1. EWA Firm Initiatives (00:39)

2. 2023 Q4 Recap (05:29)

3. Looking Ahead Into Q1 (11:30)

4. Portfolio Changes (21:00)

5. Financial Planning Tips (33:57)

Welcome, everybody. In this quarter’s video, we’re going to be talking through a look back of quarter four that finished 2023. We’re also going to be providing some economic insight into quarter one of 2024. And then we’re also excited to announce some big changes to the EWA portfolio as well. We’re going to keep you up to date with some relevant financial planning topics. And then also we have some exciting stuff that we’re working on internally, EWA as well. Well, Stephanie, thanks for joining today. Tell us about some of the initiatives that we’re working on internally at EWA. Very excited about these.

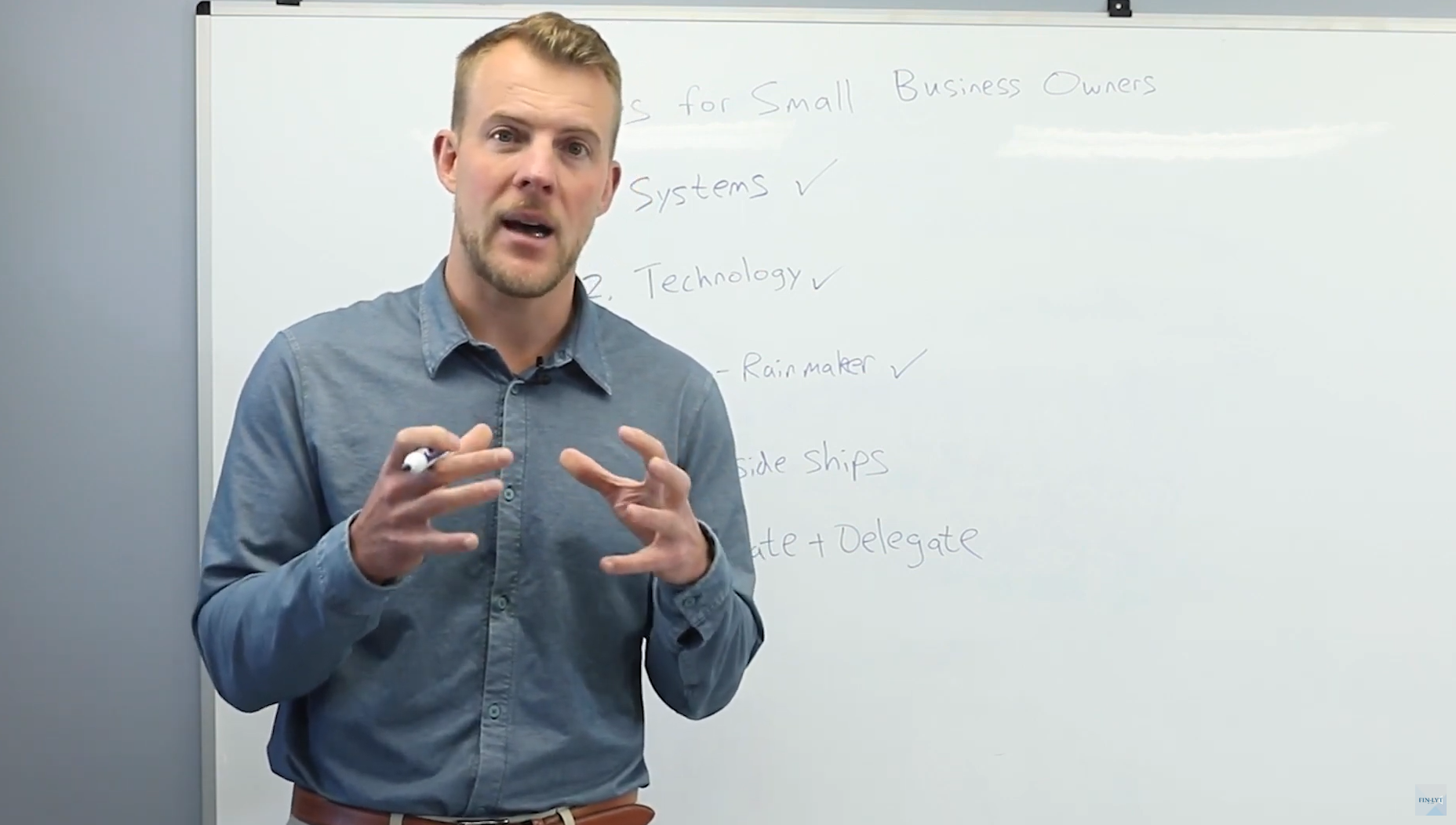

Yeah. So 2024 is a brand new year. We always, in the fall, announced some new firm initiatives, some of which are internal, but a lot of which are really focused on what our clients need in a new year. Looking back at what happened last year and then how we can increase value to our clients, provide even a better experience, become a one stop shop for them for all their financial needs, and reduce stress in their lives. So that’s sort of like where our thought process comes from each year. And I’m very excited to dig into the fact that we really have two major initiatives that are going to affect our clients this year. The first one being we are looking to bring tax services in house to EWA.

