In this episode of FIN LYT by EWA, Matt Blocki answers the pressing question that often keeps investors awake at night: “How do I know if my advisor has me in a good portfolio?”

Throughout this podcast Matt discusses:

• EWA’s portfolio construction process

• The crucial elements of a well-diversified portfolio- Asset allocation and diversification

• Red flags to watch out for

• Strategies to evaluate your portfolio’s performance and risk.

• Tips for building a strong and sustainable investment plan

If you’ve ever wondered how your portfolio was created and if its components will help you meet your goal to live your life by design, tune in to this episode for all the answers you’ve been seeking.

Welcome to EWA’s Fin-lyt podcast. EWA is a fee -only RIA based at Pittsburgh, Pennsylvania. We hope all listeners of this podcast will benefit as we deep dive into complex financial topics that we will make simplified for you.

And we hope that this really serves as a catalyst so that you can make the best financial planning decisions for your family and also save time. Welcome, everybody. On today’s Finlet by EWA episode, we are going to be talking about portfolio construction.

Now, we did a podcast on investment philosophies that we follow at EWA. But the purpose of this episode is really to answer questions. I think a lot of clients or potential clients, not just for us, but around the country, have such as who makes the investment decisions, how are the investment decisions made?

Is it your team? You guys look young. Is it someone behind the scenes? Is it Fidelity? Is it Charles Schwab? What’s really happening? So today’s episode, we want to address all of those things. And regardless whether you’re with us or not, we hope that this information is educational and helpful so that you know if you’re working with the right firm, the right advisor, the right company, et cetera.

So just to start off. So first of all, we believe working with a financial advisor should not just be about portfolio management. We believe portfolio management is extremely important to grow your wealth as efficiently as possible.

But for the price you pay, an advisor should really be providing comprehensive financial planning and be there when you need them, not you be there when they need you, for example, during an annual review.

I believe most of the value happens outside of your annual or semi -annual or quarterly reviews. It happens when you have a problem. Is your advisor and their team available with a quick turnaround to save your only non -renewable resource, which is your time?

With that being said, today we’re going to focus specifically on the portfolio management and decision making that happens. The first thing that I want to point out is that 90% or more historically, so if you look at the last 100 years of returns that an investor could have in the stock market, 90% or more the consistency of those returns can be comprised of three simple things.

If you follow these three things, it doesn’t matter on a high level what are the decisions are made. Those three things are one is asset allocating. Asset allocating is just the exercise of getting the highest return with the lowest unit of risk possible.

Highest return, bear with the lowest amount of risk. This typically means you’re investing in three to eight sectors in the market and not having all your eggs in one basket. Some people get this confused with point number two, which is diversification.

Point number two, diversification, is in each one of those baskets, we’re going to use seven baskets as an example. Having large cap, companies like Amazon, Apple, Google, mid cap would be a company like Panera, small cap would be a startup that is publicly traded, but something that you’ve probably not heard of before.

Eventually we’ll grow to a mid or large cap. International developed, emerging markets, real estate investment trust, and then fixed income, which would be bond. If you have those seven categories, we’re going to find that is asset allocation.

Diversification just means in each category, do you hold enough companies to be diversified if one goes down, are you going to be affected or go unaffected? I always use an analogy of football, asset allocation, you want to have a quarterback, a wide receiver, running back, et cetera.

Diversification means you have backup. If your quarterback goes down, you don’t need a wide receiver taking that position. You have a second string quarterback that’s able to go in. In investment terms, in those seven baskets, if you were to open up the basket, you would see at a minimum 25 companies, so 25 stocks.

That reduces 80% of the risk of diversification. To reduce 90% of the risk, you need 100 stocks. Studies have shown anything above 100 doesn’t further reduce the risk dramatically. At least 100 gives you the maximum risk reduction, but at the same time, having 25 has more risk, but could come with higher returns if you pick the right companies.

