Please select a default template!

The standing room temperature of a household is frequently a point of contention. However, whether you prefer the temperature on the cooler side or warmer side, once a number is set on the thermostat, you’ll soon adjust to that specific temperature in the room.

Budgeting on a monthly basis is a very similar analogy. If there is not a set system in place, it is very easy to seemingly adjust to your monthly income and lose track as to how much is saved versus spent each month. Because of this phenomenon, one of the most important steps one can take towards owning their finances is creating a proper budget. However, those that meticulously track expenses and worry about how much they spend, often stay behind without a set budgeting system in place.

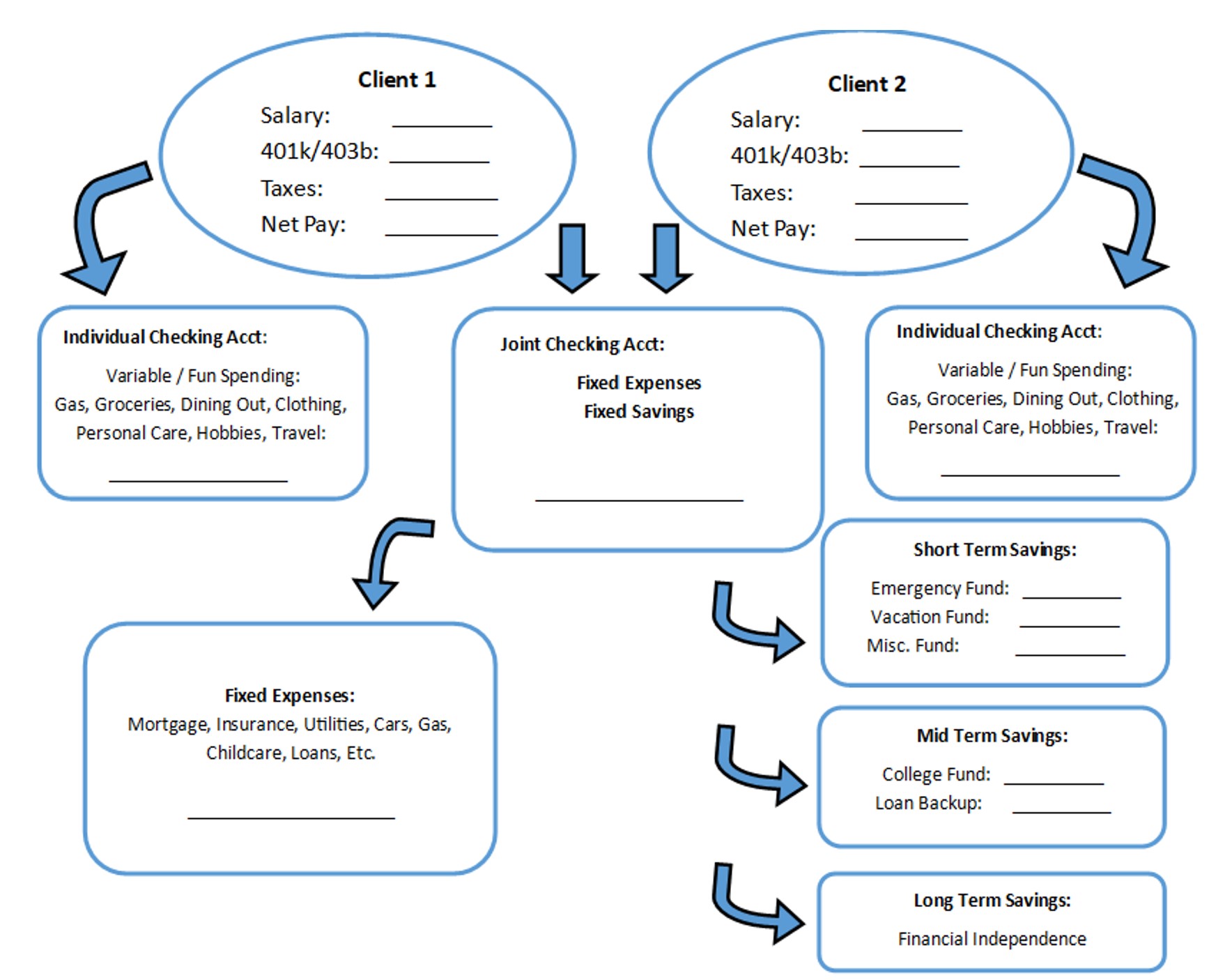

While there are many ways one can budget, one system that we have found to be most productive is the concept of “reverse budgeting.” In the simplest terms, reverse budgeting breaks down your monthly income into two buckets: one being fixed expenses and the other variable expenses, and then automating and prioritizing savings (just like you must pay your mortgage, you must pay yourself, “save,” if you want to get ahead).