So most of our clients who are watching this, they should have received a survey asking, know who their, you know, what they’re spending on CPA services, would they be interested in a service that we would offer them? And we had some great feedback. And I think as a result of that, we’re looking at bringing one of our known cpas in house to service our EWA clients, to provide very high level tax advice, preparing taxes, answering questions from our team, and really streamline the process of data, questions coming from advisors and clients to and from the CPA. So I think this is just invaluable. And I know, Matt, you’ve had a lot of clients that have mentioned to you how nice that would be to have that all in one place.

Yeah, perfect. I think. Couldn’t agree more. One of the biggest value propositions of saving our busy clients their only non renewable resource, which is their time. And this is going to further do that by being able to quarterback and communicate everything. And there’s also been a big push with a lot of CPA firms to raise their prices. And so if we have this direct communication ability with an in house CPA, one of our promises and our goals is to keep those prices at all time low and just be able to kind of package it into the overall fee advisory fee that clients already pay us. We’ll have to do some kind of nominal small fee to a separate entity, obviously for compliance purposes, but we’ll be able to quarter back that along with everything else.

So very excited about that. Yeah, so there’ll definitely be some communication as we move through quarter one, quarter two. So really trying to pinpoint a launch of this potentially in summer of 2024. So, so excited about that. And I think that’ll just help our clients sleep better at night, breathe easier about their taxes every year. That’s a big stressor in the spring. Moving on to the next initiative. I probably feel like this is a little bit on repeat, but we are focusing very heavily on our education of clients this year. So you’ll see some new educational videos, launched website and YouTube. Some revamps, obviously, like limits have changed throughout the year, tax laws change, the markets changed.

So keeping those videos updated, but focusing really on the Finlit by EwA podcast and getting topics out there that are very timely and then also bringing to the world some stories of our clients. So this quarter, we will have two exceptional clients that you sat down with and you were able to talk to them not only about what they do for a living, their businesses, which are very interesting, and then some life stories as well. So you can expand upon that. But really excited to share those with the world. We have some very interesting people that we work with.

Yeah, I found myself, I learned best from other people and real world experiences. And we look forward to publishing these two podcast episodes, one for both business owners, but one specifically is going to be really interesting to most people that love to travel. How to do that for free. This is a close friend of mine that has taught me everything I know in the points world, the credit card points world, and then the other one was been a client for over a decade and also a close friend, but successfully transitioned, has an incredible story, but successfully transitioned the business inside their family and lots of perspective to learn from if you’re a business owner or just anyone. Lots of leadership lessons, et cetera. So we encourage any EWA client if you want to be on the podcast, we’d love to have your perspective.

And I think we attract very incredible people at EWA that we get to partner with and help with their financial journey. So the more information sharing and idea sharing we can put out there, I think the better.

Yeah, absolutely. So definitely reach out if you’d like to be on the podcast, share your story. We can definitely do that. And I would say lastly, this is a big transition year and we’ll talk more about that when we do our look forward. But this is a big transition year in the market potentially. We have a lot of the world’s population going to vote again. We’ll dig into that, but we are looking to add some various offerings to our investment portfolio. So really more to come on that we’re very early in the year, so that’ll be some exciting things to look forward to in our q two video.

Now, Jameson and I are going to talk through the quarter four, look back and what happened in the markets. So, Jameson, if you want to go ahead and kick things off here.

Yeah. So 2023, just year as a whole, and then quarter four, specifically, equity markets in the US, obviously we saw positive returns. Quarter four, as we’ll hit on in a second. Basically, most asset classes were positive, and most of the gains we saw in 2023 were able to erase much of the losses that we saw in 2022. Main catalyst here you saw in the headlines was the Federal Reserve, and what they were announcing about interest rates began to drop. I believe they announced in 2024 they planned to drop interest rates three times, I think. And so a lot of investors really weren’t expecting that. And they were basically able to navigate this soft landing that a lot of people thought was impossible, get the interest rate drop perfect to avoid the economy going into a recession. And so that led to really optimistic investing.

Inflation obviously still exists, but it’s not as high as it once was. So that basically lower inflation, as well as anticipated dropping of interest rates coming. We saw a lot of stock prices in the US basically explode at the end of 2023. And we’ll get into some specifics in a second, but there’s still a lot of really bright spots in the US economy. So things like low unemployment rate, excess consumer spending, all these things led to economic growth, which really was a catalyst as we saw the 2022 and into 2023, where the stock market was down. What didn’t go into a recession was all of these bright spots and positive things still occurring in the economy. But globally, we’re still in what we would call an expansion phase.