Again, 90% of your returns are received by not picking the right companies, but by being asset allocated, diversified within with high quality companies. Then also, the third principle is just being in the market long term.

If you look at standard deviation, which is the measure of risk, there’s a really scary probability if you only have an investment time horizon of one, even three years in equities. Is my money going to be higher than what I put it in?

Now, if you look at rolling period, you’ll see that there’s a lot of risk. of 20 years, at least looking at the S &P 500, there’s no 20 year rolling period that the S &P 500 has a negative return. And if you actually look at 30 year rolling periods, then purely from a stand -in aviation compared to risk standpoint, if you have a 30 year time horizon, it’s not an argument to be made, it’s just a fact that stocks are actually safer than bonds.

Because if you have a 30 year stock portfolio, the stand -in aviation, the returns stay relatively high, historically 9 to 10%, if we look at the S &P 500 and reinvesting dividends, bonds, the interest rate fluctuations that occur over 30 years, if you bought a 30 year bond, the chance that you’re gonna sell that at a gain or a loss, 15 or 16 or 17 years in, there’s a high risk to that.

So the risk of principal loss really disappears in the longer time horizon you have. So before we go to the decision, I just wanna point out that any investor with their advisor, without their advisor, can predict 90% of their concerns by asset allocating, diversifying, and staying in the market long term.

If you do those three things, this is really hard to mess up, and you’re going to capture returns that will meet your financial plan. With that being said, decisions that you make, you need to make decisions on what categories are you and asset allocating to.

What percentage are we going to put in? 40% to large cap, 10% in the mid cap, 5% in the small cap. This is where institutional companies have CFA’s and really people that are evaluating what type of economy we’re in can be really helpful to determine the right asset allocation risk given that timeframe.

The diversification decision is essentially picking, do I want a mutual fund? Do I want an ETF? Do I want a stock or multiple stocks to serve my diversification? The third decision is what advisor or do I even need an advisor to stay in the long term?

This is harder than most people think because when you have a million dollars, if it drops 50% to half a million, even if it goes up 50%, you’re only at 750, it’s usually having a quarterback to guide you through.

There’s a lot of psychological hit that occurs when a dollar is lost versus a dollar is gained. Having someone to talk to and stay in the plan during those scary time periods is very important to falling point number three.

Going back to point number one, we’re going to address how we do that specifically in a second. For point number two for diversification, just as a general philosophy, US markets, if we look over 30 -year rolling periods, only 5% of active mutual fund managers have outperformed the indexes over 30 years.

One year almost half of them do. So if an advisor is selling, oh, this mutual fund could do really great. Over time, if you hold on that mutual fund, you’d be better off most of the time just following an index.

So ETF investing is how you do this, and ETFs generally have the lowest fees, much lower fees in mutual funds, sometimes even a tenth of what a mutual fund would charge you. So how we diversify typically in US investments is through ETFs or individual stock ownership through our direct indexing platform.

Our belief is that for active management, this would only be appropriate for really good managers in an international emerging market space where consistent results have been achieved with the best managers that actually have stake on the ground of the countries that they are investing in.

So now to get to the third. So at EWA, we follow a quarterly process. It doesn’t mean we’re making changes in the portfolio every quarter. It means that we’re keeping ourselves accountable every quarter to evaluate on a top -down analysis.

everything that should be evaluated in the portfolio. So if you’re an EWA client, you’re already asked allocated, you’re already diversified. We’re already telling you, you know, what you put in the stock market is only allocated towards long -term goals.

If you say you’re going to buy a house next year, that money’s not in the stock market, it’s going to be in cash. So we have those three things down pat. So assuming we have those three things down pat, we want to go into greater detail around how the quarterly process works.

So on a quarterly basis, the first thing we’re doing is we’re getting on the phone with some institutional partnerships we have with Fidelity and BlackRock. And they’re providing some of the smartest minds for us on a quarterly call, and they’re providing all of their research.

