Please select a default template!

With Pension plans becoming less common and Social Security payments potentially not meeting one’s basic expenses in retirement, many retirees often wonder how to supplement their retirement income to support a sustained lifestyle. From this perspective, an annuity can seem worthwhile to one’s financial plan.

While often discussed as a guaranteed income stream that can participate in the upside of the stock market but without the downside risk, many annuities can have certain pitfalls that make them generally unsuitable for most financial plans. This blog (as a follow-up to the podcast we did on the subject), will seek to explore the different types of annuities available in the marketplace and the issues associated with them.

Simply put, think of an annuity contract as the inverse of a permanent life insurance contract. In a traditional life insurance contract, the insured pays a little bit each month to the insurance company. A beneficiary receives a lump-sum payment from the company at the insured’s death. An annuity works in the exact opposite way. An insured gives a large lump-sum payment to the insurance company, and in return, the insurance company pays the insured an amount back (monthly, semi-annually, or annually depending on the contract).

There are many types of annuities on the marketplace, but the three most common products seen are fixed annuities, index annuities, and variable annuities.

Fixed annuities can either be funded by a single, one-time lump sum or can be considered “deferred”, in which case the annuitant sets a date when the insurance company begins making payments. A few different riders are available to add to fixed annuities, but generally speaking, they provide a fixed, guaranteed payout to the annuitant.

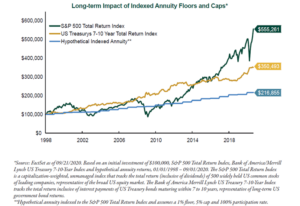

Index annuities are marketed as annuity contracts that can participate in the upside of a specific market index (the S&P 500, for example) while also providing a floor on the contract to protect the contract holder from negative stock market years.

Variable annuities are structured similarly to fixed annuities initially. But instead of providing a fixed, guaranteed payment structure, variable annuities are invested in mutual fund sub-accounts to seek market growth, meaning payments can fluctuate and are not guaranteed.

From the many annuities that have been analyzed, the three most commonly analyzed issues regarding annuities are as follows:

Many annuities, particularly variable and indexed ones, can charge large fees if the annuitant wishes to terminate the contract before a certain period. The sooner the surrender period, oftentimes the higher the charge. These surrender charges can make annuity contracts highly illiquid, meaning there could be a significant stress on one’s financial plan if the annuity needed to be taken out early. For example, in the first year of a variable annuity, the surrender charge could be as high as 7% of the contract’s premium.

This gripe is specific to index annuities, often sold as having downside protection during a market drop while also participating in upside during risky markets. Generally, index annuities do protect contract holders during down market swings. But there is often a cap on the market growth during market upside. While this is a relief for many retirees, the cap on the market upside can lead to a dramatic difference in overall investment returns. Many index annuities do not consider dividends in their calculations nor allow any of these to be reinvested into the annuity contract itself. This severely hinders the growth of the contract, as reinvested dividends have generally been a key factor in sustained portfolio growth over the long term.

Not only are annuities commissionable products for those who sell them, but they can also be extremely costly from an ongoing fee standpoint. Many variable annuities, for example, charge different types of fees: one for the contract itself, one for each sub-account that the annuity is invested in, and one for any riders added on to the contract (guaranteed income rider, a period certain rider, etc.). Some of the annuities that have been analyzed can charge up to 4% per year, which could eat away at any discussed investment returns.

Let’s assume a client needs to spend $150,000/year to maintain her lifestyle in retirement. Further, let’s assume Social Security pays her $50,000/year and that her fixed costs (utilities, groceries, rent, etc.) total $75,000/year. In this case, there is a $25,000/year gap between Social Security and the client’s fixed costs. A fixed annuity could make sense to help bridge that gap and provide her with a guaranteed income stream to help meet those obligations.

If you are considering an annuity for your financial plan, please be aware of the type of annuity being presented and all the fees and riders associated with that specific contract. If you have an existing annuity and would like it analyzed, please consult with a trusted financial advisory team.