There’s still some crosswinds at play and it’s less synchronized us and global economy, but let’s look specifically asset classes. So, Chris, what did well? What didn’t do well? How did asset classes perform?

Yeah.

So overall, across the board, Q four was great. Us growth stocks led the charge. So for Q four, the return was 14.1%. For the year. In 2023, us growth stocks gained 41.2%. So it was really big. Wow, really big win in that sector. Us large cap as a whole did great. The worst performer was commodities. So things like gold, silver, tangible things that you can actually use, those were down slightly, 4.6%. But across the board, the rest of the asset classes did well and gained in the quarter. But looking further into us growth and just the US economy as a whole, or the s, P as a whole, the majority of the growth was led by seven companies. That’s been coined the magnificent seven. So these include Amazon, Google, Microsoft, Nvidia, Apple, Tesla and Meta.

So these seven companies made up the majority of the returns that we saw in the S and P in 2023. So if we look at these seven stocks and just looked at their returns combined, it was 111% for the year compared to just 24% for the s and P. So to your point earlier, the growth companies, those are the ones that are currently excelling, and that did the best in this quarter. So those seven companies made up a lot of the growth that we saw.

So basically, every asset class was positive other than commodities. And the magnificent seven is what led a lot of the US growth. And just to dig a layer deeper, so basically, if you were only investing those seven stocks, which would be like very hard to pick, you’re up 122% or 100, and what is 111? And if you were in the SP 500, you still are up 24%. The big reason for the difference, just, I think to give some context here, is like, if you’re an S and P 500 index investor, those seven stocks maybe only make up 10% of. I don’t know, I’m just guessing, like 10% of the index, maybe, or like 10% of your holding. So you’re still seeing returns, but you’re not just concentrated in those seven stocks.

But, yeah, very interesting to see that those seven stocks made up that big of an impact. Yeah, sure. And much of this was due to the boom in generative AI as these technologies have begun to, businesses have begun to implement them. So really, I guess, two ways. Number one, businesses implementing the technology to make their businesses more productive. Number two, those companies, specifically that we talked about, they’re actually the ones like building the technology and the AI and taking those things to market. So really interesting. But 2023, I think, in general, just was a perfect example of rewarding, patient, long term diversified investors. We saw 2022, a lot of very poor performing asset classes. And if you stayed, invested, stayed the course you were rewarded in 2023.

So, Chris, what’s your favorite, speaking of AI and all this growth, what’s your favorite AI invention you’ve seen?

So I didn’t know if were going to actually talk about this or not, but if you’re watching the video, I have glasses on, so I’m excited for the new developments that could come with that. With the AI integrated with the glasses. And I saw something on a video showing, instead of computer monitors, potentially could be projecting the screens of what you’re looking at in your glasses. I think that would be awesome. If you’re working remotely or working in an airport or something like that, it would be extremely useful.

You’re better on the eyes. No blue light.

Exactly.

Yeah. Wow. Anyway, don’t base any of your investment philosophy off of our AI picks, but very interesting.

Well, now for our look forward into quarter one of 2024. So we have four common themes here, Stephanie, but let’s talk about the first one. So the first one is all about the federal rates. They’ve reduced rates. What’s going to happen in the future, and more importantly, what’s the impact to our clients if they go up or they go down or they stay the same?

Right. I mean, I’ve heard from just about everyone I’ve talked to, oh, the Fed is going to bring rates down in 2024. Well, yeah, maybe not. So I think the big thing to remember is that volatility with the bond sector and rates were higher in 2023. That that was something that was kind of unprecedented. We hadn’t really seen volatility to that degree in the bond space in a while. So it’s likely that the Fed could reduce rates this year, and if so, that would have a positive impact on those who took out potentially mortgage loans at higher rates. An opportunity to potentially refinance. But to be honest, this is a year of the unknown. We have quite a bit changing, potentially, in the political landscape and the global landscape.

So regardless of what happens with the Fed this year, it’s likely to not be a change upward, it’s likely to be a stable environment or a slight decrease in the rate environment, targeting potentially somewhere between 75 basis points to 125 basis points over the course of the next 18 month period. So could be some opportunity for refinancing, could be some opportunity on people that have held off on big purchase, big ticket items that carry a higher loan rate. Or potentially it’s a discussion as to do you finance these items more in cash? So those are topics that our clients are going to be coming to us with this year, which we will, as things progress and as the landscape unfolds this year, we’ll be able to give them some more advice on that.

So I think it’s a safe bet to assume things will at least be stable, potentially a decline and looking for opportunities to potentially refinance credit and whatnot.

