In this episode of FIN-LYT by EWA, Matt Blocki discusses key financial strategies for new parents, focusing on how to manage the increased costs of raising children and ensuring long-term financial stability. He covers the importance of early communication between partners on critical decisions like education, discipline, and housing, emphasizing how these choices can shape a family’s financial future.

The episode also dives into budgeting for higher living expenses, estate planning, and risk management. Matt encourages listeners to create a solid financial plan to minimize stress and enjoy parenthood.

Welcome to Ewa’s finlit podcast. Ewa is a fee only RAA based out of Pittsburgh, Pennsylvania. We hope all listeners of this podcast will benefit as we deep dive into complex financial topics that we will make simplified for you. And we hope that this really serves as a catalyst so that you can make the best financial planning decisions for your family and also save time. Welcome everybody. On today’s episode on Finland by EWa, we are discussing a checklist for new parents. So joined here by Devin, seasoned veteran of the new parents. Three kids. What are the ages?

S

Speaker 2

00:43

14, two and one.

S

Speaker 1

00:45

Oh, you’re living and breathing this. This is perfect. Alright, I’m gonna let you talk. So what do we do, Devin? I’ve got a six year, almost a six year old, but yeah, really important. So figured this would be helpful. A lot of our clients have kids that are having kids and so we want to create a resource that would be helpful for, you know, there’s a lot of financial implications with having a kid as we know. I think it was five or six years ago, I basically said, you know, you’re basically going to spend about 250 grand. This is way more now, I’m sure between when your kid’s born and 18, this is like an average in America and you’re probably going to spend another 250 after for college, for weddings, for some support that you want to give them.

S

Speaker 1

01:26

So we’re talking about half a million bucks. So large chunk of change, totally worth it. Kids are everything. That’s my belief. But it’s purpose in life to best set up your kid for success. There’s a fine line between helping and enabling. And so there’s a lot of stuff to do, there’s a lot of stuff to set yourself up for success. Finances are one of the biggest stresses in America. So today’s episode, we want to alleviate that financial stress and just really simplify this into what are some few things you can do. Big picture to get the financial situation right with having it kid. So Devin, what’s tip number one here?

