In recent years, the Mega Backdoor Roth strategy has gained popularity among high-income earners seeking to maximize their retirement savings. This advanced financial planning tactic allows participants in certain 401(k) plans to make sizable after-tax contributions and convert them to their Roth 401(k), potentially creating a powerful tax-free growth vehicle. However, Allegheny Health Network has recently implemented changes to its after-tax contribution limits, altering how employees can take advantage of this strategy.

In this post, we’ll break down what the Mega Backdoor Roth is, what the new changes entail, and what it means for employees and medical professionals who’ve been leveraging this approach—or planning to. Whether you’re a seasoned participant or just exploring your retirement options, understanding these updates is key to making the most of your employer-sponsored plan.

First, it is important to understand how the Mega Backdoor Roth strategy works. The key figure to keep in mind when executing this strategy is the 415(c) limit for retirement plan contributions, or the total amount that can be contributed to a qualified retirement plan in a given calendar year. In 2025 for those under the age of 50, that limit is $70,000. Meaning, between your salary deferral, employer match, and after-tax contributions, you can contribute up to $70,000 into your 401k or 403b in a calendar year.

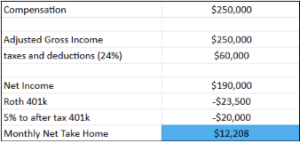

Specifically for AHN employees, let’s walk through a few examples to see how this would look in practice. Let’s assume an AHN employee is earning $250,000 of compensation. To fully maximize their contributions, they can first look to contribute the maximum salary deferral, or 402(g) limit of $23,500, to their pre tax or Roth 401(k). In this instance, we’ll assume all $23,500 is contributed to their Roth 401(k), as Roth plans have a variety of tax efficiencies and advantages. They’ll also receive their employer match from AHN of 4% (only on their first $350,000 of compensation), plus a 1% annual contribution as well. So far, this person has $23,500 from their deferral + $12,500 from AHN’s match.

The big change, beginning June 6th, 2025, is that AHN is increasing the after-tax percentage contribution for employees from 5% to 8%. Meaning, employees can now get more money into their after-tax 401k, increasing the amount they can convert to their Roth 401k to finalize the MegaBackdoor Roth strategy. The employee above making $250,000 can now get an additional $20,000 in after-tax contributions added to their 401k each year.

Between $23,500 worth of deferrals, $12,500 of AHN match, and $20,000 of after-tax contributions, this person is now contributing $56,000 to their 401k, with the majority of these contributions being Roth dollars, which grow and distribute income tax free.

Breaking down how this would appear on a monthly cash flow basis, the $250,000 employee would realistically look at netting ~$12,000/month after taxes and retirement plan contributions if they implement this strategy to the fullest extent:

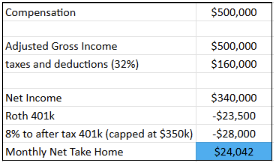

Let’s break down another example, but this time the employee is earning $500,000 instead of $250,000. The MegaBackdoor Roth plan begins the same way: $23,500 worth of deferrals to the Roth 401k. The change we need to be aware of from the first example is that the employer match from AHN is only based on the first $350,000 of compensation, which is 2025’s maximum includible compensation limit posted by the IRS. So, the employee would receive a 5% match on $350,000, not $500,000. With this in mind, the AHN match they’d receive is $17,500. Now beginning in June 2025, they can contribute 8% to their after-tax 401k (again, an increase from the previous 5% limit).

An 8% after-tax contribution (capped at the IRS limit’s first $350,000 of compensation) is an additional $28,000 that this person could get into their 401k plan on an annual basis, before converting to their Roth 401k to finalize the MegaBackdoor Roth strategy.

This person’s $23,500 deferral plus $17,500 match plus $28,000 after-tax contribution means they can contribute $69,000 annually to their plan. In practice, this person would be netting ~$24,000/month after taxes and contributions if they fully implemented this plan:

In summary, this is a positive development for AHN employees. In the state of Pennsylvania, money held inside of a 401(k) is asset protected in the event of a lawsuit– making the 401(k) one of the best places to accumulate wealth for the long-term. Additionally, since a large majority of these contributions would be Roth deferrals or converted Roth money, there would not be any ordinary income tax on any growth of these funds nor distribution of these funds in the future.

If you have any questions about how your AHN 401(k) plan is currently structured, or how these new changes impact you specifically, please reach out to a trusted tax or financial advisor to help consider all available options.