Please select a default template!

One of the most impactful decisions an individual or family can make is creating a written financial plan. But ultimately, even the most fundamentally sound financial plans can be thrown off by one mistake. Steering clear of these five mishaps will help ensure you stay on track.

1. Investing Money Into Equities That You’ll Need In The Short-Term

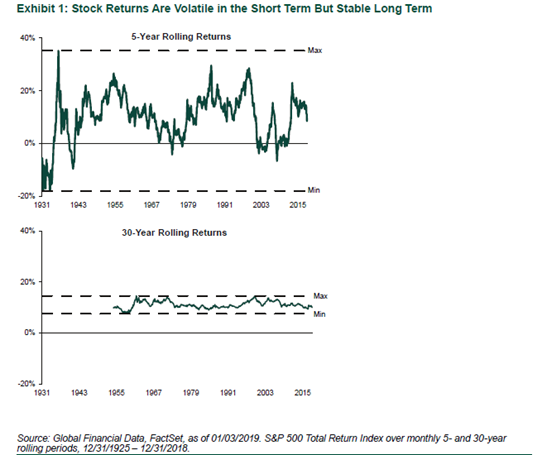

A common mistake investors can make is leaving money invested in equity markets when the time horizon for using said funds is short. Whether it be saving for a child’s upcoming education or approaching a desired retirement age, keeping the time horizon front-of-mind for funds that are invested is of paramount importance. The below exhibit shows 5-Year Rolling Returns of the S&P 500 Index compared with 30-Year Rolling Returns of the S&P 500 index between the years 1931-2015. Five year rolling returns from this time period have shown to be volatile. There were certain five year windows within that timeframe in which an investor would have experienced a loss in their investment. However, if we extrapolate out to a thirty-year window, there was no thirty-year timeframe between 1931-2015 where that same investor would have experienced a loss in the S&P 500 index.

Ultimately, a general rule of thumb is to keep money you plan on using in the next five years outside of the equity markets. Ensuring that your investment allocations match the time horizons for each of your financial goals can help keep your financial plan on a better track.

On the flip side, all money outside of 5 year timeframe, we recommend to invest in equities once you have your short term horizon planned for appropriately.

2. Letting Emotions Dictate Investment Decisions

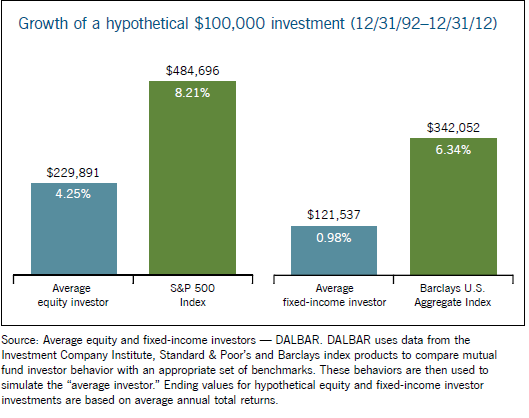

One of the keys to a sustained, long-term investment strategy is to be an unemotional investor. Whether it is easy to admit or not, oftentimes emotions outweigh logic when making investment decisions. The below graphic shows the growth of a hypothetical $100,000 investment from December of 1992 to December of 2012, in the S&P 500 Index and Barclays Index. Had an investor just kept their $100,000 in the S&P 500 for the twenty year period, reinvested dividends, and didn’t take any withdrawals, the investor would have received an 8.21% return. However, the average investor in the equity markets over that same time period only averaged 4.25% due to pulling in and out of the market because of news and ultimately fear that caused emotional decision making. Investing with too much emotion can lead to pulling money out of the equity markets when they are down (when it feels good to be on the sidelines) and putting money back into the equity markets when they rise.

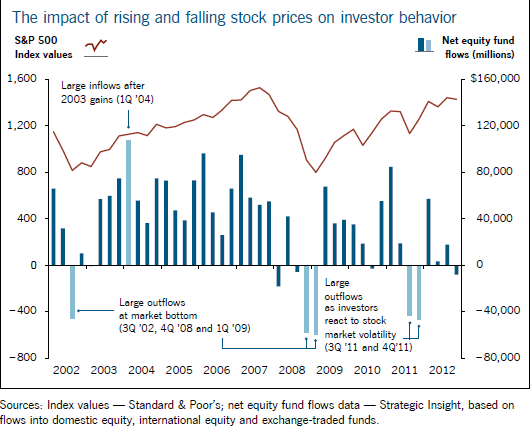

Further extrapolating, the below graph displays when large inflows and outflows from the stock market occurred between the years 2002 – 2012.

As shown, large outflows (the light blue line downward) occurred in 2008 and early 2009, as investors reacted to severe volatility. Large inflows (the dark blue line upwards) then occurred after market recovery in late 2009 and 2010.

Avoiding emotional decisions and sticking with your financial plan through short-term volatility can pay huge dividends towards achieving your financial goals.

3. Being Too Concentrated In One Investment or Sector

Having “too many eggs in one basket” with regard to your investment strategy can be a detriment to a sound financial plan. This is particularly relevant for highly compensated executives who hold company stock. Generally speaking, we advise keeping a position under 10% of your overall balance sheet. In certain scenarios, between 401k balances and large company stock positions, an executive could have upwards of 50% of their net worth tied to one company’s performance, not even including the company providing them their salary and potential benefits. If the company suffers distress, this could put a strain on the executive’s financial plan.

This idea doesn’t just apply to executives. Many investors will hold onto a position that is overweight for sentimental or emotional reasons. As stated previously, letting emotions dictate investment decisions can have consequences. Ultimately, keeping an asset allocated, diversified portfolio paired with unemotional behavior is generally advisable.

Here is a story of an EWA client who saved millions by following this exact advice.

4. Not Adjusting To Your “Money Temperature”

Without even realizing it, it is very easy to seemingly adjust to an increased income by increasing expenses and not adjusting to your “money temperature”. What is also referred to as “lifestyle creep,” this is the idea of former luxuries becoming new necessities to correspond with a rising discretionary income.

If this is not planned for in a deliberate manner, one can feel like they are living paycheck to paycheck despite earning more income. The best way to adjust to an increased money temperature is to develop the correct system for saving and spending on a monthly basis. Employing a “reverse budgeting” system aims to divide expenses on a monthly basis into a fixed category and a variable category. If fixed expenses (debt payments, bills, savings) are on autopilot and paid each month, the remaining pay can be sent to the “variable category,” and is meant to be spent down to $0 guilt-free each month. With these guardrails in place, one is much better able to adjust to their money temperature and ensure a better path towards financial success.

5. Not Having A Drafted Estate Plan

According to a Caring.com survey, only one-third of Americans have a documented estate plan in place. While some may believe estate planning is only for the ultra-high net worth, every family can benefit from having even basic estate planning documents in place, namely wills and powers of attorney. Wills help dictate what happens to your assets when you pass (if they do not have direct beneficiaries already attached), and powers of attorney allow you to choose who will make medical and financial decisions on your behalf if you are incapacitated. If these documents aren’t in place, the courts will decide how your assets are split (if beneficiaries are not already named directly), which may or may not fall in line with your ultimate wishes. If assets are further subject to probate, then this process of settling the estate is technically public record and can be accessed by anyone. Furthermore, if a situation involves trust planning, be it revocable, irrevocable, or special needs, then further discussion to ensure proper settling of assets will be required.

No investment strategy is completely bulletproof, but avoiding these five mistakes can help lead to a sustained, long-term financial plan. If you have questions about any of the above topics, please consult with a financial advisor and / or estate planning attorney.