Please select a default template!

Married couples have the option to file their federal tax returns jointly or separately. While the IRS mostly rewards couples to file jointly, there are some scenarios where filing separately could make sense. In this blog, we’re going to break down a few examples of where it would make sense to file taxes jointly, and where it would make sense to file taxes separately– strictly from a financial standpoint.

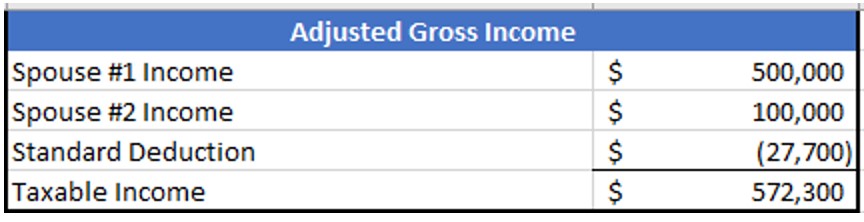

In this example, let’s assume there are two spouses– one spouse earns $500,000 and the other spouse earns $100,000. If they choose to file taxes jointly, assuming they take the 2023 Standard Deduction of $27,700 and have no other above-the-line deductions, they would show a taxable income of $572,300. Above-the-line deductions could consist of Traditional 401(k) plan contributions, Health Savings Account contributions, or Traditional IRA contributions. For simplicity’s sake– let’s assume those deductions are zero.

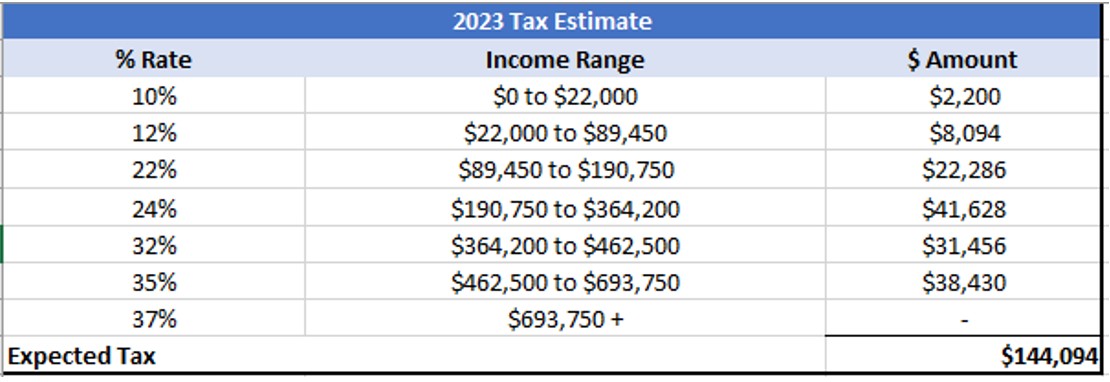

The United States tax bracket is progressive– so portions of income are taxed at 10%, 12% and so on all the way up to the highest marginal income tax rate of 37%. In 2023, the 37% tax bracket starts at $693,750, so this couple avoids that bracket entirely. Based on current tax code, this couple can estimate their federal tax liability to be $144,094

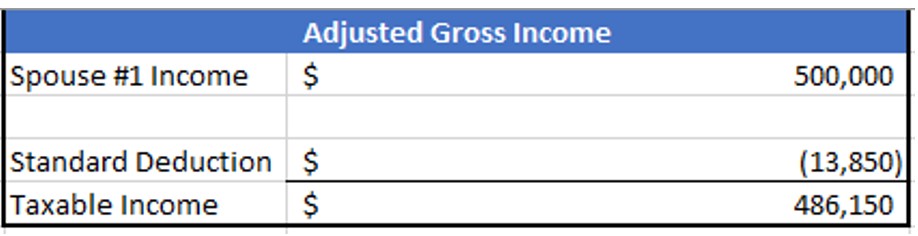

Let’s assume the exact same scenario– one spouse earning $500,000 and the other earning $100,000. Only this time, the two spouses choose to file their taxes separately, rather than jointly.S

The spouse earning $500,000 will show a taxable income of $486,150 after taking the standard deduction (limited to $13,850 if filing separately) and assuming no other deductions.

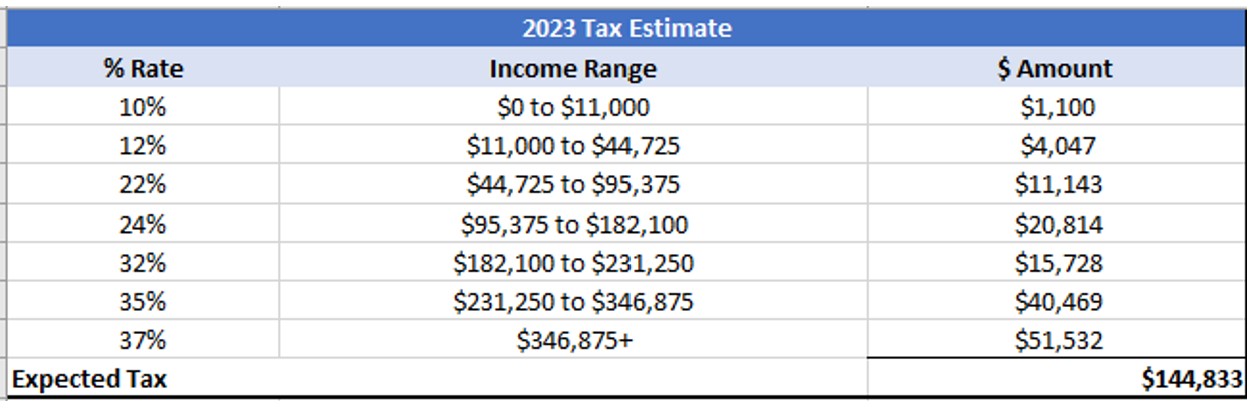

Where this is significant is that, with spouses filing separately, the 37% tax bracket begins at $346,875 of income. So, this spouse will see ~$130,000 of their income taxed at the highest federal rate– a rate which was entirely avoided had they filed jointly.