And so the first thing we ask is what stage of the business cycle that we in. And if we look on this page, it’s the early stage, you can see profits are growing rapidly, policy still stimulative, inventory is low, sales improve, activity rebounds.

Mid, as an example, would be profit growth peaks, policy neutral, equilibrium is reached, no pun intended for our name. Late economies, the growth moderating, credit titans, earnings under pressure, and then obviously recession, which is everyone is scared about typically, or the news really over centralizes when we’re following activity, profits are declining, typically stock prices are declining as well.

So the reason why we’re asking what type of business cycle are we in is not at all with saying should we get it out of the market. So I want to address that for a second first. So now we can see on the screen the reason why even if Fidelity’s institutional team or BlackRock’s institution were to say, hey, we think we’re in a recession or recession’s coming.

That means stock market’s probably going to fall. And we’re going to tell our clients you’ve still got to stay in. Here is why. If we try to get in the timing game and we say, Let’s get out of the market.

Well, that decision has to be timed right twice. First of all, asset allocation is an address. As you can see, every country typically is not in the same stage at all. So, asset allocating is an all -weather portfolio and allows your portfolios a whole to be less risk to even make sense and get returns even during a recession.

Not every recession, but really to lower the volatility when that’s occurring and then accelerate the recovery when it occurs. So there’s a study that’s been shown, and this is showing 20 years of data that an S &P 500 investment of $100 ,000 made on December 31st of 1992 until December 31st of 2012.

If you had just put your money in the S &P 500 index, $100 ,000, it would have grown to $484 ,000 and $494 ,696. And so that would have been an 8 .2% kegger compound on annual growth rate. However, On the left, it shows that the average equity investor only made it to $229 ,000.

So less than half of the returns were actually received. And the reason for that is the timing risk. So if we time before recession, that means we have to time it right twice. We have to get back in before the market’s gone up.