Absolutely. And then as far as from the portfolio perspective, we’re going to get into this in more detail on the next section. But the duration of, if you’re a client that has fixed income in the portfolio, which means you’re probably near to or in retirement, and we need to have that state stability. If you’re taking rmds out or taking distributions, we’re able to get the money out without a loss. We’ve had a pretty low duration under five years over the last couple of years. And as interest rates go up or down, if interest rates go up and you’re already locked in, bond prices fall and vice versa. If interest rates go down, your bond price are going to go up because that’s going to make the bonds that you have at the higher interest rates very much more attractive.

So of course, this is something, again, we’ll get into. But as far as impact from a portfolio perspective for our clients, we have a very diversified approach. So if interest rates go up, we’re going to be able to take advantage of that. And if interest rates go down, we also have a safe, stable way for clients that are in that distribution mode to make sure they’re getting that money out without taking any kind of losses. So again, we’ll get into that. But just there’s the personal finance world of the refinancing, and then there’s the portfolio world that could. Overall, I think a lot of people initially were very hesitant on what’s the Fed doing? They’re ruining the economy, et cetera.

But on the flip side of that, with inflation and just looking at housing prices and how they were skyrocketing and how that was affecting people, how they were able to navigate this was actually quite impressive. It was artful. I think this should be a celebration. They were able to do this, lower inflation and also avoid a recession all at the same time. It’s one of the best economic feats in the history of the United States. Not well talked about it, because that doesn’t sell well. But that’s just the reality. Inflation was getting out of control. And so when people say, oh, the rates are going to go down, that could be true.

But again, remember, we’re humans, and if rates go back to where they were, people are greedy and people are envious, and they want the house that’s just as big as their friend’s house. And so I would anticipate, and we’re not making any bets here because even though the Fed has come out and said we intend to keep rates stable and go down, if inflation gets out of control again, they’re going to go right back up. So we’re not making any significant bets here. We’re staying disciplined, we’re staying thoughtful, and making sure that clients are protected no matter whether they go up or down. We have a stable strategy in place.

Right. We always talk about this, and you talk about this in another video, which is to control your money temperature regardless of the market conditions, that’s going to be the focus, and continue to be the focus, which is staying the course for the long term, not making knee jerk decisions based upon market conditions and rate environments. So that will always be the mean, I think that segues into another piece of the look forward, which is inflation. And like you said, the Fed was able to very artfully, carefully bring inflation down. But we’re still above, like we’ve heard targets between two and three. We’re still at three or a little bit above, and that’s anticipated to stay for quite a while. So what does that mean? That means the cost of where things are right now are probably going to stay.

We’re not going to see a decrease in the cost of everyday goods and so forth. But that also means that in order to have a portfolio that actually is growing and you’re netting return, you need to have a portfolio that’s returning more than what the inflation rate is. So we’re talking about bonds, we’re talking about rates. If a bond is returning 3% and inflation is three and a half, you’re technically losing half a percent on that return. So continuing to focus on a portfolio that is for the long term that meets your needs, that’s going to enable you to hit those long term goals, is really still what we’re focused on, whether that is in the equity market or a blend of the bond and the equity markets together.

Absolutely. Well, I think a common theme here before we get into the inevitable that everyone’s expecting of the tech, AI, tech, et cetera. So there’s a staggering statistic that’s going to happen in 2024. That’s basically theme is going to be the unknown.

Right?

So tell us about this, Stephanie.

Yeah, I’ll steal this line. But I mean, 2024, as you said, it’s the year of the unknown. And I didn’t know this statistic until we started researching and whatnot. But 49% of the world is in an election year this year. So 49% of the global population will be eligible, whether they do or not, to cast a vote for the leader of their country this year.

That’s 64 countries, and those countries are some of the biggest. United States is an election year. So basically, if we round up 1%, half of the world is going to have a say in major political change in 2024.

Right. And most people, the thought is we get a lot of questions, well, what happens if so and so wins the election? What happens if so and so wins the election? And the impact is, I think, far reaching in terms of international relations, in terms of just general philosophy and whatnot. So, I mean, this is where being, again, staying the course long term and knowing exactly why you’re doing what you’re doing is important, because 50% of the world could change. We could have a changing leadership, major leadership.

So I think just focusing on the things that we can control, these things are going to happen outside, focusing on the things you can control and being cognizant, having flexibility in our portfolio, ensuring that our clients are in the right mindset, coaching them through hard decisions, that’s still going to be the focus, regardless of what happens with that 50% of the world.

Absolutely. Well, that brings us to the last and talk about change and the unknown. Is this AI, artificial intelligence and tech. So this was a huge run, really, in the big seven. Most of those companies had a huge AI play in 2023, and now tech valuations are at an all time high. So talk to us about 2024 and the impact of AI and technology.

