Please select a default template!

Having a sound investment strategy is crucial to giving an investor greater peace of mind, rather than relying solely on investment returns when making life decisions. At EWA, we follow 4 main investment pillars that help allow our clients to live life by design, rather than default, and make life choices without relying entirely on market returns. These 4 concepts are asset allocation, diversification, long term investing, and asset location.

1st Pillar: Asset Allocation:

Asset allocation is the act of investing in different categories of investments, called asset classes. If you’re a football fan, this is like having the correct player at each position on the field. Rather than having the quarterback on the field alone, you want a running back, a wide receiver, tight end, etc. all on the field to build a well-rounded offense. The same concept applies to an investment strategy, it is important to have multiple asset classes present to form a well-rounded portfolio. Generally, we see one of two scenarios:

To be in scenario 2, limiting downside risk is very important, which can be managed through proper asset allocation. An example would be if parts of the market are down when your kid is going to college or you are in retirement, it is crucial that you have a portion of your portfolio that can be taken out at a gain.

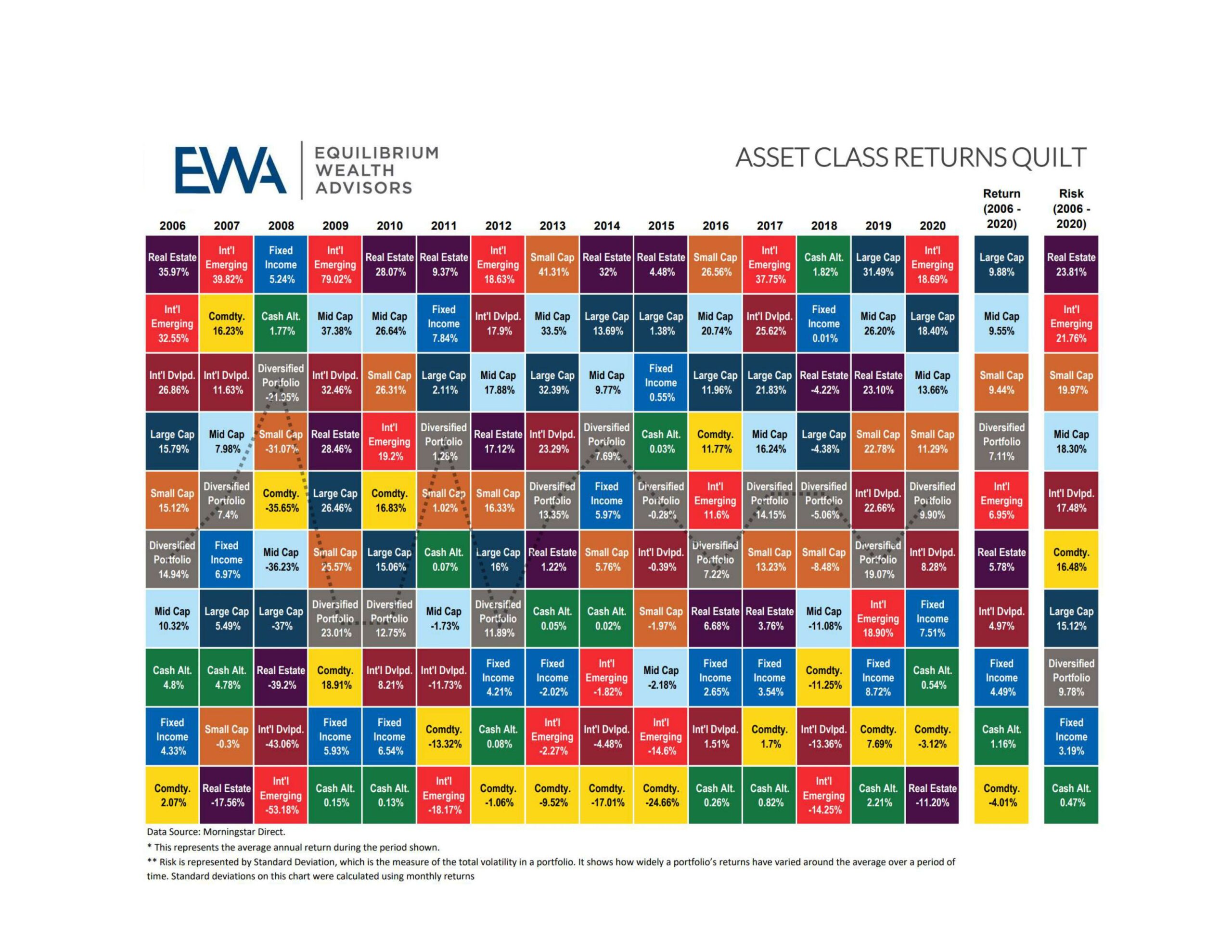

This chart below shows several asset class investments you could have made from 2006-2020:

The gray box shows what an asset allocated portfolio invested in all 9 asset classes with a mix of 60% equity/ 40% fixed income. This trends right in the middle, and over 15 years, has been between 6-7% return, and risk has historically been low.