Fixed expenses are payments that need to be satisfied on a monthly basis. Examples of fixed expenses include mortgage payments, insurance premiums, utilities, student loan payments, etc. For this exercise, monthly savings are also included in the “fixed bucket.” Examples of this can include: 529 plan contributions, investment account contributions, Roth IRA contributions, etc.

Variable expenses are not fixed and can be different every month. Some examples of variable expenses include groceries, travel, dining out, and other discretionary spending.

The idea behind reverse budgeting is to have a portion of your income that fully satisfies the “fixed bucket” sent to a separate bank account (and set all bills and all savings on autopay). This is the key part to reduce decision fatigue. If this is not automated, we have seen the snooze button hit too many times for clients that intend to save but have not accomplished it. Feelings, moods, and short-term thinking can hijack the long-term plan.

The remaining portion of your income can be sent to your “variable bucket” bank account and can be spent down to $0 every month, knowing everything is satisfied from the fixed side of things.

For example, let’s assume a household earns a net monthly income (after taxes and 401k contributions) of $10,000. Furthermore, this household’s fixed expenses (including savings) are $7,000 and variable expenses are $3,000.

If properly implementing the reverse budgeting strategy, this household would have $7,000 of their monthly pay deposited into a bank account set strictly for fixed expenses. This satisfies all monthly savings and obligations, and essentially puts them on “auto-pilot” moving forward. The remaining $3,000 of pay would then be deposited into a second bank account. This allows this household to guilt-free spend down that $3,000 every month, knowing full well that they have already “paid themselves” and that their account will be replenished by their next pay.

We have found successfully implementing the reverse budgeting strategy helps eliminate “decision fatigue” and allows for easier spending decisions (knowing that all necessary obligations are on autopilot). While there are other budgeting systems that suffice, the reverse budgeting system doesn’t require tracking every expense on an Excel spreadsheet. Reverse budgeting allows efficiency and simplicity for an important aspect of your financial planning.

A proper budgeting system can help set you on the right path to spending within your means and working towards your financial goals.

__________________________________________________________________________________

Equilibrium Wealth Advisors is a registered investment advisor. The contents of this article are for educational purposes only and do not represent investment advice.

Stock markets are volatile, and the prices of equity securities fluctuate based on changes in a company’s financial condition and overall market and economic conditions. Although common stocks have historically generated higher average total returns than fixed-income securities over the long-term, common stocks also have experienced significantly more volatility in those returns and, in certain periods, have significantly underperformed relative to fixed-income securities. An adverse event, such as an unfavorable earnings report, may depress the value of a particular common stock held by the Fund. A common stock may also decline due to factors which affect a particular industry or industries, such as labor shortages or increased production costs and competitive conditions within an industry. For dividend-paying stocks, dividends are not guaranteed and may decrease without notice.

Past performance is no guarantee of future results. The change in investment value reflects the appreciation or depreciation due to price changes, plus any distributions and income earned during the report period, less any transaction costs, sales charges, or fees. Gain/loss and holding period information may not reflect adjustments required for tax reporting purposes. You should verify such information when calculating reportable gain or loss.

This content has been prepared for general information purposes only and is intended to provide a summary of the subject matter covered. It does not purport to be comprehensive or to give advice. The views expressed are the views of the writer at the time of issue and may change over time. This is not an offer document, and does not constitute an offer, invitation, investment advice or inducement to distribute or purchase securities, shares, units or other interests or to enter into an investment agreement. No person should rely on the content and/or act on the basis of any matter contained in this document. The tax and estate planning information provided is general in nature. It is provided for informational purposes only and should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.