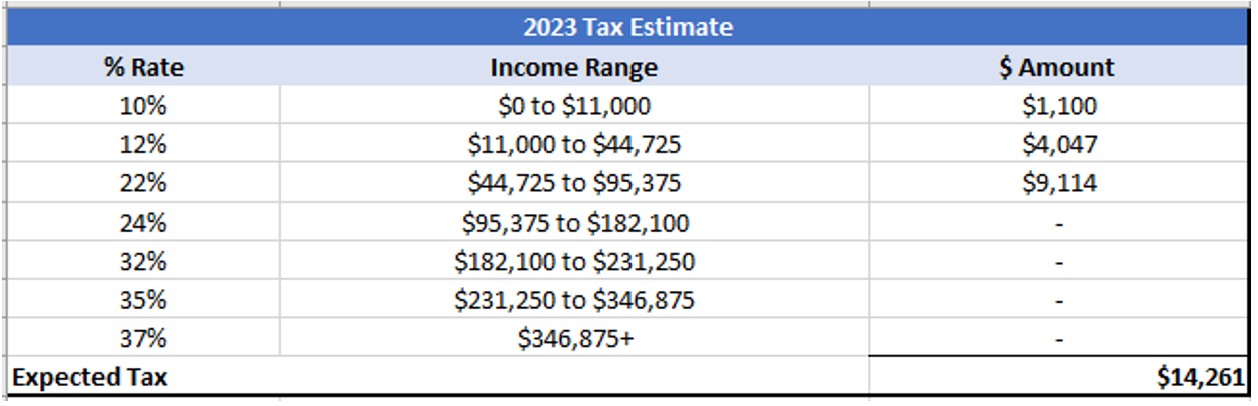

Repeating the same exercise with the spouse earning $100,000, showing a taxable income of $86,150 after the standard deduction, shows the following numbers:

In summary– if the spouses file jointly, they’d owe approximately $144,094 in federal tax. If they decided to file separately, that number jumps to a combined $159,094.

In this example, the couple would save approximately $15,000 in federal taxes by choosing to file jointly.

When would it make sense to consider filing taxes separately, as opposed to jointly? Consider a scenario similar to above– one spouse earning $500,000 and the other earning $100,000. What if the spouse earning $100,000 had a sizable student loan balance? In order to keep their student loan payment as low as possible, they could consider filing taxes separately– as some student loan repayment programs (ex: Pay As You Earn, Income-Based Repayment) would just take the $100k spouse’s income into account when calculating payment (and not the $500k earning spouse) if and only if they filed separately.

In this example, let’s assume by filing separately this spouse is able to keep his/her student loan payment at approximately $500/month. If the two spouses were filing jointly, and both incomes were used to calculate the student loan payment, the student loan payment could be as high as $4,000/month (depending on interest rate, length of the loan, etc.). This $3,500/month difference in payments ($42,000/year) more than outweighs the $15,000 tax savings the couple would have received had they been married filing jointly. Particularly if the $100k spouse is pursuing a student loan forgiveness program and trying to keep the monthly payment as low as possible (in order to maximize the balance forgiven), then filing separately could make sense.

Before deciding whether to file federal tax returns jointly or separately, it would be wise to consult with a tax and financial advisor who is familiar with your personal financial plan and circumstances to make the best decision.

___________________________________________________________________

Equilibrium Wealth Advisors is a registered investment advisor. The contents of this article are for educational purposes only and do not represent investment advice.

Stock markets are volatile, and the prices of equity securities fluctuate based on changes in a company’s financial condition and overall market and economic conditions. Although common stocks have historically generated higher average total returns than fixed-income securities over the long-term, common stocks also have experienced significantly more volatility in those returns and, in certain periods, have significantly underperformed relative to fixed-income securities. An adverse event, such as an unfavorable earnings report, may depress the value of a particular common stock held by the Fund. A common stock may also decline due to factors which affect a particular industry or industries, such as labor shortages or increased production costs and competitive conditions within an industry. For dividend-paying stocks, dividends are not guaranteed and may decrease without notice.

Past performance is no guarantee of future results. The change in investment value reflects the appreciation or depreciation due to price changes, plus any distributions and income earned during the report period, less any transaction costs, sales charges, or fees. Gain/loss and holding period information may not reflect adjustments required for tax reporting purposes. You should verify such information when calculating reportable gain or loss.

This content has been prepared for general information purposes only and is intended to provide a summary of the subject matter covered. It does not purport to be comprehensive or to give advice. The views expressed are the views of the writer at the time of issue and may change over time. This is not an offer document, and does not constitute an offer, invitation, investment advice or inducement to distribute or purchase securities, shares, units or other interests or to enter into an investment agreement. No person should rely on the content and/or act on the basis of any matter contained in this document. The tax and estate planning information provided is general in nature. It is provided for informational purposes only and should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.