S

Speaker 2

02:05

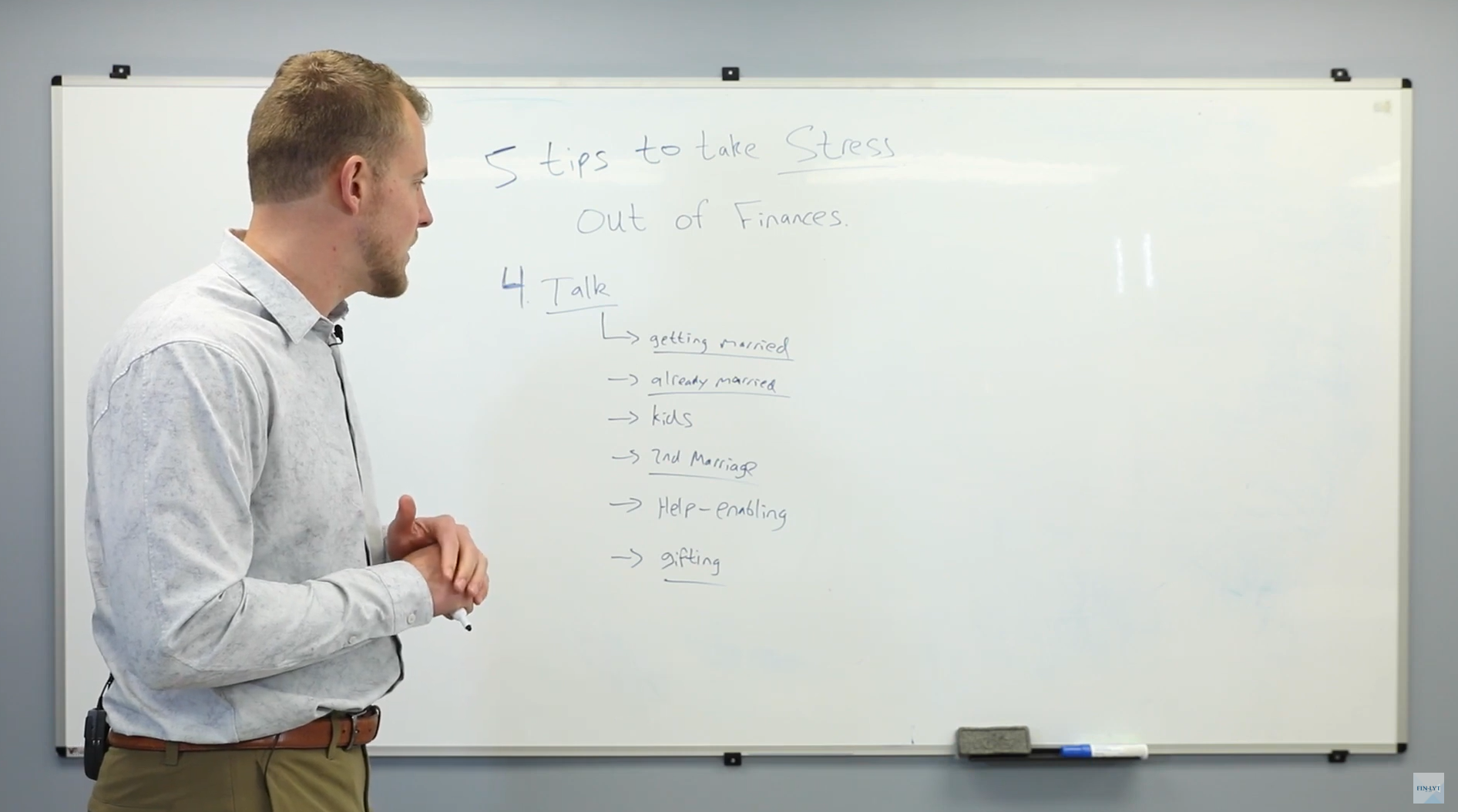

Tip number one is the big C word again. Communicate. Sit down with your partner. Whether it’s when you’re trying, whether it’s when you’re pregnant or right when the baby’s born. Just sit down and have a conversation about how you see this going, right? How do you want to raise this baby or these babies? Everything from discipline styles to which religion do you want to raise them into? What are your thoughts on education, both primary, secondary and college, private versus public school. A big one these days. A huge one these days is screen time. Do we want to get them phones? Because I think kids are asking for phones now at age three, what time, how young was your daughter whenever she asked for one? Has she asked for one on your phone?

S

Speaker 1

02:47

No, not yet.

S

Speaker 2

02:48

Keep it away. Keep it away. Sports, you know, what. What kind of sports? What’s, what’s. What schedule do we want? Just sit down and have that conversation.

S

Speaker 1

02:56

Yes. I think a couple of the big things that we see, like, mistake wise, is that if you don’t have these conversations up front, you know, the average American moves like nine or ten times. I was, like, advocating on it, like, a video of, like, why renting is better than owning, which I own a house. So I like, I love owning house.

S

Speaker 2

03:16

I agree.

S

Speaker 1

03:17

Actually, I hate it because it’s like, I hate the maintenance and stuff, but now that I’ve hired someone to do the most that I do love it, but the renting is just, it just, you can’t argue with. It’s a better financial choice. Like, if you invest the difference, it’s so much. If you move nine times, like the average American, you’re gonna avoid closing costs of like 30 or 40 grand every time. It just. It’s crazy. So the reason I say this is where you send to your school, your kid to school is so important because if you don’t philosophically agree on this upfront and you move a couple times, that’s going to be so costly. Just getting the right school district. So having a public versus private, having a conversation, you know, what kind of school district do we want to be in?

S

Speaker 1

03:55

I find this is super important. I think, especially for the moms, not just in general, and I’ve been in this point probably, I don’t know, 20,000 financial planning meetings. So in general, that’s super important for the moms having that conversation and having the decision of you, maybe we rent until we figure this out and then we settle in that house. We don’t have all these transactional costs that we’re wasting. And then I think religion, like you said, is really important because in summer, literally, you tithe 10%. Is that how we’re gonna raise? And that needs to factor in to the budget? And then as far as other financial concerns, is, what’s the philosophy in college? Are we going to fully pay this? Are we going to be in the position to fully pay this?

