Please select a default template!

When it comes to tax planning, one of the most important decisions you can make is where to hold your assets. If you aren’t tax efficient, you could be leaving a lot of money on the table. In this blog post, we will discuss asset location and how it can help save you taxes and will also provide some tips on how to get started with tax-efficient portfolio management.

What is Asset Location?

Asset location is a strategy that has the potential to lower your taxes by putting tax-inefficient investments inside of tax-deferred accounts, and tax efficient assets inside of taxable accounts. Simply put, asset location looks at where you are holding specific investments with the overall goal of making your portfolio as tax efficient as possible.

3 Types of Investment Accounts-

The tax treatment of each investment account will directly influence where different types of investments should be held. Here are the 3 main investment account categories:

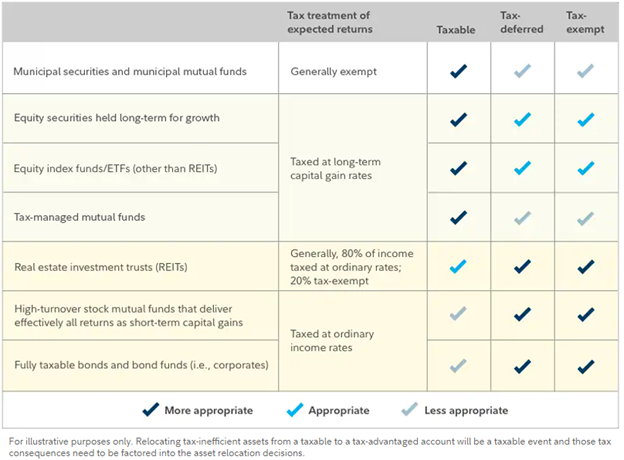

Tax Efficient vs Tax Inefficient Investments-

Now that we have covered the tax treatment for each account, let’s look at tax efficient vs tax inefficient investments.

Application-

In general, it is not tax efficient to hold dividend paying stocks and corporate bonds inside of taxable accounts. When you earn interest, the net amount that you receive is taxable as ordinary income and can lead to a liability when you file. For example, if you are in the 37% tax bracket and receive $10,000 in corporate bond interest, this translates to an additional $3,700 in tax. High turnover mutual funds and REITs should also be avoided in taxable accounts because these vehicles pass along capital gains to investors, which is often times out of the investor’s control and unexpected.

If you want fixed income exposure inside of a taxable account, consider holding municipal bonds instead of corporate bonds. Municipal bond interest is not taxable as ordinary income at the federal level, so this would be a tax efficient way to invest in bonds within a taxable account; however, the interest rates tend to be lower. It is important to note that a retiree trying to avoid a medicare surcharge needs to factor municipal bond interest as countable to their MAGI. (modified adjusted gross income)

When it comes to equity investing, consider holding growth-oriented funds instead of value-oriented funds. Growth mutual funds and ETFs focus on reinvesting profits instead of distributing them to shareholders in the form of dividends, which will limit tax liability. Lastly, rather than holding high turnover mutual funds inside of taxable accounts, consider holding passively managed ETFs which track the major indexes. These funds typically do not pass capital gains to investors and will result in less tax liability as opposed to actively managed funds with high turnover.

Since there is no tax until you distribute funds from tax-deferred accounts, there is no downside to holding tax-inefficient vehicles inside of these accounts. For example, it would be suitable to hold corporate bonds in an IRA instead of a taxable account because the bond interest would not be taxable (since an IRA is a tax-deferred account). The same goes for dividend paying equities and high turnover mutual funds. If these are held inside of a tax-deferred account, there is no tax liability until you distribute the funds out of the account. Or even better, no taxes at all during distribution in a Roth (again if all IRS rules are met).

On a high level, the investment vehicles that should be avoided in taxable accounts should be favored within tax-deferred and tax-exempt accounts.

Closing Thoughts-

Instead of viewing a Roth IRA, 401(k), taxable account, etc. as separate entities that should have the same asset allocation mix, it is more beneficial to view everything as one entity then reverse engineer which accounts hold each asset class / fund (dividend vs non dividend paying funds).

Instead, decide your asset allocation and diversification mix first, then allocate positions where they are best suited for tax efficiency.

Over the life of your portfolio, this could save thousands of dollars in taxes, and result in more money in your pocket to put towards your financial planning goals.

____________________________________________________________________________

Equilibrium Wealth Advisors is a registered investment advisor. The contents of this article are for educational purposes only and do not represent investment advice.

Stock markets are volatile, and the prices of equity securities fluctuate based on changes in a company’s financial condition and overall market and economic conditions. Although common stocks have historically generated higher average total returns than fixed-income securities over the long-term, common stocks also have experienced significantly more volatility in those returns and, in certain periods, have significantly underperformed relative to fixed-income securities. An adverse event, such as an unfavorable earnings report, may depress the value of a particular common stock held by the Fund. A common stock may also decline due to factors which affect a particular industry or industries, such as labor shortages or increased production costs and competitive conditions within an industry. For dividend-paying stocks, dividends are not guaranteed and may decrease without notice.

Past performance is no guarantee of future results. The change in investment value reflects the appreciation or depreciation due to price changes, plus any distributions and income earned during the report period, less any transaction costs, sales charges, or fees. Gain/loss and holding period information may not reflect adjustments required for tax reporting purposes. You should verify such information when calculating reportable gain or loss.

This content has been prepared for general information purposes only and is intended to provide a summary of the subject matter covered. It does not purport to be comprehensive or to give advice. The views expressed are the views of the writer at the time of issue and may change over time. This is not an offer document, and does not constitute an offer, invitation, investment advice or inducement to distribute or purchase securities, shares, units or other interests or to enter into an investment agreement. No person should rely on the content and/or act on the basis of any matter contained in this document. The tax and estate planning information provided is general in nature. It is provided for informational purposes only and should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.