Matt shares valuable insights on financial returns, debunking common myths and emphasizing the importance of a long-term perspective. Exploring topics like compound interest, risk, and the sequence of return risk, he guides listeners to navigate the intricate world of investments. Matt’s lessons extend to real estate, urging individuals to view their homes as lifestyle choices rather than mere financial investments. With a focus on fundamentals and a disregard for short-term market fluctuations, Matt encourages a holistic approach to financial planning, empowering individuals to embrace a lifelong journey towards financial independence.

Several things about returns that I’ve learned are really surprising to most and a lot of lessons I’ve learned along the way. So the first one is going to be, you know, simple versus compounded interest. So the 7th wonder of the world, as Einstein, you know, 8th wonder of the world, as Einstein said, is compound interest is not simple interest. So let’s just use an example where you have a million dollar investment and the simple interest gets 10% a year for 30 years. So that simple math, 10% of a million is 100 a year times 30, that’s 3 million plus the original 1 million. So the total that you would have is $4 million. Well, if you take that same million dollars and you apply half of the return, but compound it over the 30 years, you’re going to have over 4.4 million.

Again, half the return, but compounded versus simple, not only do you get the same result, you get more result by 400,000 over the same 30 years. And really, there’s so many short term fads, there’s so many. Let’s two XR money, let’s three XR money in a short period. That’s really irrelevant because where you want to get your money is in a long term environment where it’s supporting your life by design. And ultimately, in a compounded environment, if we just apply the same math, where we have a million dollars that gets the same 10%, but we compound it instead of simple, the ending balance is a little over 19.8 million. So almost five times the result before. And this is actually, I just did it, 4.46 million plus, to be exact.

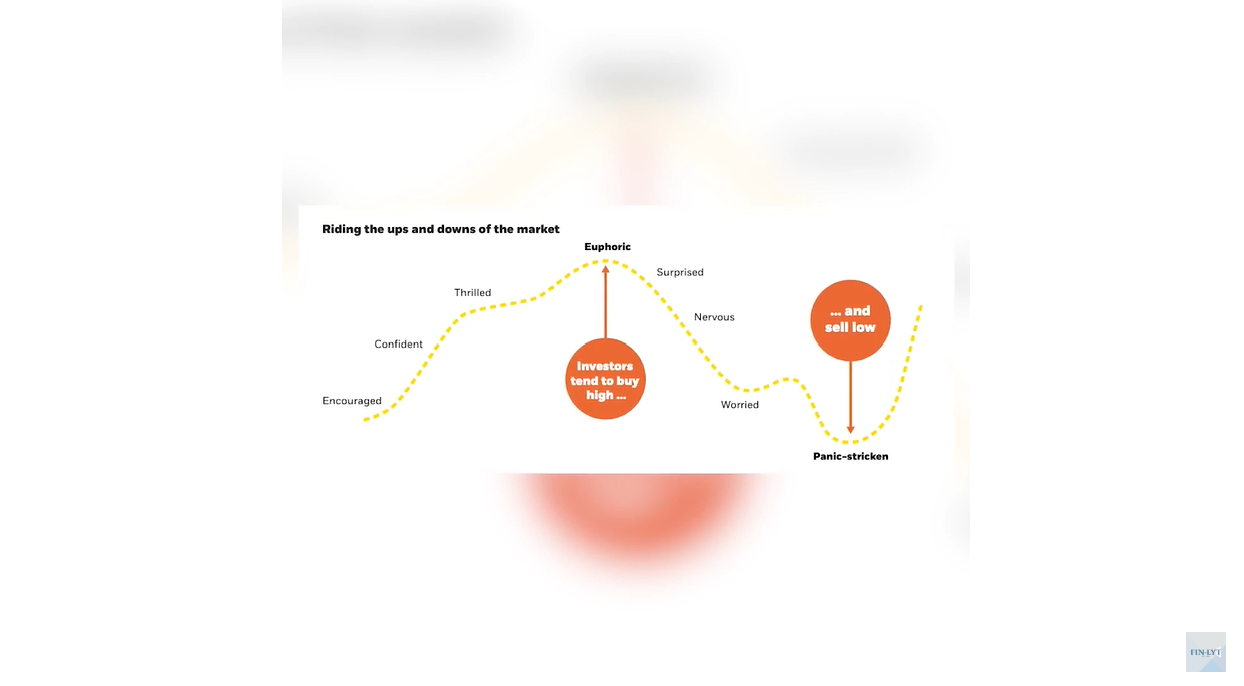

So that’s the first rule of thumb, is not necessarily looking for big returns in the short term. It’s where can I get my money to work long term? In an environment where it compounds interest, earns interest on the interest, and every year that continues to go. So the second thing is the paradox between risk and return. And this ultimately gets marketed out there where be risky when you’re younger and be safe when you’re older. I think this should be the opposite. Here’s why. A big return when you have a little amount of money doesn’t result in really anything but a decent return when you ultimately have a couple of million dollars. The return of that one year could be more than all of the returns that you get, big or small, in the first 20 years of investing.