Yeah, so I think big thing is, AI is here to stay. We’ve talked significantly about how technology embracing technology enables you to grow as a business. It also enables the world to continue to grow around you. All the technology that you’re using day to day, even just like your phone, it’s literally a computer in your pocket. But there are significant investments in pieces of this technology that comprise just every aspect of AI, all the way down through your vehicles and whatnot. So we had a number of clients ask us, well, this is obviously like an industry that it’s newer, it’s blowing up. You hear about it constantly, whether it’s. You’re using chat, GPT for things, whether or not you’re using voice activation, how are we incorporating that into our portfolio? And so we’ll get to that piece in a moment.

But I think what’s important to realize is that most of this is already kind of like baked into our portfolio in the large cap space. So we are exposed to companies who are heavily invested in and innovating in AI. Same with tech. But we will make a small shift, which we’ll get into in a moment. But we do have our finger on where we should be in a proper allocation overall to tech and AI in general. And we are going to make, again, a small tactical shift to bring ourselves right up to where we feel the benchmark should be in this category.

So we are not going to go straight AI, we’re not going to stock picking into the top seven, we’re not going to wait to meta or Tesla and Nvidia, any of the type things, but we will get some exposure to the potential upswing in that industry.

Absolutely. Next up, we’re real excited to talk about some of the changes we’re going to make to the EWA portfolio to align with the common theme of 2024, which is the unknown.

Right.

So, Stephanie, the first thing I want to talk about is our large cap section of our portfolios. Last year, as James and Chris mentioned in the look back, there was these big seven stocks that really took advantage of having good balance sheet and be able to invest heavily in AI. So moving forward in the large cap, the reason, just as a quick reiteration of why we have it structured the way we do, on the screen, you’re going to see a nice chart that shows the returns from 2003 to 2023, the returns of these us large cap investments, and then also the risk. So obviously, we want the returns as high as possible, the risk as low as possible.

So the best relationship we got here over the last 20 years was actually this minimum volatility fund, which focuses on defensive companies, healthcare, energy, things that have to exist, whether we’re in a recession or a booming economy. And you have the momentum, which is a factor based ETF, which did the best over the last 20 years, but also came with the higher risk than the market. You can see slightly, the standard deviation almost was 16 versus the market being right about 15. So what we found is if we mix these two, this is what’s referred to by some as a spectrum strategy, right? If we mix minimum volatility and momentum, we’re able to get market like returns with much lower risk.

And so that’s a position to further that we’re able to favor one or the other, depending on if we’re an early, mid, late or recession type of economy. But that’s just to reiterate why we have done things the way we have. And we’re going to be shifting a little bit heavier into both of those. But the big move that worked out great over the past year was the shift to quality. And quality really means that the companies we’re investing in are in the bottom 25% of companies in their peer groups that have the lowest amount of debt, not the bottom 25% of performers, but the bottom 25% of debt on their balance sheets. And so these companies have done so well because the shift in this really happened before the interest rates went up like crazy.

And so one of the reasons why these funds have done so well is these companies with low debt were not affected or impacted nearly as much as a company that had a low debt. If you have a payment that’s ballooning with double the interest, that’s really going to affect the bottom line. But if you have a company with a low debt on your balance sheet, then high interest rates just aren’t going to have that much of an effect, comparatively speaking. So quality really represents high profitability and low leverage. And this is something because of the unknown of 2024, these companies will be dynamic, republican, Democrat, overseas, political ramifications of, again, 49% of the population going to vote this year over 64 countries. These companies will respond very quickly and dynamically, regardless of change.

That’s why you’re going to see the biggest shift in the quality, both in the US large cap space and in the international space as well.

Right.

But Stephanie, one of the things that we’re doing, speaking about internationally, is we had this emerging market fund, which excluded China.

Right.

And we’re making the decision now to sell out of that and go back in. So give us some of the rationale behind that.

Yeah, absolutely. So, I mean, investing 101 is buy low, sell high. So, number one, in looking at this strategy, we put this in place because there were some tensions, there was some geopolitical, some just overall global sentiment about shifting away from China in terms of their impact on the United States, like the balance of trade, so many imports and so forth. But we decided to get into this fund last year and we got in very low. And now at this point, we’ve seen some nice growth in this, and it’s just basically time to get out.

And this kind of echoes our sentiment of, I want to say, cautious optimism that regardless of the 49% of voters, that they’re going to go out to the polls this year, that the political situation will stabilize, will calm down, and that the global economy is going to look better as a whole, not excluding any specific nations. So we want to make sure we get exposure to all of those countries, both developed and in emerging markets.

Yeah. In China recently, we’re going to talk about AI, but they had made a big investment in semiconductors. And the other factors we’re looking at for emerging markets is really three countries. So Japan, Mexico and India. So Japan has really not had the best returns over the last couple of decades, but the companies we found are becoming more and more well run. So lots of value there, right?

They’re finally kind of hitting that stride.

Absolutely. And then India is obviously turning into a powerhouse. Some people think it could know bigger than. Bigger than China, and I tend to agree with that. That could be a whole podcast episode in itself. And then Mexico is, regardless of political ramifications, cost savings, et cetera, imports, exports, Mexico is the easiest for the United States. And so forget about the political disagreements about a wall. We’re not talking about citizenship, we’re talking about exports, imports. And so Mexico is going to benefit the highest from those changes as well.

