2023, we sell that asset. We have a $900 ,000 gain. We don’t report it this year. So we don’t pay taxes.

We defer that until 2026. However, we’re able to put this $1 million into the real estate syndicate, the qualified opportunity zone. And that now is my basis on that investment. 2026 comes, we report that gain.

We pay the taxes. You still pay tax on the 900. Still pay tax on the 900 in that year. So the risk is, what if capital gains taxes go up? However, this million dollars that’s now the basis appreciates.

And if you hold it for 10 years, that’s all tax -free. So if it appreciates to 10 million, in after 10 years, you don’t pay any taxes on that. Got it. So it can be tax beneficial. I would say it’s totally case by case specific.

But the way they pitch these is that it’s a huge, huge, huge tax benefit. And when you really lift the hood up, you’d have to have a huge appreciated asset that would make sense to do that, which could, I mean, that’s not realistic that somebody gets the $900 ,000 gain like that generally could happen.

And so these qualified zones, it’s not just anything. You can’t just go invest in a hot area. It’s usually a not good area right there. Underdeveloped or, yeah, where they’re trying to. High risk, underdeveloped, that they’re trying to boost the economy up.

So there’s a reason the government’s allowing you to avoid taxes so they can redistribute wealth and help other areas of need. And I think that’s an important thing to do. Understand what you’re. Yeah, but understand not to do the qualified opportunity zone to help out areas of need.

But also with your own personal financial plan, you know, don’t let the taxes lead. Make sure your goals, your financial plan, your risk profile lead, and then make the decisions based upon that. And be as tax -evident as you can.

But if all you care about is taxes, you know, you may end up with $0 in your tire. Yeah, yeah, one bad deal could ruin you. I’d say one other thing that you can do with that. So there’s obviously, these are usually high fees, just like any other real estate syndicate.

You can open your own LLC and then you can designate it as a qualified opportunities zone. And you could get a real estate syndicate to let’s say you’re investing where you use Pittsburgh, for example, it’s a qualified opportunity zone, they’re doing a build in Pittsburgh, let’s say, and you could go through one of these syndicates to invest in that, or you could open your own LLC, classify it as a qualified opportunity zone, you have to have enough money that they would accept it, whatever their minimum is, and you could go to that project and say, I’m going to invest in this through my own qualified opportunity zone, or me and you could pull our money together and create our own, and then you pay annual legal fees, which I analyzed this for the one deal was far less than what the syndicate was offered.

Management fees were. Yeah, and so then you could literally just create this yourself and cut the middleman out, so probably a very rare case we’d recommend that, but that would be an easier way to get into one of these.

Okay, awesome. Well, Jameson, to close up here, thanks for sharing, those I think are going to be more and more popular from pitching because of the people that organize those are going to be able to charge a high fee and pitch it with all the tax savings.

So if you’re high income earner and have high capital gains, you’re probably going to be a huge target to get these things pitched to you. So let’s close up with this. So I know to prepare for this podcast, you asked one of our most successful clients that did a ton of real estate investing that we actually hope to interview on the podcast soon.

You asked him for advice, because he had invested in one of the hot pockets of Pittsburgh and done very well with a partner, him and a partner. And you asked him, you know, what advice would you give to someone like a young doctor, a young person, or someone older that’s retired, anyone investing in real estate, what advice?

So let’s just go, I know you have these listed out, let’s go back and forth here. So what’s the first piece of advice that you heard? He said, there’s a lot of unexpected costs. So make sure that you have liquidity available.

You have a cash reserve built up or an available line of credit that you’re comfortable using. There’s always gonna be costs that you do not anticipate, whether it’s, you know, fixing something in a property or who knows.

And because of that is number two, be prepared for negative cash flow initially. It may be pitched, so you put in a million dollars and boom, it’s like, oh, there’s this great rate of return. You’re getting seven or eight percent back on your mind.

Well, you may, when the tenants flip, you may have to fix a bunch of stuff. You may have to, so just prepare it initially. It’s not always a positive cash flow, sometimes a negative cash flow. So make sure your base, your active universe of income is really strong in order to support any needs that your real estate baby has.

Yeah. Third one is learn as much as you can before entering, especially if you’re not a real estate perfection. I think that’s true with, again, I’ve said this three times on this podcast. Anywhere you put your money, make sure you understand it.

Don’t just go in blind. Research, ask people that have done it, ask people that are in the business to make sure you get as much knowledge as you possibly can before making the investment. Absolutely.

Next one, start small. I completely agree with this. It’s see if you like it. See if it likes you. See if you like it, it likes you. If you’re doing the partner, start small, have an easy exit plan, or if you do like it, then go all in on it.

Yeah. And don’t buy 10 properties at one. Start with one, maybe two, and yeah, exactly what you said. The next one, have a trusted network of people to use. So this is important. Contractors, landscaping, whether using a property manager or not, but people that you know, that you trust and so if you have a property and you have to, and the tenant has the, I don’t know, say the garage door breaks, if you don’t want to go out there on Saturday night to fix the garage door, have a contractor or somebody that you can just send to fix it that you trust.

So have that network developed that you can call in. Awesome. Have a trusted financial advisor, CPA, attorney that’s able to give you good unbiased advice. Yep, I think that’s really important and he actually specifically said a lot of, he had worked with a bunch of advisors in the past before he started working with us and he said a lot of them genuinely didn’t understand how real estate works.

So having somebody has experience doing that is really important. Absolutely. Be careful buying properties that have existing tenants in them. He said always make sure you screen them, whether you have by a property that’s vacant and then you’re getting a tenant in there, screen them, make sure that they’re not going to give you.

State by state specific, but typically laws work really in favor of tenants and not not fairly landlords. So you didn’t make sure that you screen them. That’s great. And then the last one is make sure you have appropriate insurance coverage.

You know, stuff can go wrong and you don’t want to have to dig into your other universe of wealth and income to constantly support this. So, well, James, thanks for joining me and going into so much details.

We welcome any questions anyone has on real estate and look forward to helping our existing and new clients in the future on all of their real estate endeavors. We have seen real estate be an amazing investment opportunity for a lot of people.

A lot of people are passionate about it. We’ve also seen the mistakes and sometimes people realize they’re absolutely not interested in doing real estate. You know, what they thought it was, it turns out it wasn’t at all from a tax or a return perspective or peace of mind perspective.

So really case by case basis. And we encourage you, you know, talk to people that have experience doing this, talk to a trusted advisor, and make sure you put a lot of intention before making any quick decisions.

Absolutely. Thanks for tuning in to our podcast. Hopefully you found this helpful. Really hope this is as beneficial and impactful to as many people across the nation as possible. So hit the follow button.

Make sure to rate the podcast and please share with any friends or family members that would also find this beneficial. Thank you very much.