Asset allocation increases the likelihood that some portion of the portfolio will maintain positive returns to support the possible need for a withdrawal without selling other positions at a loss. For example, in 2008, most equity asset classes returned negative. If you were in a 60/40 asset allocation portfolio as shown above, you would have had 40% of your portfolio in fixed income that you could have sold at a gain to avoid selling any losses if withdrawals were needed.

2nd pillar: Diversification:

The next concept we recommend following is diversification. Diversification refers to the process of having an assortment of investments within each asset class. Using the same football analogy, not having a diversified portfolio is like having a starting lineup with no backups. You would be in trouble if your quarterback got hurt. The same concept applies to diversification. If you have 25 investments within an asset class, that reduces diversification risk. And if you can have 100 investments in an asset class, that further reduces diversification risk. This is diversification and is intended to illustrate the importance of investing in different investments within each asset class, so you have a variety, where if some investments go down, others will hopefully maintain or gain value, thereby offsetting negative long-term effects to a portfolio.

The easiest way to explain diversification is by trying to break a pencil. Try to break 1 pencil and it is easy to snap it in half. Try to break 100 pencils wrapped in a bundle using a rubber band, and it would be nearly impossible. This is asset class diversification.

Many of the ETFs/mutual funds that we recommend to clients have 100+ underlying investments within the fund to make sure they are properly diversified. The stock market historically goes up and down, but over long periods of time has tended to trend up.

