Please select a default template!

Medicare surcharges can be a huge drain on your retirement savings. If not planned around carefully, you could end up paying thousands of dollars in extra premiums each year. In this blog post, we will discuss how to help avoid Medicare surcharges and keep more money in your pocket during retirement.

What is Medicare?

Medicare is a federal health insurance program that is available for individuals over age 65 and individuals with disabilities. There are four parts of Medicare:

Although Medicare Part B and Part D costs are both determined by income, this article is going to focus on Part B only as this is the biggest culprit for rising costs.

Understanding Part B Costs-

Medicare Part B is paid through monthly premiums, which most often are deducted directly from Social Security retirement benefits. The premium cost is determined by income, specifically a person’s modified adjusted gross income (MAGI). MAGI is the adjusted gross income that is reported on line 11 of your federal tax return, plus any tax-exempt interest income (such as municipal bond earnings). It is important to note that Medicare Part B premiums for the current year are based on MAGI from 2 years prior, so for example, 2023 premiums will be based on 2021 MAGI.

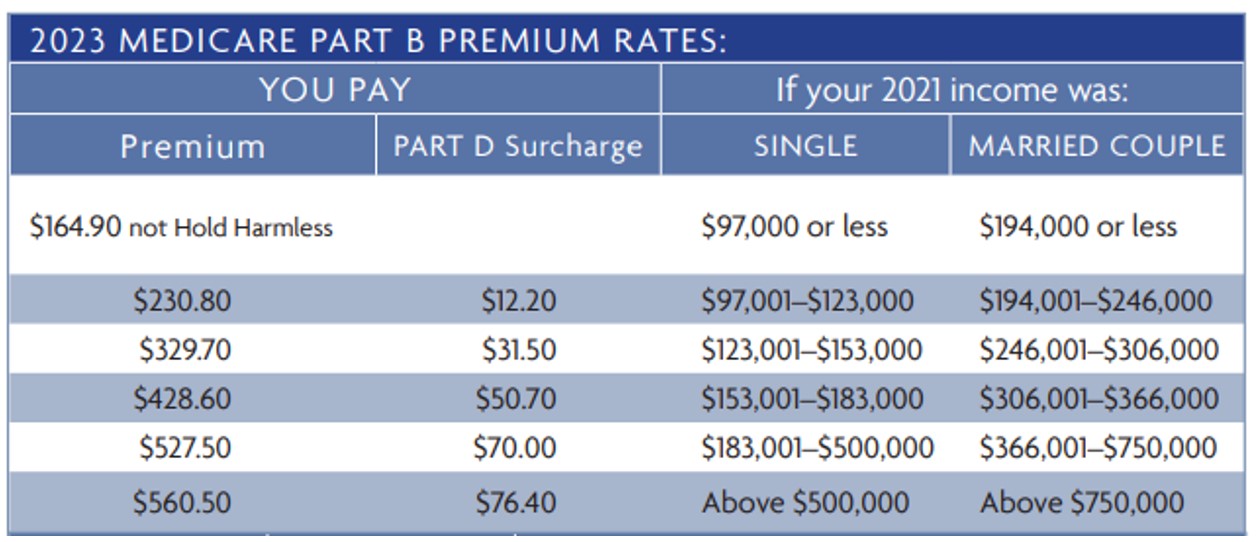

Here is a breakdown of 2023 Part B premiums:

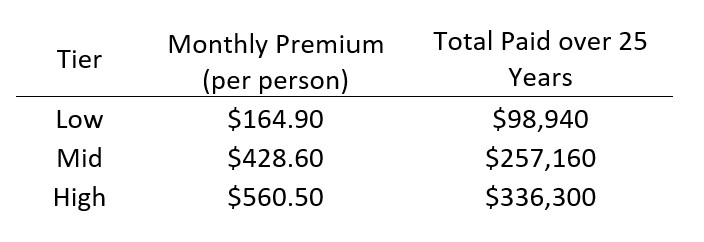

Next we will take a look at total Part B premiums for a couple filing a joint return over a 25-year retirement (no COLA adjustments) for low, mid, and high tiers.

If proper planning is not in place, it is very easy to wind up paying a surcharged premium throughout the duration of retirement. Typically, the surcharged premium is a result of required minimum distributions (RMDs), which is the amount of money that must be withdrawn from pretax retirement plans (most often IRAs) starting at age 72. RMDs are calculated by dividing the prior December 31 balance by a life expectancy factor that the IRS publishes in Tables in Publication 590-B.

