Many physicians today are building wealth not just by practicing medicine, but by leveraging their expertise through consulting, public speaking, expert witness work, medical writing, or moonlighting. These ventures often generate 1099 income, which may provide opportunities for tax strategies, retirement savings opportunities, and long-term wealth building when properly structured with guidance from qualified tax and financial advisors.

Below, we explore how to maximize deductions, set up the right retirement accounts, and manage this income stream like a business.

When physicians earn 1099 income, whether from consulting, expert witness work, speaking engagements, or moonlighting, it’s treated as self-employment income. Unlike W‑2 wages, this income is reported on Form 1099‑NEC, and you’re responsible for both income tax and self-employment tax on it.

Self-employment tax covers the full amount of Social Security and Medicare taxes, a combined 15.3%, made up of:

As a W‑2 employee, you typically pay only half of this (with your employer covering the rest). But as an independent contractor, you’re responsible for both the employee and employer share.

There’s a cap on how much of your income is subject to the Social Security portion of payroll tax. In 2025, the Social Security wage base is $176,100. This means:

If your W‑2 salary already exceeds $176,100, you will not owe additional Social Security tax on your 1099 income. You will still owe the full 2.9% Medicare tax on all 1099 income, and possibly the 0.9% surtax if your total earnings exceed the threshold.

If you have multiple employers or income streams, and overpaid Social Security tax, the IRS may refund the excess when you file your return.

| Scenario | Social Security (12.4%) | Medicare (2.9%) | Additional Medicare Surtax |

|---|---|---|---|

| Self-Employment up to $176,100 | Applies until cap reached | Applies to full 1099 income | 0.9% if income exceeds threshold |

| Already reached $176,100 via W-2 | No further Social Security tax on 1099 income | Still owe Medicare on all 1099 income | Same rules apply |

Understanding these payroll tax rules is critical for physicians earning 1099 income. Many high-income doctors will find that:

Next, we’ll explore how to reduce taxable income through business deductions and how physicians with 1099 income can potentially contribute up to $70,000 (2025 IRS Limit) per year toward retirement using advanced tax strategies, including the Mega Backdoor Roth.

Here are common deductions that may apply, depending on the nature of the side work:

| Deduction Category | Examples |

|---|---|

| Home Office | A dedicated space used exclusively and regularly for the business. |

| Professional Fees | Medical licenses, board certifications, subscriptions (e.g., UpToDate, Doximity Pro). |

| Continuing Education | Courses, webinars, and certifications relevant to your consulting or clinical expertise. |

| Travel & Lodging | Travel to speaking engagements, medical conferences, or consulting gigs. |

| Equipment & Software | Computers, microphones, projectors, medical tools, or business-related apps. |

| Marketing | Website, personal brand development, business cards, digital ads. |

| Legal & Accounting Fees | Tax prep, entity formation, contract review. |

| Health Insurance Premiums | If you’re not covered elsewhere, premiums may be deductible. |

Pro Tip: Use a separate business checking account and credit card to simplify tracking. Tools like QuickBooks Self-Employed or Keeper Tax can automate deduction tracking.

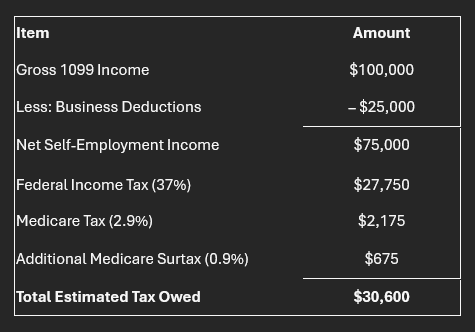

To illustrate potential tax considerations, here’s a hypothetical example. This assumes an individual is in the 37% federal tax bracket from W-2 income and has reached the Social Security wage base. Individual circumstances will vary, and you should consult with a qualified tax advisor regarding your specific situation.

Let’s say you earn $100,000 in gross 1099 income and claim $25,000 in business deductions:

Business deductions saved $9,250 in federal tax alone (37% × $25,000).

State Tax Reminder: Depending on your state of residence, you may also owe state income tax on this income. Some states (like California, New York, or New Jersey) have top marginal rates exceeding 10%, while others (like Texas or Florida) have no income tax at all.

For high-income physicians with 1099 income, one of the most powerful and often overlooked wealth-building strategies is the Mega Backdoor Roth. If you have self-employment income, you may be eligible to open a Solo 401(k) and structure it specifically to support this strategy. For 2025, this could allow eligible individuals to fund up to $70,000 into a retirement plan (subject to IRS rules and limitations) with potential for Roth conversion, though specific amounts depend on individual circumstances.

A Solo 401(k) plan can be designed to include:

The key advantage? The after-tax contributions are not subject to the 402(g) elective deferral limit of $23,500 per person (or $31,000 for those 50+ in 2025). Instead, they’re governed by the 415(c) limit, which sets the total maximum contribution to a qualified plan in 2025 at $70,000 per person, per plan (or $76,500 with catch-up contributions if age 50+)

This means if you’ve already maxed out your 401(k) elective deferrals through your W 2 job, you can’t contribute any more elective deferrals to your Solo 401(k). However, you can still make after-tax contributions to the Solo 401(k) up to the full $70,000 limit, funded dollar-for-dollar from your 1099 income, assuming sufficient net earnings.

Here’s how to implement the Mega Backdoor Roth using a Solo 401(k):

But here’s where it really matters: Many physicians build substantial pre-tax retirement savings during their working years through 401(k)s, 403(b)s, and SEP IRAs. While these offer upfront tax deductions, they also come with Required Minimum Distributions (RMDs) in retirement, which force taxable withdrawals starting in your early 70s.

Future tax rates may change based on various factors. While some financial experts suggest rates could increase, future tax policy cannot be predicted with certainty. It’s important to consider both current and potential future tax implications in your planning.

Even in retirement, you could find yourself in a higher tax bracket than expected, especially when layering in RMDs, Social Security income, investment gains, and potentially fewer deductions.

Roth strategies may be worth considering as part of a comprehensive tax planning approach. The Mega Backdoor Roth, when appropriate for your situation and properly implemented with professional guidance, may provide tax advantages including potential tax-free qualified withdrawals. Consult with qualified tax and financial advisors to determine if this strategy aligns with your specific circumstances.

Most physicians overlook the planning opportunities tied to their 1099 income. But with the right guidance, these earnings can become a launchpad for strategic tax savings, aggressive retirement funding, and permanent Roth wealth. The key is structuring your plan intentionally, from business deductions to Solo 401(k) design, and executing it with precision.

For assistance with planning and managing your side income, or assistance with any of our other services, contact Equilibrium Wealth Advisors today at (412) 991-1385!