Please select a default template!

Congratulations! You’ve done a great job investing and building your nest egg for retirement. You’ve made it to the end of your career and you’re now ready to enjoy some well-deserved free time with loved ones. Although there’s plenty to look forward to on the horizon, it’s important to ensure the proper planning is in place.

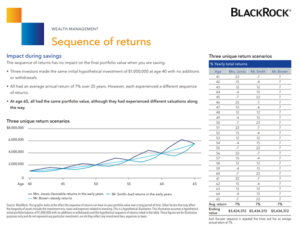

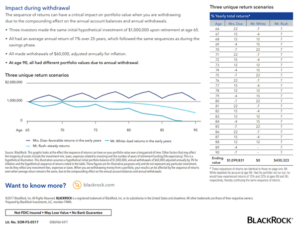

Monitoring the size, frequency, and timing of portfolio withdrawals in Retirement is of utmost importance. This is especially so in the early years of Retirement when withdrawing too much can potentially cause an irreparable drain on your portfolio (first ten to fifteen years). This is highlighted to an even greater degree when large and/or frequent distributions are made during a down market.

Becoming a disciplined, patient, long-term investor is an important part of wealth accumulation. Set up systematic savings and treat these contributions as “non-negotiable” in your ongoing budget. In doing so, you’ll be shocked at the power of compounding returns once Retirement is around the corner.

Once a calculated, comfortable financial plan is in place, it’s significantly easier to remove the emotional response to temporary market downturns. There’s comfort in knowing you’re on the right track to achieve your long-term goals.

The blind spot for most investors: Scaling the mountain tends to be less risky than the descent.

The sequence of returns you experience in your portfolio is more critical once the investment time horizon begins to narrow.

A pitfall to be wary of is processing large withdrawals during a down market in the early Retirement years. While it’s perfectly acceptable to utilize your well-earned savings in Retirement, it would be prudent to pull from liquid investments (savings, money market, cash value from life insurance) at the beginning of the “rocky descent” rather than selling equity exposure.

The first picture below shows 3 different investors who:

The second example now shows 3 investors who are descending the mountain. These 3 retirees have the following in common:

Why are the results so different now? Because of sequence of return risk.

Because of the sequence of return risk seen clearly here, EWA has put several potential fail safes into place for our retired clients that are actively distributing.

The first one is to help ensure all clients have 7 years of safe money to ensure they are never likely to have to take at an actual loss.

The second one is the “guardrail approach”.

The next step is to help ensure the size of the distribution(s) taken maintains a healthy portfolio.

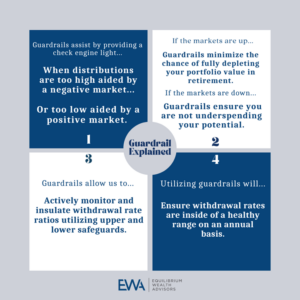

An important planning topic to become familiar with and monitor is a Retirement Income Guardrail Strategy. “Guardrails” are put in place to monitor the amount withdrawn from your portfolio to help ensure that you are staying within a safe withdrawal rate. Guardrails should be placed at upper and lower bounds to track the amount withdrawn and to help ensure changes are implemented should a barrier be breached. If you’re withdrawing above the upper guardrail, a decrease in spending is appropriate. If you’re withdrawing below the lower guardrail, an increase in spending is prudent if your goal is to maximize retirement income. Guardrails help ensure that you are not spending too much, or to the contrary, underspending your potential in retirement.

The follow-up question tends to be, “how much can one distribute on an annual basis to help ensure the portfolio remains “healthy?”

EWA monitors retirement distributions and their effects on a household portfolio via Monte Carlo Analysis and Withdrawal Rate Analysis.

Monte Carlo Analysis stress tests a portfolio for the likelihood of future success. By running hundreds of variations in asset returns, longevity, inflation rates, and tax rates, Monte Carlo Analysis helps to showcase how a portfolio would fare in ever-changing conditions. It’s important to consistently revisit these stress tests as factors/situations continue to evolve.

Using a standard withdrawal rate percentage primarily ensures a system is in place to monitor portfolio distributions.

There are many opposing viewpoints to the “4% Rule,” but the importance at EWA is to actively manage and have a finger on the pulse of the risk component of the retirement portfolio.

Withdrawal Rate analysis occurs by monitoring the total amount withdrawn on an annual basis vs the total market value of the account(s). Using a 4% baseline with upper and lower guardrails at 3% and 5%, respectively, helps to ensure monitoring and accountability occurs on a consistent basis.

Monitoring withdrawal rates helps to provide warning signs. Think of it as a check-engine indicator in your car. When a warning sign pops up, it’s important to act. At EWA, these warning signs lead to deeper financial planning discussions surrounding your goals and their future likelihood of success.