Please select a default template!

Many often wonder: How can I best save for retirement? Outside of a workplace retirement plan, there are seemingly many different investment vehicles at one’s disposal to save for the long-term. One of the most tax-efficient vehicles to save for retirement is the Roth IRA, introduced as part of the Taxpayer Relief Act of 1997. Here are five key advantages to investing in a Roth IRA:

1. Roth IRAs Grow Tax-Free and Distribute Tax-Free

A Roth IRA is one of the most tax-efficient vehicles you can invest after-tax dollars. Any growth and distributions of a Roth IRA occur free of ordinary income and capital gains tax, provided you’ve had the account established for five years and do not take distributions until age 59.5. Whereas in a taxable investment account you would be subject to tax on dividends and interest each year, as well as capital gains tax on any growth when you take a distribution.

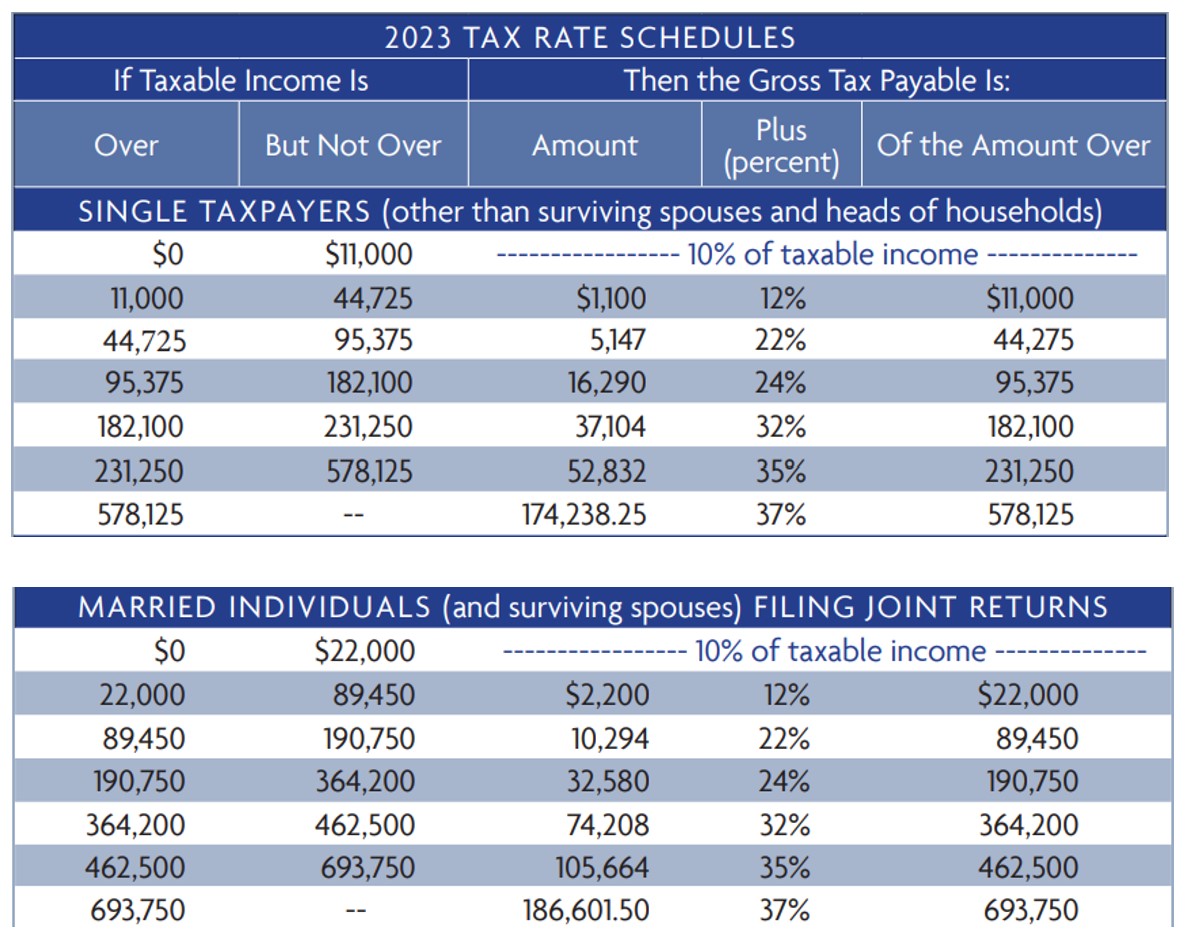

In a Traditional IRA, any pre-tax distributions (after attaining age 59.5) are subject to ordinary income tax, as shown below:

Depending on your income levels and filing status, this tax could be as high as 37%.