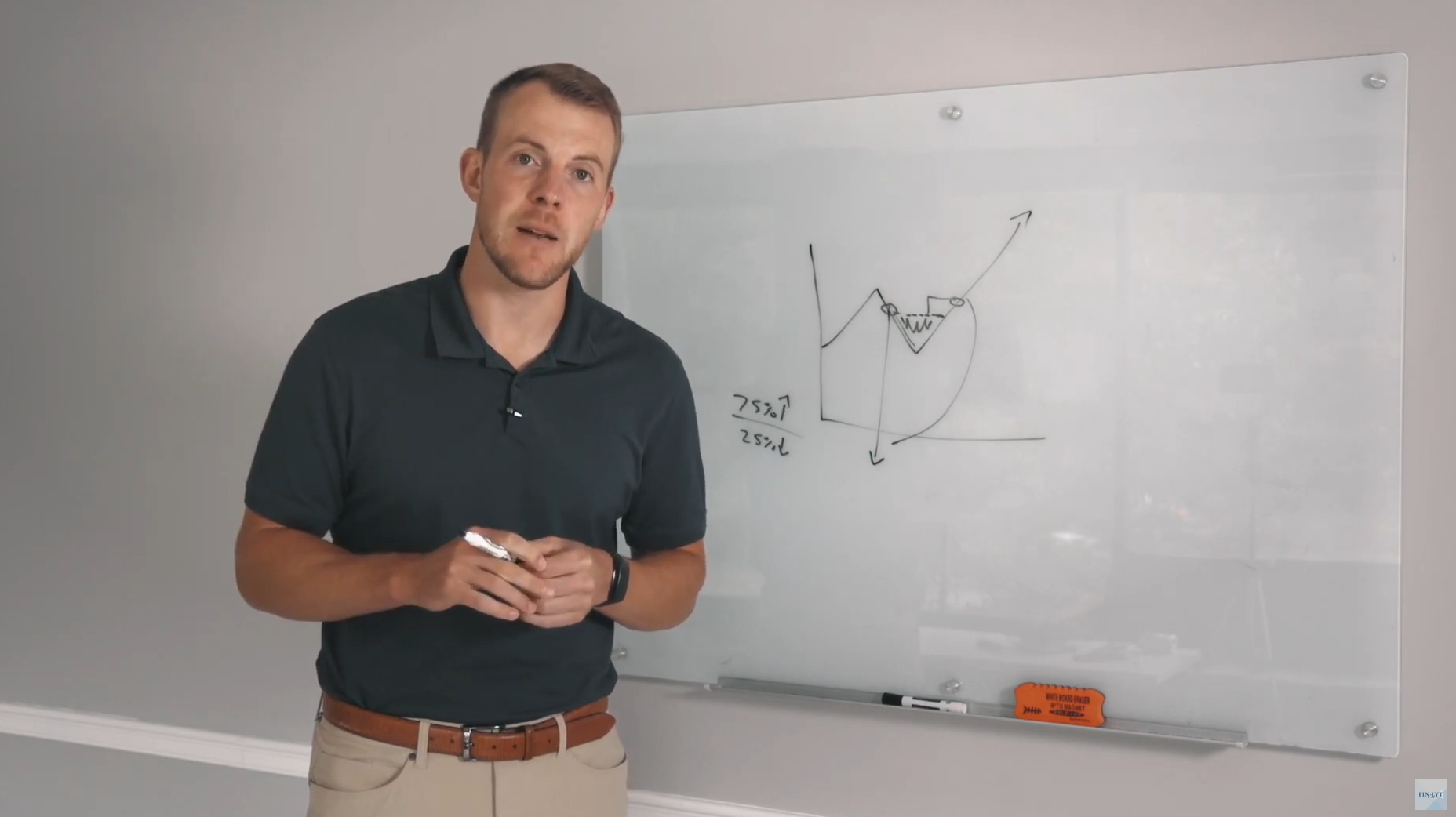

And you can see most investors on the left side of the screen here, there’s large inflows when the market’s good, there’s large outflows after the drops occurred. And so not only statistically is it impossible to time the market consistently over a lifetime portfolio, it’s dangerous too.

Because even if we get it right where we get out and then the market drops for 10%, well, if we don’t get it back in before the market’s come back up 10%, and in fact, let’s say it’s gone up 15%, we’ve actually just missed on those returns.

And generally speaking, the markets are up, S &P 500 is up 75% of the time. If we look back at the last 100 years, it’s only down 25% of the time. So if we get out, we now have a 75% chance that we’re losing that bet.

And let’s make it very clear, time in the market is not investing, it is betting. So imagine, you know, going to a casino, if you play Blackjack or Roulette, the odds are against your favor, eventually statistically, you’re gonna lose all your money.

However, if you are the casino, you’re the house, statistically, eventually, even if you have a bad night, long -term you’re gonna make money. That’s why casinos always make money, millions if not billions of dollars.

So to be the house from an investment standpoint, no questions asked, you have to stay in the market at all time, whether we’re in an early, a mid, a late, or a recession, no matter what you are, even if we’re being told we’re in a recession or even if we already are in a recession, we’re staying in the market because we’re the house and we’re only interested in sound investment principles and we’re only interested in making money, not gambling away, which will eventually mean we lose the money.

So as you can see, the first information we’re extracting from these quarterly calls are what type of economy? me we’re in regardless we’re still staying in. Well, you probably ask, well, why do you care if you’re just going to tell us to stay in the market, why do you care what stage we’re in?

Well, the stage we’re in is very important because if we ask to allocate properly, diversify properly and we’re going to stay in the market, if that’s the goal, the companies that are set up to position the best risk reduction and the best growth, history has shown that certain companies perform better in certain sectors.

As you can see on the screen here, early cycle, real estate, consumer discretionary and industrials, those three historically have been the best performers in early cycles, whereas consumer staples, healthcare, energy, utilities are not as favorable.