Absolutely. I mean, just the geographic positioning makes it a logical place for outsourcing, for United States to be able to build and do business in another nation. So, yes, take the border situation. We’re not talking about border, we’re not talking about immigration. We’re just purely talking about the balance of trade, import, export.

So that leaves us with really three things. So one is we do not like commodities, but we do have this ticker called XLB, which is heavily invested in chemicals, et cetera, which is essentially a commodity alternative. One of the reasons we don’t like commodities is not just the horrible performance over the last couple of decades, but also the fact is you don’t get a dividend. You don’t get to really see anything unless there’s a good return. However, XLB is investing in companies like PPG, which is close to home here, that chemicals, precious metals, et cetera, are going to have a similar correlation where if the market goes down, typically these companies, like precious metals will go up. An inverse relationship really is a risk return play.

Yeah, and we added this in last year as a bit of a stabilizing factor, if you would, because these are materials and companies that produce materials that are going to be necessary regardless of the market conditions. So it is a little bit of a hedge, if you want to use that word. But specifically, this does not include energy, which is huge energy, and oil really create volatility. They can change so quickly. So this is exclusive of that specific piece of the broad commodities basket. So we like this as a stabilizer factor. It’s just a small 2% portion of the portfolio. So it’s not going to change anything drastically one way or another, but it does add to core stability. So we like that.

Absolutely. We’ll define that as like the other category, very small, 2%, but definitely a good head. And then the other fund that we’re adding into that other category in the ticker called Sox. Soxx. And this is specifically around AI, but not investing directly in AI. It’s a semiconductor. So if you think about AI is run on semiconductors, not semiconductors. AI does not exist. Similar to, I think, of two analogies I can use. One would be the Internet. When the Internet was invented, it was a game changer. And you could have invested in some companies with a.com boss that would have make you bankrupt. You could have invested some companies long term that did incredibly well investing in the Internet. But if you could have invested in the Internet directly, there would have been a game changer, just in general.

And then same thing for the blockchain in relation to bitcoin. There’s all these different coins in. Bitcoin is still the main one, but there’s ethereum, et cetera. The blockchain is a technology that even most Fortune 500, Fortune 100 companies have adopted for security and efficiency purposes of their businesses. And so investing in the blockchain, which you naturally do through big us companies and even overseas, is an incredible idea. We’re not a proponent at all of a speculative coin investment. It’s fine if you have a small portion of your net worth, but not something that we’re going to directly recommend. Sure, even though it’s been on the rise, but now going back to AI, so there’s all these big players. What we saw in 2023 was really seven companies that just crushed the index.

I mean, it made up for four times the return of the index itself, just if you invested in those seven companies. So the common theme was AI. And so there’s just going to be this huge rush that obviously companies with big balance sheets, lots of cash, have a competitive advantage to buy startup companies and incorporate. And you’ve seen that already. We’re not in the game of guessing. We’re not in the game of gambling. We’re in the game of discipline, long term investing and making sure your money is supporting your life by design. So to take advantage of this AI as safely as possible.

We’re adding 2% into this semiconductor ETF, which is going to have big names that you recognize that as AI goes, regardless of what companies take good advantage of it, profitable advantage of it, or do not, we’re taking the guessing game out of it. All of them, regardless, have to use these semiconductors. This is really a long term play, our belief that AI is here to stay, regardless of what regulations the government puts into place, et cetera. We need these things to exist in order to progress.

Yeah, basically, if you boil it down, we took a look at this, well, two things. We took a look at our portfolio in general and said, where do we want to be from a technology allocation in general, and were slightly underweight in technology after last year because we did shift to quality. We said, okay, well, a, let’s bring that up to where we want it to be for our benchmark purposes. But okay, how do we do this? So take a look at the big picture of AI, like you said. And if you break it down into its basic components, that’s where you want to invest.

You want to invest in something that has to exist, and it will continue to exist, that will support these businesses, those that stay in business, those that go out of business, those that hang out in the middle of the road. This technology supports all of that growth. So it’s a much more tactical bet, if you would, to use the word. But we know that for everything else to exist, this also has to exist. So it makes a lot more logical sense to kind of get in at the root of that technology versus the end product.

Absolutely. And then one of the things you’re going to see is that some intentional shifts in the fixed income, if you’re an investor that has fixed income with us with a slight adjustment in duration. So historically, with interest rates being low, we’ve kept the duration under five years, which really helped to allow us to dynamically shift into higher paying interest rate bonds without selling at a loss.

Right.