2. You Can Access Your Contributions From a Roth IRA Tax and Penalty Free, At Any Time

A lesser-known advantage of a Roth IRA is that you can access your basis, or after-tax money that you have physically contributed, tax and penalty free at any time. This flexibility option is not shared amongst other investment vehicles. In a Traditional IRA, for example, if you wanted to access your pre-tax basis before age 59.5, you would be subject to ordinary income tax and a 10% early withdrawal penalty on your distributions. Not only does taking your contributions out of a Roth IRA incur no tax or penalty, but there is no requirement for how you use your distributions.

3. Roth IRAs Do Not Have Required Minimum Distributions (RMDs)

Required minimum distributions are mandated by the government, detailing that distributions will have to be made from certain accounts once the account holder reaches age 73 (as of the Secure Act 2.0’s recent passing). Roth IRAs are not subject to RMDs, and therefore give the account holder autonomy over when and how he/she distributes money.

For example, let’s assume a client has a Traditional IRA with a balance of $1,000,000. Furthermore, let’s assume when the client turns 73, there is a market drop, leaving her Traditional IRA balance at $900,000. RMDs are calculated using actuarial data, but generally speaking they are around 4% of the account value in a client’s early 70’s.

So, in this case, let’s assume 4% of $900,000 is distributed ($36,000). This leaves the account balance at $864,000 from its original $1,000,000 balance.

If the $1,000,000 balance was a Roth IRA, not Traditional, the client could in theory choose not to take a distribution if one was not needed and allow the account to recover. This avoids sequence of returns risk and is vital to sustaining long-term portfolio growth throughout retirement.

4. Roth IRAs Pass To Heirs Income Tax-Free

Roth IRAs are great for legacy planning, as they pass along to the next generation income tax-free.

Let’s assume a client passes away with a $1,000,000 Traditional IRA balance and leaves it to his daughter. Current law mandates that the daughter in this case must fully liquidate the $1,000,000 balance in a ten-year period. If the daughter takes a $100,000 distribution in the first year, this will count as $100,000 of income in her name– potentially bumping her up into a higher tax bracket and increasing her tax liability.

If the $1,000,000 inherited account was a Roth IRA, not a Traditional IRA, the daughter in this case would still be forced to liquidate the account within ten years, only all distributions would be completely tax-free, and therefore not subject her to any additional tax liability.

5. Roth IRAs Allow for Strategic Asset Location

Because of the tax-free nature of Roth IRAs, they can be great vehicles to hold what are considered to be “inefficient funds.” Real estate funds and value funds, for example, are considered to be tax inefficient because they release capital gains and dividends that the fund holder is subject to each year. These “inefficient” funds can be valuable to hold inside of a Roth IRA, since all the growth is tax-free and account holders would avoid these capital gains and dividends subject to taxation. If these types of funds were held in a taxable investment account, for example, any dividends or capital gains are reportable as taxable income– hitting one’s ordinary income tax rate.

In summary, a Roth IRA is one of the best ways to save for retirement in a tax-efficient manner. If you have any questions about your Roth IRA specifically, please consult with a trusted financial professional.

________________________________________________________________________________

Equilibrium Wealth Advisors is a registered investment advisor. The contents of this article are for educational purposes only and do not represent investment advice.

Stock markets are volatile, and the prices of equity securities fluctuate based on changes in a company’s financial condition and overall market and economic conditions. Although common stocks have historically generated higher average total returns than fixed-income securities over the long-term, common stocks also have experienced significantly more volatility in those returns and, in certain periods, have significantly underperformed relative to fixed-income securities. An adverse event, such as an unfavorable earnings report, may depress the value of a particular common stock held by the Fund. A common stock may also decline due to factors which affect a particular industry or industries, such as labor shortages or increased production costs and competitive conditions within an industry. For dividend-paying stocks, dividends are not guaranteed and may decrease without notice.

Past performance is no guarantee of future results. The change in investment value reflects the appreciation or depreciation due to price changes, plus any distributions and income earned during the report period, less any transaction costs, sales charges, or fees. Gain/loss and holding period information may not reflect adjustments required for tax reporting purposes. You should verify such information when calculating reportable gain or loss.

This content has been prepared for general information purposes only and is intended to provide a summary of the subject matter covered. It does not purport to be comprehensive or to give advice. The views expressed are the views of the writer at the time of issue and may change over time. This is not an offer document, and does not constitute an offer, invitation, investment advice or inducement to distribute or purchase securities, shares, units or other interests or to enter into an investment agreement. No person should rely on the content and/or act on the basis of any matter contained in this document. The tax and estate planning information provided is general in nature. It is provided for informational purposes only and should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.