That doesn’t mean we’re going to just suddenly get out of certain sectors, but we are going to use our rebalancing tools, not move you out of the market or time the market, but we may move you into less volatile holdings.

We may focus on financials. in an early cycle and keep that position through a minute and late and then go less financials in a recession just using that as an example. That data is so important to not timing -wise, but as a pilot to how we navigate the ship and how we acidic allocate, how we make our diversification decisions, those do change, but those all change while we’re always staying in the market.

To prove this point, we’re going to look at some data that shows the last 70 years of stock market data, bond market data, and cash data. If we look at this left hand of the screen, we’ll circle this for you.

In early stages, stocks in general just hit the bottom of the park. The annualized nominal return of stocks in early stage economies is between 20 and 25%. Bonds are just above 5 and cash is, we’ll say, right around 4.

Mid -stocks drop to 15. Bonds are about the same, right around 5. Cash is about the same. Late -stocks drop down drastically. Over the last 70 years, stocks have performed just around 5% to 6% in late -stage economies.

Bonds right around 5. Cash goes up a little bit. Now, in recession, this is why everyone wants to time the market, stocks over recessions over the last 70 years have averaged between negative 5 and negative 10%.

If a client asks, well, if we know stocks are going to do poorly, US stocks are going to do poorly during recessions while I stay in. Two reasons. One, the timing of that, if we get it wrong, 75% chance of losing.

So we don’t want to go from being the house of the casino to being a player in the casino. Sure, we could avoid some short -term noise, but getting back in at the right time, impossible. So we’d rather ride it out and guarantee the returns that we can receive long -term.

firm, historically guarantee based upon if we stay in the market. Secondly is if we utilize all three principles together, if we utilize long -term investing, asset allocation, diversification all together, if we look on the right hand of the screen, this portfolio shows an asset -allocated portfolio.

It shows a asset -allocated portfolio, a diversified portfolio. This shows 35% of domestic equities, US equities, 24% in foreign, 40% in bonds. You have those asset classes covered. Those domestic equities include large, mid, small.

The foreign equities include some emerging markets. The bonds include the US aggregate bond index. What we can see here now is that the returns in an early, in a mid, in a late, in a recession, and these are all adjusted for inflation.

Inflation historically in the US has been 3%. all the way across the board here. Real return means inflation’s already been taken into consideration. So 4% add inflation, that means you’re actually getting 7% regardless of whether we’re in an early stage, regardless of whether we’re in a mid stage, regardless of when we’re late, regardless of when we’re recession.

So just to sum up here, if you asset allocate and diversify, you put yourself in a position to be an all weather investor. You put yourself in a position to invest regardless of what’s happened in the economy as a whole.

And you put yourself in the position to be the casino and make money off of all the different offerings that a casino has because you’re the house. You’re going to make money long term in US investments, in international, in emerging markets.

They’re all going to behave in different patterns. And so that does two things. It allows you to always stay in, eliminate timing off the table. And it also allows you to live life by design because these assets do behave differently at different times.

And so if you are needing to go on vacation or needing to live your life and we’re still in a recession in the US, great, pull from your international, pull from your bonds, which aren’t getting hit.

So you can still live your life by design regardless of what’s happening. So that’s how we make our decision on a quarterly basis. And that’s why you can see we’re rebalancing in and out of sectors. But what you’ll never see us do is try to time the market.

We’re going to move you to cash. What you will always see us do is asset allocate very wisely, is make good diversification decisions behind the scene that are very low cost, and always have a financial plan that’s supporting your life by design.

And that each bucket of money has a specific goal and designation to ensure the maximum chance that actually respects and supports your goal, which allows you to live your life by design. We welcome any questions.

And thank you so much for tuning in. This week of FinLip by EWA. Thanks for tuning in to our podcast. Hopefully you found this helpful. Really hope this is as beneficial and impactful to as many people across the nation as possible.

So hit the follow button. Make sure to rate the podcast and please share with any friends or family members that would also find this beneficial. Thank you very much.