So set yourself up between navigate the paradox between lowering risk as much as possible, but getting the returns as high as possible and navigating that paradox is very important. For the success. Obviously, that piggybacks off of rule number one. And one thing I want to point out is if you have a million dollars and you drop 50%, we’re at 500,000, and then if we go back up 50%, down 50, up 50, you think, okay, we’re broken even. Well, 50% of 500 is only 250, so we’re at 750. So it would take, actually, in that example, you go down 50%, we’re at 500. It would take 100% return, two times the return than the one year drop to get just back up to even. So, again, another reason why you want to always navigate that risk versus return.

I always say to young people, manage savings rates. That’s the most important. Don’t worry about returns when you’re young. Until you get to your first million, it’s really not irrelevant, but it’s kind of irrelevant. But then once you have over a million, it’s really how well people can manage the paradox between the risk and the return and also have a peaceful life, a life that your money supports you and saves time, not waste your time, et cetera. So that’s the second lesson I’ve learned about returns. The third lesson is that when looking at statements and looking at returns, a lot of companies and 401 will report like a return on value, which includes your contributions. It doesn’t include the timing of your investment.

So if you really want to know what your true return is, you have to look at a compounded annual growth rate, what I refer to as the kegr, for it to be a really true, it’s got to be a time weighted return, but it looks at the inflows and outflows that you made as an investor, not just what the return of the fund or ETF or stock that you did. And so that’s a very detailed calculation. It’s a very complicated formula. I’m not going to draw it on the screen here, but you need a software that’s able to calculate that for you correctly. And it boggles my mind that a lot of 401K providers don’t provide the correct actual rate of return, which would be a CAGR. That’s a time rate of return.

Not going to call anyone out today, but it’s very surprising that many reputable custodians still don’t have the right return calculation. So just look at, when comparing statements or comparing, you really have to look at the methodology behind how the returns are being calculated, because there’s many ways to do that. The fourth thing is the sequence of return risk. So essentially, when you are saving money, you’re climbing the mountain. It doesn’t matter what path you take, if you get, let’s say, an average of 7%, you start with a million dollars, you’re going to have a 40 year old that turns 65, you’re going to have over 5 million at the top, and you could get that 7% by doing it consistently and going straight up. You could do it by going up high at first and down.

As long as you get that kegr at 7%, you’re going to get the same result. But if you look at declining the mountain, where you’re pulling money out, where the returns are different, we could have scenario a, b and c here, where if you look at their average compound annual growth rates, they could be all be 7%. But when you’re pulling money out, if this investor had good returns at the start and bad at the end, they may still have their principal. In fact, if this person just reversed the returns, then they would run out of money. Let’s say 65 and look until 90 here, and the third person at 7% consistently would actually have less than about 40% of the money at the end.

So setting your financial plan up when the times come to actually use your money to address the sequence of return risk is so crucial because you don’t want your money to dictate how you live your life. You want to have your money support your life by design, regardless of what’s happening in the market, good or bad. So to do that, have backup plans, have fail safes, and let your money compound and grow over the long run, be able to ignore short term noise and address the sequence of return risk. It is the number one risk in retirement, hands down. And it’s just simple math. So the fifth thing is, I’m going to say around houses. So there’s been this big push where houses are great investment. There’s been double digit growth rates recently.

If you get really the last hundred years, and then look at adjustment for inflation, the growth rate on your primary house has really been flat in America. But because of COVID because of interest, rates have been low, there’s been a recent surge. So just be careful. I always view house as a lifestyle choice. If you look at all the phantom cost of a roof repair, or just look at the actual growth rate of most people will move. I’ve googled this five to ten times throughout their life, and it cost money to buy, and then it costs 6% or 7% to sell because of commissions. If you add up all these fees, the interest, the taxes, you’ll never get back. I’m not saying buying is better or worse than renting.

I mean renting in a lot of cases is better financially if you can invest the cost difference between the phantom cost and the monthly payments, in some cases all an individualized calculation. But my lesson learned here is that don’t look at your house as a rate of return. Look at it as a place where you can raise a family, have long lasting memories, and just view it as a lifestyle decision that’s going to save you from so much headache of justification of I’m going to put this in because it’s an investment. I’m going to update my kitchen because of investment. It’s not. It should be all lifestyle. If you do that within boundaries and have good guardrails, you’ll make good decisions. The 6th thing is if you have the fundamentals down in a financial plan, everything that you invest should have no time horizon.

Everything you invest for financial independence, that is because the reality is a good financial plan. You have no idea how long you’re going to live. You have no idea what the market is going to do. So you want to have fail safes in place and you want to have a time horizon that you view as the rest of your life. And if you do that, you’ll not worry about timing the market. You’re not worried about the market being higher low. You’re going to stick to the basics of asset allocation, diversification, dollar cost averaging, things that will work long term in your favor. And again, going back to point number one, we want long term compound environments. The more guesswork you put in to get the short term, it’s just going to ruin the long term in the end.

So there are going to be some things you have to invest in that do have time horizons, like college planning. If you’re going to buy a vacation house with a big down payment, but the big pot of money that you’re going to set aside for financial independence, really, you can forget about time horizon as long as you have backups in place for when the market inevitably goes down about once every seven years because it’s a lifelong journey and good asset allocation diversification. Long term equity investing with the backup plans in place when the down years happen, allow you to take a lifelong look at your time horizon and make good decisions accordingly.