Hello, Matt with EWA. Chris with EWA. Today we’re talking about the hierarchy or the order of importance of where to save and why from a tax efficiency standpoint. So, Chris, walk us through where do you put money first and then how do you decide to start opening up new buckets and give us the tax reasons behind that?

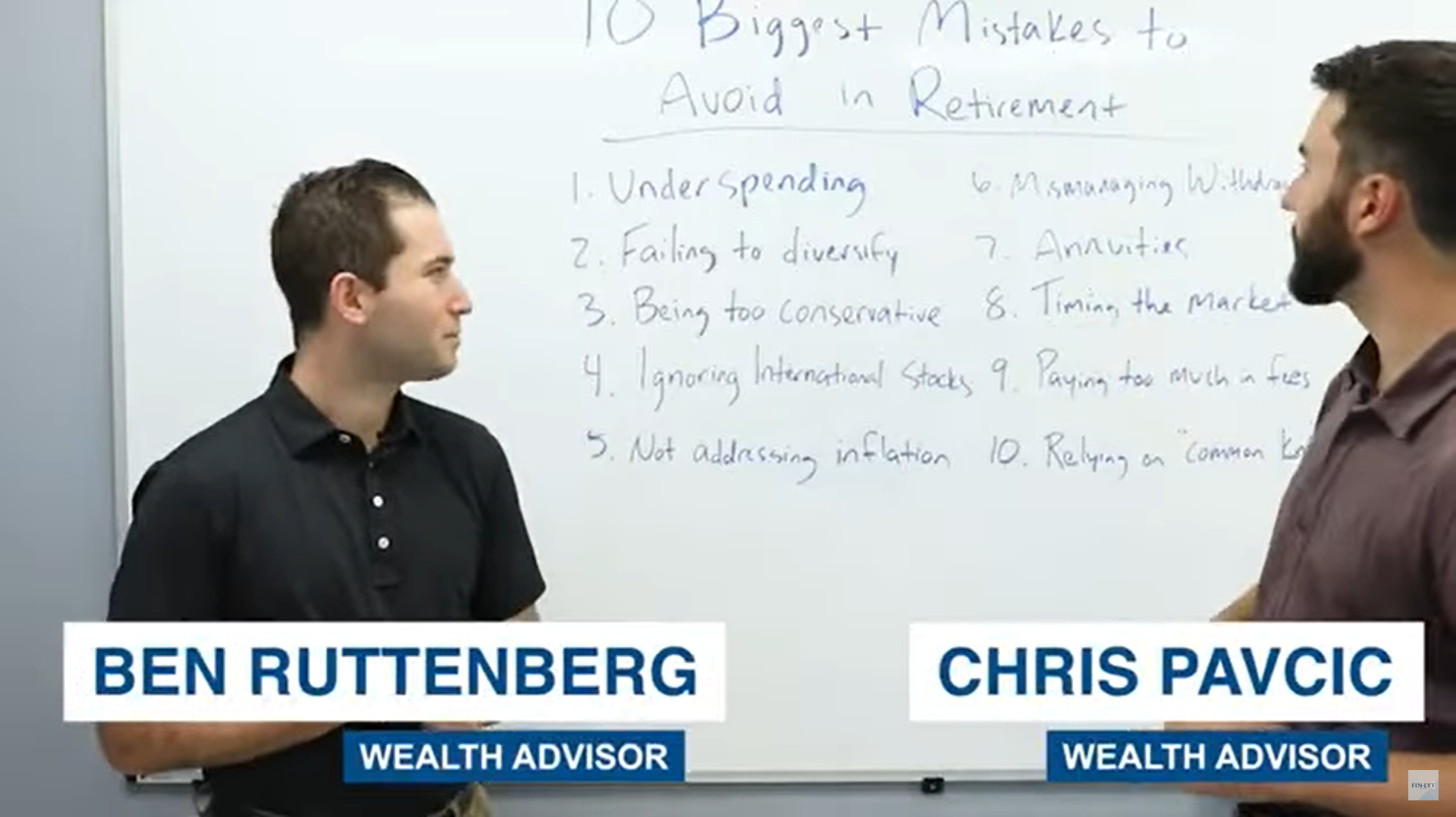

Yeah, absolutely. So what what we have on the screen here is just a hierarchy of where we want to start when we’re looking to save money. First rule of thumb is we want to make sure we have an emergency fund.

Established rule of thumb is between three to six months of expenses readily available at any time. This doesn’t only have to be in cash. For example, if you’re funding a Roth IRA, you can take out the basis at any time, meaning what you contributed into the account, you can always take that out tax and penalty free.

Or if you have a brokerage account that’s flexible and liquid, we would also consider part of that as an emergency fund as well. Next would be making sure that we have our basic insurances in place life insurance, disability insurance to protect against worst case scenarios.

And then once these two are satisfied, we start moving into tax favorite accounts. So next you’ll see health savings account. That is the only type of account that is triple tax free. So the money on the way in, you get a tax deduction, it grows tax free.

And if you use it for qualified health care expenses, the distribution is also tax free. Then we start to move into 401K planning and IRA planning. General rule of thumb for a 401K is always at all times, if your employer offers a match, make sure that you’re contributing up to that match so that you’re not leaving any free money on the table.

And then beyond that, before. Going above that match maxing out IRA accounts. Specifically, we’re big fans of Roth IRA planning and then moving on up to work towards getting the maximum amount inside of the 401K plan, which is currently 20,500 per year.

After 401 KS and Roth IRAs are maxed out, some plans allow you to contribute above them the $20,500 limit and complete what’s known as the mega backdoor Roth 401K strategy. We filmed a completely separate video on this, and we included a link below for you to access if that’s something that you’re interested in.

And then after all these accounts, after we check all of these boxes, next step would be starting to look into some insurance planning, specifically with cash value life insurance, to start building up a safe bucket that is not correlated to the stock market that you can use to eventually supplement portfolio withdrawals during retirement.

And then lastly, moving into just funding a flexible brokerage account that you can use at any time for any reason, whether it’s for college planning, retirement planning, et cetera. Excited to chat through this next time we meet.

If you have any questions in the meantime, please feel free to reach out.