Assuming a married couple at age 75 receives $30k/year (each) in Social Security benefits, $50k/year pension income, $30k/year in dividends, taxable interest, and capital gains, total income before any portfolio withdrawals is $140k. If we assume $2M balance in qualified retirement accounts, RMDs will be approximately $81k at age 75, bringing total gross income to $221k.

In this example, the couple would pay $230.80/mo (each) in Part B costs. Total annual cost combined = $5,539.20

If we assume $5M in qualified retirement accounts (instead of $2M), the annual RMD would be closer to $203k at age 75, bringing total gross income to $343k. In this example, the couple would pay $428.60/mo (each) in Part B costs. Total annual cost combined = $10,286.40

Surcharged Part B premiums can be amplified by the “Widow Penalty,” which occurs when 1 spouse passes away. The widow is often left paying a much higher Part B premium because IRAs are typically left to the surviving spouse (so RMD does not change), and the higher Social Security benefit between the 2 spouses remains in place.

For example, if a married couple has MAGI of $300k, they will pay $329.70/mo (each) in Part B premiums.

If a single person (widow) has MAGI of $250k, they will pay $527.50/mo in Part B premiums.

How to Prevent Surcharges-

You can control your Part B costs and avoid surcharges through proactive planning. As we described above, the surcharge is typically a result of RMDs that begin at age 72, which force an individual to withdrawal from the account (and realize income) regardless of whether or not they actually need the funds to meet their living expenses. Future RMDs can be minimized through the following:

Assuming you meet IRS distribution requirements, Roth IRAs receive 100% tax-free treatment for both earnings and distributions. Therefore, by having an optimal Pretax vs Roth IRA mix prior to age 72 (when RMDs start), you can control how much income you will realize when mandatory distributions begin.

For example, the RMD for a 75-year-old with a $3M IRA would be $121k/year, vs $40k/year if the IRA balance is $1M.

Here is a video resource from EWA describing the benefits of Roth Conversion Planning- https://vimeo.com/manage/videos/547932830

In addition to Roth planning, you can also avoid Part B surcharges through efficient cashflow planning (specifically deciding where to pull income from during retirement years). For example, if Social Security income, pension income, and RMDs put you near the end of a Part B tier, consider pulling from a source that does not increase MAGI. A few examples include distributions of basis from a taxable account, cash savings, and utilizing cash value inside of a life insurance policy (return of basis and policy loans are not subject to MAGI).

Here is a video resource from EWA describing how whole life insurance can be utilized – https://vimeo.com/manage/videos/750103505/transcript?ts=501700

This highlights the significance of having a well-rounded asset mix. If your balance sheet consists primarily of pretax retirement assets, you are the mercy of RMDs, future tax rates, and future Medicare Part B premiums (all of which are ‘unknowns’ that you as a retiree have no control over).

Situations like this are precisely why a sound financial plan is needed, especially during distribution years. If proper tax / financial planning is in place, you can potentially save thousands during retirement and avoid unnecessary costs by having an assortment of assets to pull from (between taxable and tax-free sources).

Here is a video resource from EWA describing a few additional tips and information around Medicare – https://vimeo.com/manage/videos/693232984

__________________________________________________________________________________

Equilibrium Wealth Advisors is a registered investment advisor. The contents of this article are for educational purposes only and do not represent investment advice.

Stock markets are volatile, and the prices of equity securities fluctuate based on changes in a company’s financial condition and overall market and economic conditions. Although common stocks have historically generated higher average total returns than fixed-income securities over the long-term, common stocks also have experienced significantly more volatility in those returns and, in certain periods, have significantly underperformed relative to fixed-income securities. An adverse event, such as an unfavorable earnings report, may depress the value of a particular common stock held by the Fund. A common stock may also decline due to factors which affect a particular industry or industries, such as labor shortages or increased production costs and competitive conditions within an industry. For dividend-paying stocks, dividends are not guaranteed and may decrease without notice.

Past performance is no guarantee of future results. The change in investment value reflects the appreciation or depreciation due to price changes, plus any distributions and income earned during the report period, less any transaction costs, sales charges, or fees. Gain/loss and holding period information may not reflect adjustments required for tax reporting purposes. You should verify such information when calculating reportable gain or loss.

This content has been prepared for general information purposes only and is intended to provide a summary of the subject matter covered. It does not purport to be comprehensive or to give advice. The views expressed are the views of the writer at the time of issue and may change over time. This is not an offer document, and does not constitute an offer, invitation, investment advice or inducement to distribute or purchase securities, shares, units or other interests or to enter into an investment agreement. No person should rely on the content and/or act on the basis of any matter contained in this document. The tax and estate planning information provided is general in nature. It is provided for informational purposes only and should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.