S

Speaker 1

04:42

But maybe let them feel the skin in the game so they stay motivated? Are we going to have a flexible approach where we can wait and see if they turn out really motivated regardless of whether we’re going to pay it or not. Obviously it’s a huge blessing if you can pay for your kids college because they’re going to be way ahead of the game if they’re coming out of school without school loans. But what if they don’t come out of college at all because you pay for it all and they don’t have any motivation? That goes back to the discipline style. So all those, I completely agree with huge implications in your financial plan having this conversation. Okay, let’s just go more basic now. So number two, you put plan for higher living expenses. Just adjust accordingly.

S

Speaker 1

05:22

So give us some examples and how big this can be in the budget.

S

Speaker 2

05:25

Well, you kind of jumped off with it in the 500k number. Everybody’s going to be different. I feel like I’m spending five hundred k per month on organic fruit these days.

S

Speaker 1

05:35

Your whole foods or what’s.

S

Speaker 2

05:37

It’s, it’s everywhere. But the kids, the kids are. Yeah, the kids have a great diet. What can I say? I was, I was surviving on Burger King and steakums and they’re eating, you know, five star meals every day. But seriously, your expenses are going to jump. So just be ready for it. I’ve got a list here and I could, the list is long, but some of the top ones, childcare, that’s a huge one. We’re talking four to five figures per month. Per kid.

S

Speaker 1

06:03

Yeah. So what are we talking? Because I think back in the day of my daughter was like 1300 a month for a daycare. So per kid, is that still the number or is it?

S

Speaker 2

06:14

Depends on where you’re living. Right. I think that’s a big one. I think Pittsburgh is a fairly average city. So yeah, I mean, you could spend easily. It’s going to be bare at the bottom is going to be about 1500 month is my guess, upwards. I don’t know if there is a top end of the range. It’s probably three grand or something like that. Again, this is per kid per month. If you have more than one kid, you get a bit of a discount, but it’s not much. So plan accordingly. And these days we typically see dual income households. So both parents are working and so you’re staring down the barrel of paying somebody to take care of your kid or kids during the day.

S

Speaker 1

06:49

That’s why my daughter, you see her on social media, she’s here. I save that 1300 a month, just put her to work. So not only do I save 1300 a month, it’s free labor.

S

Speaker 2

06:57

That’s a win. My book.

S

Speaker 1

06:59

Just kidding, actually, side note, if you’re a business owner, you can actually pay your kid for up to the standard deduction tax free. So that’s like 14,000 something right now. Tax free. So, yeah, pretty cool. So she is on payroll. And, you know, we, she does work through social media. You can do modeling. So quick tip, side tip. We’ve actually done a podcast on that.

S

Speaker 2

07:20

But she a vp, you know, I.

S

Speaker 1

07:24

Mean, she’s gonna be okay.

S

Speaker 2

07:25

Good.

S

Speaker 1

07:25

She’s my boss already, so. Okay, what else?

S

Speaker 2

07:30

So continuing with childcare. Daycare is one type of childcare. You could have nannies, au pairs, et cetera. I don’t know the numbers, but it’s going to be costly whichever route you go. And sometimes it makes sense for one of the spouses to stay home. It just does from a numbers perspective, but also from a parenthood psychological perspective. You know, a lot of people aren’t comfortable just dropping off their kids and having them spend the day with a stranger. So it’s just something to kind of talk about and think about as you are entering the stage of being a parent. So childcare is a big one. Next one are just kind of the miscellaneous equipment and items that you’re going to need as new parents. Diapers, formula, clothes, furniture, car seats.

S

Speaker 2

08:19

I mean, these things are must haves and they can be pretty pricey. I mean, diapers and formula alone is, I don’t know, in the hundreds to thousands per month. So just something to kind of keep in mind and put on the list as you are doing cash flow projections for the future, how is this going to affect our incoming cash flow in the future?

