For many retirees, the transition from a lifetime of saving to a phase of spending can include psychological challenges and strategic dilemmas. This shift is not just about financial readiness but also about psychological adaptation to changes in lifestyle and purpose. A common pattern among retirees, especially those who have been diligent savers throughout their careers, is the difficulty in switching gears from saving to spending. This issue often stems from a deeply ingrained habit of accumulation, which can make the act of drawing down savings in retirement feel counterintuitive or even reckless. This psychological barrier can be so strong that it not only causes stress and anxiety but can also lead to tension between partners and, in worst case scenarios, a significant decrease in life satisfaction during what should be a rewarding phase of life.

The crux of retirement planning isn’t simply about how much you’ve saved—it’s also about how you plan to spend those savings without the fear of running out. Here are some common strategies and their adaptations:

Originally derived from historical market data, the 4% rule suggests that retirees can withdraw 4% of their retirement portfolio annually, adjusted for inflation, with a reasonable expectation that their funds will last through 30 years of retirement. However, potential market volatility and longer life expectancies have led to recent questions about whether this percentage is still valid, with some experts suggesting a more conservative approach.

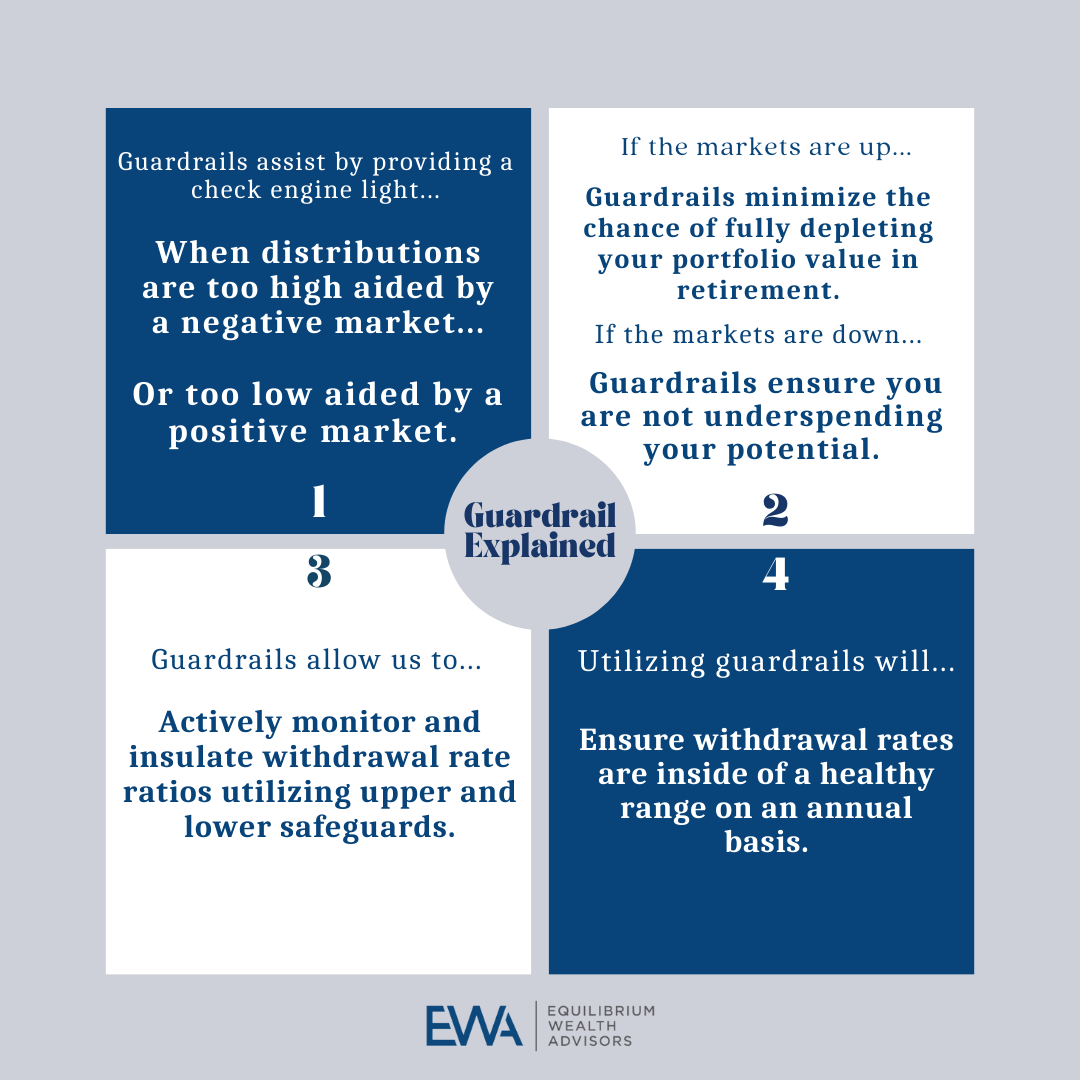

Rather than sticking to a rigid withdrawal rate, some financial planners recommend a more flexible approach that adjusts spending based on market performance and personal circumstances. The “guardrails” strategy is a popular method where spending limits are adjusted annually to reflect the current economic environment and portfolio performance.

This approach involves dividing retirement savings into different “buckets” for various stages of retirement or for different spending purposes (e.g., daily living expenses, travel, healthcare). Each bucket can be invested differently based on when the funds will be needed, providing a structured yet flexible spending plan

While often debated, annuities could be a part of the retirement portfolio for those seeking guaranteed income. Fixed annuities can provide a steady income stream, complementing other retirement funds and Social Security benefits. However, the key is to ensure that annuities are used judiciously, as they can also be restrictive, and many come with high fees.

One of the most significant tasks for financial advisors working with retirees is helping them overcome the fear of spending their savings. This often involves regular discussions about the purpose of their accumulated wealth and encouraging clients to enjoy the fruits of their life’s work. For many retirees, giving themselves permission to spend can be assisted through regular financial reviews with their financial advisor in which spending plans may be adjusted. This can provide additional assurance that retirees that they are on the right track. Also, maintaining clear and honest communication with loved ones and trusted advisors can help alleviate worries about legacy and inheritance issues. Lastly, building a savings plan before beginning to spend can help ensure the plan matches the retirees’ lifestyle and goals.

The journey into retirement should be as meticulously planned as one’s career. With the right guidance, retirees can overcome the psychological challenges and strategic complexities of turning their savings into a sustainable income. This helps ensure not just financial security, but also the prospective fulfillment that most seek in retirement.