If you have read a lot of the financial and market headlines, many people are asking are we in a recession right now? Is the economy trending into a recession? So we want to talk about what actually indicates a recession, what a recession means, and look back at some past recessions and give you this should give you some peace of mind that your financial plan should not be in jeopardy even if we are trending into a recession.

So with the recession, it is hard to tell if we are in a recession generally until we are actually past a recession. So overall, recession is a general decrease in GDP, a country’s GDP for more than two quarters.

But there are a lot of different factors that tie into this. Many people think that a recession is the only indicator of a recession, is a decrease in stock prices. But that is a misconception. There are a lot of things that factor into it.

So stock prices, the unemployment rate, manufacturing, inflation, supply chain and many different economic indicators that lead to a recession. So let’s look back at the last bear market that we saw, march of 2020.

We saw a 34% decrease in US equity markets from the COVID-19 Pandemic. And that was not long enough to be considered a recession. That was just a market pullback, a short bear market and we saw double digit recoveries within the next couple of months.

Following March of 2020, average bear market lasts about ten months. Sometimes that leads to a recession, sometimes it does. So characteristics of recession, this will be things like a decrease in GDP for at least two quarters.

Consumer confidence is down, they’re less likely to make major purchases. Unemployment spikes and companies begin massive layoffs reduced consumer activity which forces business to scale down in production inflation leads to decreasing in purchasing power of the US dollar which leads to consumers purchasing and buying less things but what is an actual economic indicator that would come into play to dictate that we are actually in a recession?

So the first thing would be, again, decline in GDP. The second would be a rise in the unemployment rate. Third would be low consumer confidence. Fourth would be stagflation in manufacturing and sales.

The CPI index, which is the consumer price index that tracks inflation, which ultimately just leads to a rise in inflation. So we look at causes of a recession. The first one would be when supply cannot keep up with demand.

Example this was 2008 with the housing market. The supply could not keep up with the demand for houses, which then led to the second cause, which would be an asset bubble. Asset bubbles bursting. So the housing bubble or the.com bubble in the early 2000s are examples of this.

And another cause of not a recession but a bear market would just be economic shock or a black swan event. So 911 COVID-19 those were examples that led to a bear market, not necessarily led into an economic recession.

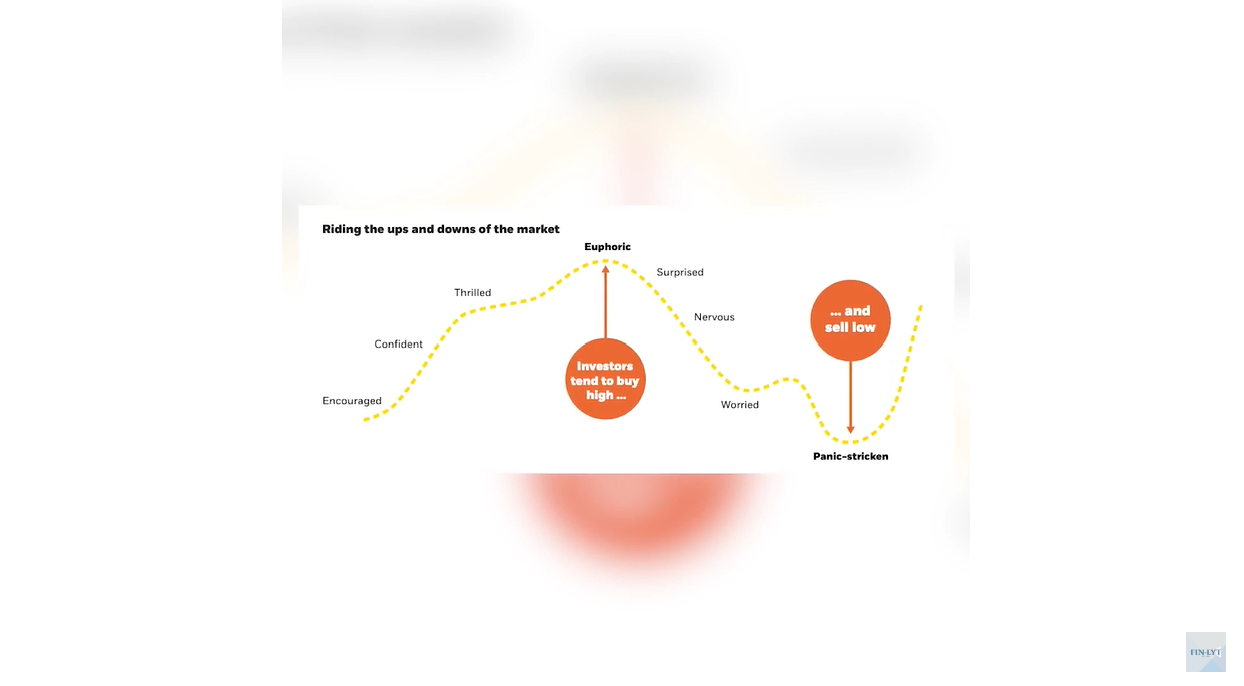

Investing can generally be a very emotional thing and when you rely on emotions and not logic or investment principles or sound financial planning, that can generally be costly to your returns of your portfolio.

So when times get tough, human nature is that you get fear of missing out and you want to limit your losses. This so things you see your portfolio drop, you want to sell to limit any downside. When fear and emotion comes in, investors tend to do the opposite of what you should.

This would be they tend to buy high and sell low. So if we look at this graph here, this just shows. As the economic cycle progresses, the emotion that comes along with the market. So you can see here at the top, there’s a euphoric emotion when the market is at an all time high.

Generally as a consumer, you want to buy more. When panic sets in, it’s at a low. You generally want to limit your losses and begin to sell, which is the opposite of what we actually want to do as an investor.

Many investors like to mitigate their losses and sell when markets hit an all time low. But looking at historic averages, there generally tends to be a very rapid increase in rate of return in equity markets following a bear market or a 20% decline.

So this chart is going to look at the worst days, months and three month periods of the S and P 500 since 1950. So if we look over here on the right side, we’ll look at two examples. One would be January of 2020.

To March of 2020, the S and P 500 decreased 19.6% but one year later. So one year after that, the rate of return from that dip was 56.4%. And then the last recession that we saw. So from December of 2008 to February of 2009, over that three month period, the S and P 500 was down 17.3%, and one year later, we saw an increase of 53.6%.

Winter is always followed by spring, meaning that a bear market is always going to be followed by a bull market. Looking back at history, there’s always double digit returns following negative days in the stock market.

So you should have fail safes in place in your financial plan that you have safe assets to pull from to get through any down market. So you don’t have to sell any equities at a loss.