S

Speaker 1

08:43

Yeah. If you were to put a number on it, childcare then just increased expenses and like, diapers, formula, you know, like clothes, all that kind of stuff. And then also college savings. I’ve got a number in my head. I promise I won’t change it. What would your number monthly be for one kid in the Pittsburgh area? You say this is going to have this amount of effect on the cash flow. What would be your average and then what would be your range? Because obviously, if you’re lower income, like, you have to figure it out at a lower. And if you’re higher income, it’s probably going to be higher. But if you had to, like, just.

S

Speaker 2

09:15

Yeah, I mean, some of these are fairly. It’s, it’s not connected to your income. You’ve got to pay for childcare, you know, regardless of where you’re at, that’s a tough if not impossible task, but I’d say roughly. Pretty easy. 2500 to five grand a month.

S

Speaker 1

09:34

Yeah, I was gonna say 3000 a month because I’m thinking 1500 day care, probably 500 of just like you have to feed a. The baby after like diapers, that kind of stuff you do.

S

Speaker 2

09:44

Cloth diapers.

S

Speaker 1

09:45

That’s, that’s gross in my opinion, but no judgment, whoever does it.

S

Speaker 2

09:47

No, it is.

S

Speaker 1

09:49

I think my brother did that. I definitely judged him. But anyways, he. So. And then, you know, 500 a month probably for college savings and 500 a month for miscellaneous. There we are. Three grand.

S

Speaker 2

10:00

Yeah, yeah, I mean, that’s, that was right in my range. So again, whatever the number is, just get ready for it. Right. As best as you can. Calculate that number. But again, you’re going to have to make some sacrifices, some way, shape or form. And I think we’ll get to that in a minute here. On top of that, sort of the. Maybe the medium and size. Sorry, the medium. Small sized items like diapers and car seats. Very, very popular. To spend more on larger things like a new home or a new car.

S

Speaker 1

10:32

Becomes a justification process or your spouse is beating you up. Yeah, this isn’t safe. We need this five star crash rating. We need to be in a good school district. We need a playroom. The kid needs, you know, basically a mansion before you know it. But it does become a huge justification process. So I would say make sure you’re on the same page before the child is born with how to make it work. Because every, I mean, I’ve seen stages of people move. Oh, we grew out of this house. We grew this house. Well, if you had to make it work, you would. But, you know, let’s plan for that up front.

S

Speaker 1

11:06

And then, you know, with the childcare, at some point it becomes like a, if you have two or three kids, if one spouse is making 201, one spouse is making 75. Let’s say like, does that spouse making 75, does it make more economic sense for that spouse at that point just to stay home? Maybe, maybe not. Does it make mental health sense? Maybe, maybe not. Maybe that person enjoys working, maybe they want, you know, so there’s a lot of aspects of that. But from a financial planning standpoint, like being able to stress test your plan, what if we both continue to work? What if one of us stays home? How does that affect our. The college, the retirement, our day to day cash flow, our lifestyle?

S

Speaker 1

11:46

Are we gonna be able to live a peaceful life, financially secure now, financially secure in the future, one that we don’t have a lot of regrets. Minimize regrets and stress testing and having a financial planner to work through those scenarios, I think is super important. So, okay, this is super important one. Now that kids are in the picture, so creating a state plan, not just where assets are going, like, will revocable trust, direct beneficiary want to keep all those up to date, both kids in the picture, it becomes even more important. What’s the big thing you have to decide at this point?

S

Speaker 2

12:21

Something happens to you, probably guardianship.

S

Speaker 1

12:23

Yeah, 100%.

S

Speaker 2

12:25

Which means what happens? What happens to your child or children if you and or your partner, the parents pass and you’re deciding who they essentially, who they live with, who takes care of them. Very, very difficult to think about, but it’s. These days, it’s very important.

S

Speaker 1

12:43

Absolutely. The next one we’d recommend is definitely review insurance coverages. So review. You know, most people think, oh, life insurance. Review your disability insurance. Like, what happens if you don’t have an income to support your family? Review life insurance. What happens if one of you pass? Do we have enough to replace the lifestyle? And, you know, work with a financial professional. Don’t let your spouse say, oh, you’ll be fine, they’ll get remarried. It just. I’ve never heard stupider stuff come out of people’s mouth when talking about life insurance, and I had ten years of experience doing that in my prior place of, you know, before we start this rea. But work with a professional, and they should just tell you what to do. It’s very important to have the right amount of insurance in place.