For example, in 2022, if all you had was a long term duration, you would have had to sell at a loss to get your own money. So you’re going to see more of a layering strategy. We’re not forecasting if rates are going to stay the same, higher or lower. We’re developing a strategy that takes advantage of current high rates, but also has the flexibility if rates change for the better or for the worse. So that your number one rule of money is you don’t lose money. Number two rules you don’t forget about. Rule number one, that’s a Warren Buffett quote. So that’s the strategy. But with these changes, you’re going to see two things. One is lower cost, and two is going to be a duration shift from under five years to just under six years.

So a slight shift, but very intentional shift in the fixed income part of the portfolio.

Yeah, I mean, as you mentioned, the cost of the portfolio. We always are proponents of a low cost portfolio. All of these changes, I think it’s important to note, actually bring the expense ratio of the portfolio down a little bit. So no increase in cost in the portfolio. And there is one other change we should just note. It’s not like a strategy change, it’s a ticker change. So in our small cap space, we are going to go from the vanguard small cap value in the qualified space and the Vanguard small cap growth in the non qualified space into ticker IJR, which is the iShares small cap. So no change in the amount that’s in the small cap sleeve versus on any side of the portfolio. Just a ticker shift there so that you’ll have the ishares in your mid cap and your small cap.

Awesome.

Yeah.

Well, Stephanie, thanks for joining and EWA clients. Please reach out if you have any questions and look forward to catching you next quarter.

Ben and I are here to talk about some financial planning tips as we head into 2024. Specifically, what can be implemented in quarter one of 2024. So, Ben, what should people be thinking about?