3rd Pillar: Long Term investing

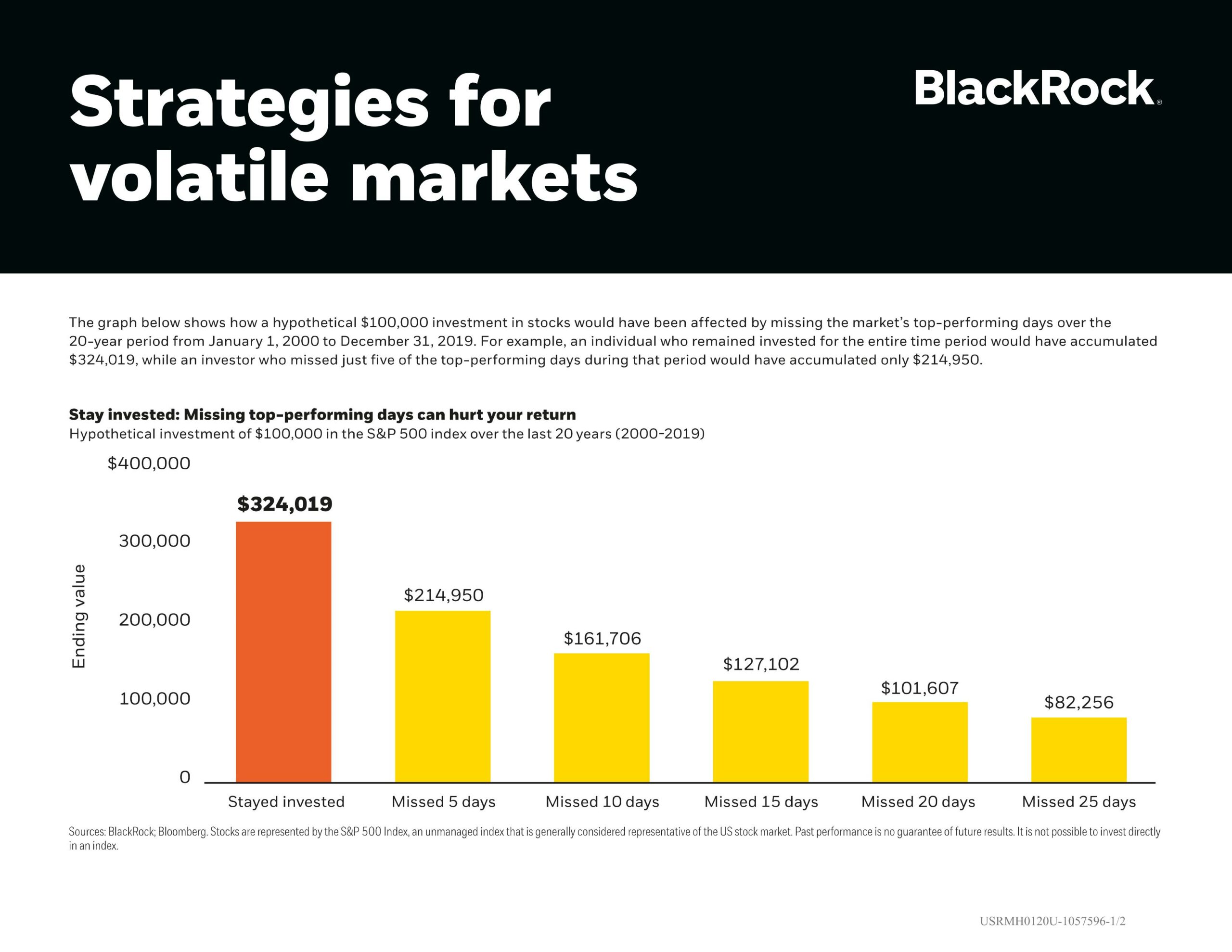

There was a study done by DALBAR, a financial research firm, that showed how the general temptation for investors to try and time the stock market often resulted in the investor diving into the market at the top and fleeing at the bottom. This chart shows this mistake monetized:

This is showing an investor that invests $100,000 on January 1st, 2000, into the S&P 500. The orange box shows that if they stayed invested every day until December 31st, 2019, their account would have grown to $324,019. The yellow box to the right shows the same investor, but they hypothetically pulled out of the market on the top 5 performing days in that same period. Their account is only $214,950 after missing the 5 best days. Their account is at a loss if they miss just the best 25 days out of 20 years with an ending balance of $82,256.

4th Pillar: Asset Location

The fourth concept we follow is asset location (different from asset allocation). Asset location is a tax efficient investment strategy that refers to how investments are distributed between various accounts, such as taxable accounts, tax-deferred or tax-free accounts. Sticking with the football analogy again, a quarterback is generally better suited to play on offense rather than defense. The same applies to an investment strategy. Tax efficient investments are well suited for use inside of a taxable account, whereas less tax efficient investments may be more appropriate to be placed inside an IRA where no taxes are paid while the account grows.

Instead of viewing each account you have as separate entities that should have the same asset allocation mix, it may be beneficial to view everything as one entity and reverse engineer which accounts hold each asset class. Decide on asset allocation and diversification mix-up first, and then allocate positions where they are best suited for tax efficiency. Example would be keeping corporate bonds outside of your taxable account, but okay to keep them inside your IRA (since they pay interest that is taxed at marginal tax rates). The most aggressive growth asset classes should be placed in your Roth IRA where all growth and distributions are tax free assuming the 5-year rule (if converted or rolled into a Roth), and age of 59 ½ has been reached.

Having a sound investment strategy and principles to stick to when times in the market get hard will help live life by design, rather than worrying about what the market does or does not do when making decisions.

_______________________________________________________________________________

Equilibrium Wealth Advisors is a registered investment advisor. The contents of this article are for educational purposes only and do not represent investment advice.

Stock markets are volatile, and the prices of equity securities fluctuate based on changes in a company’s financial condition and overall market and economic conditions. Although common stocks have historically generated higher average total returns than fixed-income securities over the long-term, common stocks also have experienced significantly more volatility in those returns and, in certain periods, have significantly underperformed relative to fixed-income securities. An adverse event, such as an unfavorable earnings report, may depress the value of a particular common stock held by the Fund. A common stock may also decline due to factors which affect a particular industry or industries, such as labor shortages or increased production costs and competitive conditions within an industry. For dividend-paying stocks, dividends are not guaranteed and may decrease without notice.

Past performance is no guarantee of future results. The change in investment value reflects the appreciation or depreciation due to price changes, plus any distributions and income earned during the report period, less any transaction costs, sales charges, or fees. Gain/loss and holding period information may not reflect adjustments required for tax reporting purposes. You should verify such information when calculating reportable gain or loss.

This content has been prepared for general information purposes only and is intended to provide a summary of the subject matter covered. It does not purport to be comprehensive or to give advice. The views expressed are the views of the writer at the time of issue and may change over time. This is not an offer document, and does not constitute an offer, invitation, investment advice or inducement to distribute or purchase securities, shares, units or other interests or to enter into an investment agreement. No person should rely on the content and/or act on the basis of any matter contained in this document. The tax and estate planning information provided is general in nature. It is provided for informational purposes only and should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.