S

Speaker 1

13:28

And, you know, as a newly married couple, just get a big term life insurance policy. It’s gonna be really cheap. Other considerations. So, you know, rapid fire. Just some quick checklists. Devin, what else should we be thinking about here?

S

Speaker 2

13:41

Yeah, so if you have kind of a normal w two job, a lot of companies offer FSA options, which is a flexible spending account. You can put in money, kind of pre tax, and get tax benefits by using those funds for things like childcare, daycare, for example. It’s not a huge tax savings, but it’s effectively free money if you fit that situation. So you might as well leverage that you have to use.

S

Speaker 1

14:04

That year to year. So get it in, get it out, because if you don’t use it, you lose it.

S

Speaker 2

14:08

It’s not like an HSA, which is.

S

Speaker 1

14:09

Basically a tax free way up to a certain limit to fund childcare cost.

S

Speaker 2

14:13

Exactly. Exactly. So definitely set that up if you can, if you want to. I think that the key to a healthy financial lifestyle is having a buffer fund or an emergency fund. You know, if you’re newly married and the new parents, maybe that emergency fund is a bit too low. So think about and talk about if it is too low, if it needs beefed up. You know, we have a child now and we might need to increase that just to feel safe and secure. Let’s talk about that again. If you have. Well, even if you don’t have a normal w two job, you’re going to be covered by a medical health insurance plan. You have a baby now, so make sure you review that. Add the baby to the policy itself.

S

Speaker 2

14:52

It’s a quick phone call, it’s a quick log on to the portal, but just make sure that’s the case. And then maybe lastly is update your w four, which is the form in your HR portal. Just adding the proper tax situation and adding dependents just to make sure again, so that the withholding that’s coming out, each paycheck is the proper amount. Not too high, not too low.

S

Speaker 1

15:14

Absolutely. I’m trying to think of any rapid fire. Yeah. The other thing I would be a huge proponent of when your kids are old enough. I’ve already started this with my. She’s turning six in October, but is financial literacy training, so not as parents talk about it, but you can never start too early with teaching your kids how money works. I remember I had like three little jars. One was I had to put away for like, you know, for tithing. I grew up very religiously, but dad’s a pastor, so I’m trying to think if I ever use that for candy or something. I didn’t. It was like, it was like all this change. I remember, but, like, you know, that they pass, like, the thing in the church. I would dump it. It would just like, interrupt the whole service.

S

Speaker 1

16:04

I like, do it like, from this high. It’s pretty funny, but yeah, it was like, I don’t know, a couple hundred dollars worth of like, pennies and nickels. But it was a habit, Tommy. Like, here’s how tithing works. And the second one was savings. You know, if I want to go to Walmart and make like, buy a super soaker 2000 or something. And then the third one was, maybe there’s only two. I can’t remember.

S

Speaker 2

16:27

No, it’s saving, spending, and giving away. That’s what you had. You saved some of it for yourself.

S

Speaker 1

16:33

Yeah, but I just realized I spent everything.

S

Speaker 2

16:35

You spent it all? Yeah. On super suckers.

S

Speaker 1

16:37

Yeah. Sorry, parents. Sorry, dad and mom.

S

Speaker 2

16:39

No, I mean, I think that this is. We touched fairly high level on components of your financial life as new parents. I mean, there’s, you know, there’s entire careers baked into how to you be a great parent thoughtfully. But I’ll just throw it out there just to enjoy it. I mean, it’s hard changing diapers. You’re up at night, you’re trying to work, juggle a bunch of different things, and it’s a lot different than when it was just the two of you. But enjoy it. And I think that as financial professionals, we want to try to take that money anxiety away from new parents so that you can enjoy it. And whether you hire one or not, the key is to just soak it all in because it goes by fast.

S

Speaker 1

17:23

Absolutely. Couldn’t agree more. Thanks for joining us, everybody, and look forward to catching you next week. Thanks for tuning in to our podcast. Hopefully you found this helpful. Really hope this is as beneficial and impactful to as many people across the nation as possible. So hit the follow button, make sure to rate the podcast, and please share with any friends or family members that would also find this beneficial. Thank you very much.