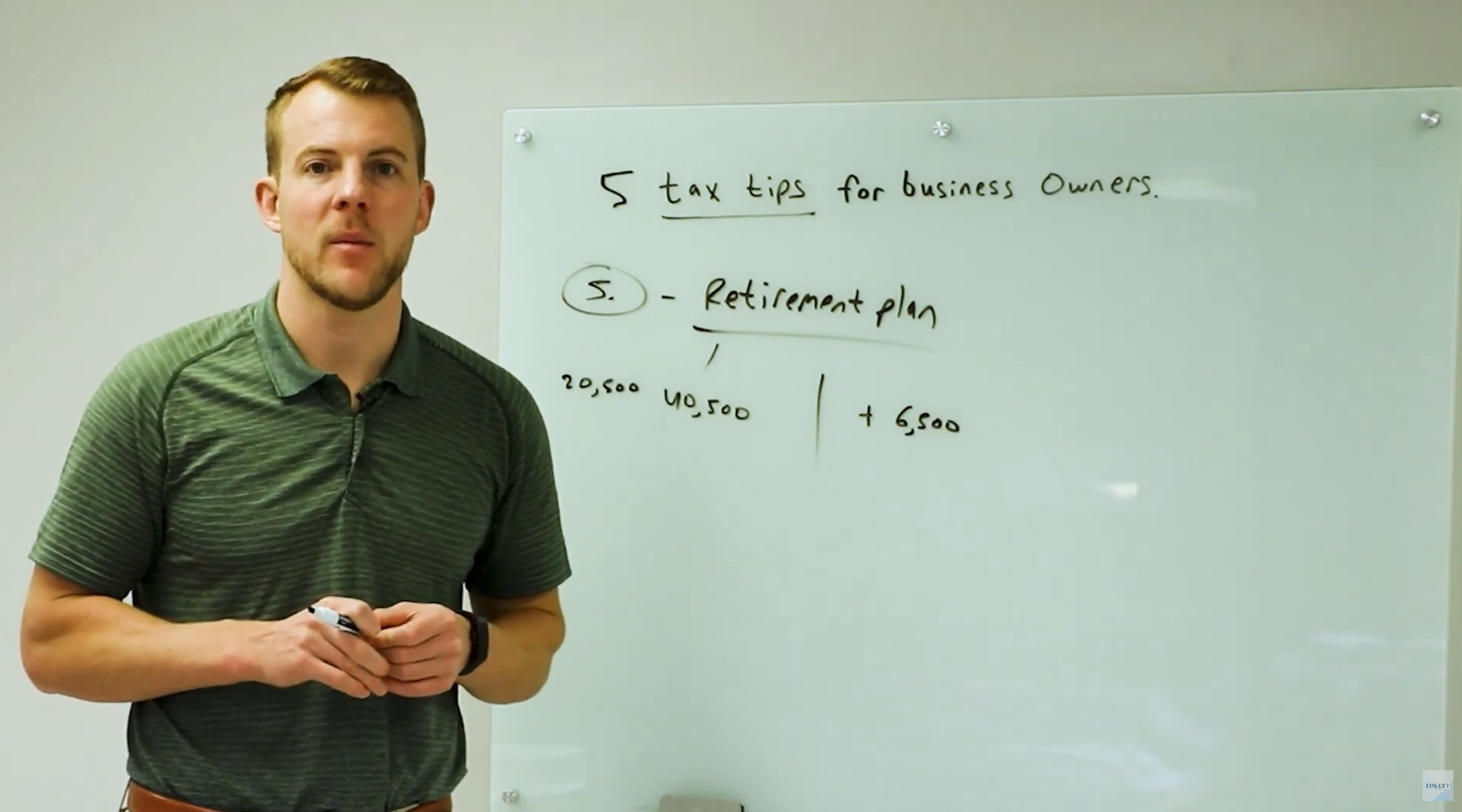

Yeah, a couple of annual limits that have changed due to inflation that we want to make sure that we’re adjusting with our clients here early in Q one 2024. First one we’re going to talk about is the 401K limits. Those have increased. 22,500 was the limit in 2023. Those are now 23,000 in 2024. So a $500 increase in what you can defer into your calendar year and the catch up contribution. So if you’re over the age of 50, that remains at 7500. So if you’re under the age of 50, you can defer 23,000 into your 401K plan. If you’re over the age of 50, you can defer 30,500 into your other.

Thing, along with the limit, which is the total amount that can go into a retirement plan. Again, under the age of 50 is increased from 66,000 to 69,000 over the age of 50s. Can still get that catch up on top of that.

So that’s important if you’re getting an employer match, if you’re making after tax contributions, trying to get up to that full four one five C limit. Just be aware, that limit did increase to 69,000.

Okay. What other limits have changed?

Yeah, the IRA limit increased from 6500 to 7000. So if you’re funding a traditional or Roth IRA, be aware that limit increased.

If you’re over the age of 50, you get an extra thousand. So 8000.

Correct. So other thing we want to be aware of, and this is actually a pretty sizable jump, was that the IRS limit for maximum compensation for any sort of employer match that you may receive increased to $345,000. So this is important if you’re planning out your 401K contributions throughout the year. Let’s say you’re a high income earner and you’re over $345,000. Let’s just say, for example, you earn 500,000, and you think I’m getting a 3% match from my employer. Well, you’re not getting a 3% match on that full 500,000. You’re getting a 3% match on what the IRS deems as the maximum allowable compensation limit, which is 345,000. So be aware as you’re planning out your contribution percentages, if you want to make sure that you’re hitting the annual limits.

If you’re over that limit, any sort of match you receive is only going to be based on your first 345,000 of compensation.

Very good to know. The other thing, the Social Security tax on your income has increased up to now, the first $168,600. So that is one downside of this. Paid a little bit more in Social Security tax on a little bit more of your income. The standard deduction has gone up, obviously, both for single and married tax filers. Single has gone up to 14,600. Married filers has gone up to 29,200. And as well as there’s some tax bracket increases. So one example, in 2023, the 37% tax bracket kicked in at $693,750. In 2024, the 37% tax bracket kicks in at $731,200. So a little bit of a tax break. Just in all tax brackets across the board, HSA funding for a family plan has increased to $8,300 per year. And this is an important one. Ben, what happened with gifting and the estate exemption?

Yeah. So the gifting limits went up a little bit as well. An individual can now gift $18,000 to an individual without having to report it as a gift or have it count against your lifetime gift exemption. So that’s $18,000 per individual. So if a married couple wanted to combine their gift. That could be 36,000 that can go to an individual in the year of 2024 without having to report it in any sort of capacity. Only other limit that we want to make sure that we’re aware of is that the individual estate tax lifetime exemption bumped up with inflation, so it’s now $13.61 million person. So again, if you’re a married couple, that’s a little over 27 million that you can pass completely estate tax free. If you have a net worth over that estate exemption, you’re subject to a 40% estate tax.

That’s why it’s really important to, if it fits in your financial plan, to be aware of these gifting limits, making sure that you’re getting money out of your estate, and if it’s a priority for you to avoid that estate tax.

Good to know. So a couple of just tips then for 2024, obviously make sure that all of your contributions are adjusted to hit these maxes. If you are maxing out some of these accounts, another tip would be contribute to whatever you can early on in the year. So one example would be like backdoor Roth IRA health savings account that gets the full twelve months of accumulation can be applicable with your 401K. However, there is one caveat we want to make sure you’re aware of. If you do have an employer match, if you over contribute early on in the year, you can miss out on some of the match because it’s not getting you up to that IRS max compensation limit. So only max out your 401k early on if there is no match.

If you are, just talk to your HR department, make sure you’re getting the full match. And then other tips. So there are some things you can still fund for 2023 before you file your taxes in April. So things like you could still fund an IRA for last year, your HSA, if you’re a business owner, any type of profit share cash balance plan, all of these things still have, you can still fund for 2023. So if you haven’t maximized them, you still have a little bit of time to do so. Anything else to add, Ben?

No, just be aware that all of these financial planning topics we’ll be addressing with all of our clients, and if you have any questions about how any of these limits apply to your financial plan, we do ask you that you reach out or consult with a financial advisor.